What Is Three to Six Months Savings? Your Clear Guide

Many people hear the advice to save three to six months of expenses and nod along without truly understanding what it means in practice. What counts as an expense? Three months or six? What if you are self-employed or supporting a family on a single income? Understanding what is three to six months savings, how to calculate it correctly, and how to build it step by step is one of the most useful things you can do for your financial health. This guide cuts through the noise and gives you a clear, practical path forward.

Table of Contents

- Key Takeaways

- What three to six months savings actually means

- How to decide between three months and six months

- Building your emergency fund step by step

- Common misconceptions about emergency savings

- Emergency fund examples by household type

- My honest take on the three to six months rule

- Start building your financial safety net with Amanahfund

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Target essential expenses only | Calculate your fund based on bare-bones monthly costs, not your total spending. |

| Your situation shapes the target | Income stability, household structure, and job type determine whether three or six months is right for you. |

| Start small, build steadily | Begin with a $1,000 milestone, then progress to one, three, and six months of savings. |

| Use a tiered liquidity approach | Keep immediate funds in accessible accounts and longer buffers in slightly higher-yield instruments. |

| Treat it as a living resource | Use the fund when needed and replenish it. It is meant to be used, not preserved untouched. |

What three to six months savings actually means

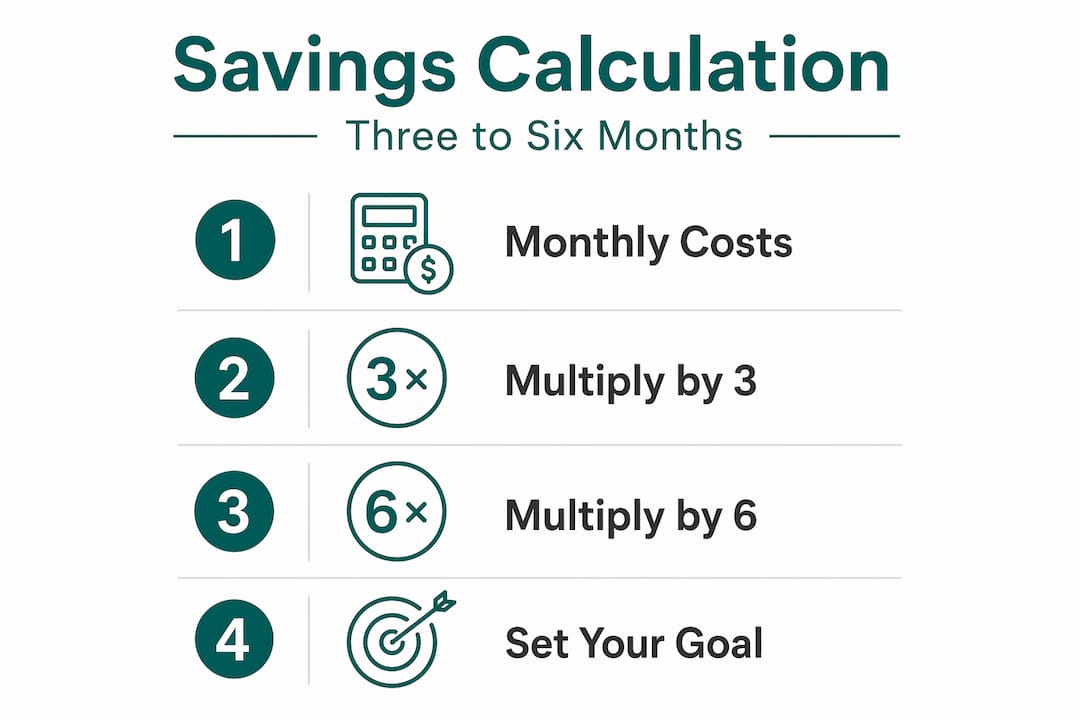

The phrase “three to six months savings” refers to an emergency fund large enough to cover your essential living expenses for three to six months without any income. According to emergency fund guidelines, a good rule of thumb is to save three to six months of current living expenses to avoid going into debt from unexpected events like job loss, illness, or a major repair.

The critical word here is essential. Your target amount is not based on what you currently spend each month in total. It is based on what you need to spend to keep your household running. The bare-bones monthly expenses you should be counting are:

- Housing: Rent or mortgage payment

- Utilities: Electricity, water, gas, and basic internet

- Groceries: Realistic food costs for your household

- Insurance: Health, auto, renters or homeowners insurance premiums

- Minimum debt payments: The floor payments on any loans or credit cards

What you leave out is equally important. Dining out, subscriptions, clothing, entertainment, gym memberships, and travel do not belong in your emergency fund calculation. These are discretionary costs. In a true financial emergency, you would cut them.

So if your essential monthly expenses total $3,000, your three-month target is $9,000 and your six-month target is $18,000. Those are the bookends of your savings for three to six months.

Pro Tip: Go through your last three months of bank and credit card statements to identify your true essential expenses. Most people overestimate what they spend on necessities and underestimate their discretionary spending.

How to decide between three months and six months

The 3-6 month range is a starting point, not a formula. Your personal and financial circumstances determine where within that range you should aim, and whether you should go beyond it entirely.

The table below lays out the main factors and how they shape your target:

| Factor | Lean toward 3 months | Lean toward 6 months or more |

|---|---|---|

| Income sources | Dual income household | Single income household |

| Job security | Stable, in-demand career field | Volatile or niche industry |

| Employment type | Salaried employee | Self-employed or freelance |

| Dependents | No dependents | Children or aging parents |

| Health | Good health, low medical risk | Chronic illness or high medical costs |

| Financial obligations | Low debt, flexible budget | High fixed debt payments |

According to income-based fund sizing, dual-income households with stable jobs can reasonably target three months of expenses, while single-income households should aim for six months, and self-employed individuals should consider nine to twelve months given the unpredictability of their cash flow.

Think about how long it would realistically take you to replace your income if you lost it today. A software engineer in a high-demand field might find work in six weeks. A specialist in a contracting industry might need four months. Your emergency fund should roughly match that realistic window.

Pro Tip: If your household depends on a single income and you have children, aim for six months at a minimum. The combination of one income source and multiple financial dependents creates a compounding risk that a three-month fund may not adequately cover.

For Muslim families managing a household budget built around shared responsibilities, family financial planning resources can help clarify how much each household member’s expenses contribute to the overall target.

Building your emergency fund step by step

Knowing how much to save for emergencies is one thing. Getting there requires a clear progression. Building this fund is a dynamic process that balances debt payoff, investing, and saving with distinct milestones to guide you forward.

-

Start with $1,000. An initial $1,000 milestone prevents most small, debt-inducing emergencies like a car repair or unexpected medical bill. This is not your final destination, but it is a meaningful and achievable first step.

-

Work toward one full month of essential expenses. Once you have your $1,000 buffer, calculate your essential monthly costs and make that your next target. This single month of coverage changes the psychological reality of your finances significantly.

-

Balance saving with debt repayment. If you carry high-interest debt, you do not need to pause all progress on debt to fund savings. A common approach is to split extra monthly cash flow equally, putting half toward debt and half toward your emergency fund until you reach three months of coverage.

-

Choose the right account. Your emergency fund needs to be liquid, meaning you can access it quickly without penalty. High-yield savings accounts and money market accounts are strong options because they offer better returns than a standard savings account without locking up your money.

-

Use a tiered liquidity approach. A tiered liquidity strategy involves keeping one to two months of expenses in an instantly accessible account and placing the remainder in slightly higher-yield instruments like short-term certificates of deposit or money market funds. This way your money works harder without sacrificing access.

-

Replenish after every withdrawal. The moment you use your emergency fund, create a plan to refill it. Treat replenishment with the same urgency as the original savings goal.

Pro Tip: Automate a fixed transfer to your emergency fund account on the same day you receive your paycheck. When the transfer happens before you see the money in your checking account, you are far less likely to spend it.

Common misconceptions about emergency savings

One of the most persistent misconceptions in personal finance is that a $1,000 fund is sufficient. A small buffer like that covers a minor car repair. It does not cover job loss, a medical emergency, or a major home issue. It is a foundation, not a completed structure.

The second major misconception is about what counts as an expense. Confusing total household income with essential expenses is one of the most common errors people make when calculating their emergency fund target. Some people calculate their target based on their take-home pay, which inflates the number and makes the goal feel impossible. Others include every discretionary expense, which is equally misleading.

Then there is the overwhelm problem. 55% of Americans say the three-to-six-month rule feels unrealistic. That statistic is not discouraging. It is clarifying. The rule sounds daunting because most people frame it as one giant goal rather than a progression of smaller, achievable targets.

For gig workers and freelancers, the financial safety net calculation looks different. Variable monthly income means your expenses also fluctuate. A practical approach is to calculate your average essential expenses over twelve months and use that number as your monthly baseline.

The emergency fund is not a prize you save up for once and then admire. It is a living resource that you use when needed and rebuild when depleted. Thinking of it as a tapped-and-replenished account is the healthiest way to relate to it.

Emergency fund examples by household type

Abstract guidance only goes so far. These concrete examples show how the three to six months savings rule applies across different life situations.

| Household type | Monthly essential expenses | 3-month target | 6-month target |

|---|---|---|---|

| Dual income, no dependents | $3,200 | $9,600 | $19,200 |

| Single income, two children | $4,500 | $13,500 | $27,000 |

| Self-employed, no dependents | $2,800 | $8,400 | $16,800 (aim for 9-12 months) |

| Dual income, one child | $4,000 | $12,000 | $24,000 |

Notice how the single-income household with dependents has a six-month target nearly three times that of the self-employed individual with no dependents, even though their monthly expenses are only 60% higher. The risk profile compounds the target, not just the dollar amount.

For families managing these goals together, a shared household budget approach helps both spouses stay aligned on which expenses are truly essential and what the realistic monthly savings capacity looks like. The importance of savings becomes especially clear when you see how a 3-6 month window covers most financial disruptions, from unemployment to medical recovery to family crises.

Also worth noting: most serious financial emergencies resolve within a 3-6 month window, which is exactly why this range was established as the standard. It is not arbitrary. It reflects real-world emergency timelines.

My honest take on the three to six months rule

I have watched a lot of families treat their emergency fund as a homework assignment they complete once and forget. That mindset is where things go wrong.

What I have learned is that the number matters less than the habit. I have seen households with six months saved who dip into it for non-emergencies and never rebuild. I have also seen households that started with $500 and systematically built to three months of coverage, and those families sleep better at night regardless of market conditions or job instability.

The part most people overlook is the emotional dimension. When you know you have three months of essential expenses sitting in a liquid account, your financial decision-making changes. You negotiate salary differently. You take career risks differently. You weather an unexpected expense without panic.

My honest view: if you are carrying any consumer debt, start with the $1,000 milestone and work on debt aggressively at the same time. Do not delay building some buffer while you eliminate debt, because life does not pause for your payoff plan. Once debt is managed, push hard toward three months, and then reassess based on your actual risk profile at that point.

The budgeting strategy you use matters, too. A clear, intentional budget that separates essentials from discretionary spending makes the emergency fund calculation much easier and keeps your target honest.

— Imran

Start building your financial safety net with Amanahfund

Knowing what three to six months savings means is only the first step. Acting on that knowledge requires the right tools to track your essential expenses, set savings goals, and keep your household aligned.

Amanahfund is a halal-first budgeting app built specifically for Muslim families. It lets you set dedicated emergency fund savings goals, track spending through halal-aware categories, calculate your zakat, and share household budgets with your spouse or family members. Whether you are working toward your first $1,000 milestone or refining your six-month target, Amanahfund helps you stay focused, intentional, and true to your values. No ads. No interest-based products. No selling your data. Just a tool built for your dunya and your deen. Start with Amanahfund today and take the first step toward a genuine financial safety net.

FAQ

What is an emergency fund and how much should I save?

An emergency fund is a dedicated savings buffer that covers your essential living expenses if your income is disrupted. Most financial guidance recommends saving three to six months of essential expenses, adjusted based on your income stability and household situation.

What counts as an essential expense for an emergency fund?

Essential expenses include housing, utilities, groceries, insurance premiums, and minimum debt payments. Discretionary spending like dining out, subscriptions, and entertainment is excluded from your emergency fund calculation.

Should I save three months or six months of expenses?

Dual-income households with stable jobs can lean toward three months, while single-income households, those with dependents, or self-employed individuals should target six months or more. Your personal risk profile is the deciding factor.

Where should I keep my emergency fund?

Keep your emergency fund in a high-yield savings account or money market account for liquidity and modest growth. A tiered approach places one to two months in an immediately accessible account and the remainder in slightly higher-yield instruments.

Can I invest my emergency fund to earn more returns?

Your emergency fund should not be invested in volatile assets. The priority is accessibility and stability, not maximum growth. Locking emergency savings in stocks or long-term investments defeats the purpose of having funds available when you need them most.

Recommended

- How Much Does Hajj Cost and How to Save for It: A Practical Guide — Amanah Budget Blog

- How Much Does Hajj Cost and How to Save for It: A Practical Guide — Amanah Budget Blog

- Share Budget with Your Spouse App: 2026 Guide — Amanah Budget Blog

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account