How to Automate Halal Savings Transfers in 2026

TL;DR:

- Automated halal savings transfers involve scheduled, recurring deposits into Shariah-compliant accounts to build wealth without interest. They typically use Wadiah for principal protection and Mudarabah for profit-sharing, supporting various savings goals through digital platforms. Regular review and manual rebalancing remain essential to ensure alignment with goals and Islamic principles.

Automated halal savings transfers are defined as scheduled, recurring fund movements into Shariah-compliant accounts, designed to grow wealth without interest and in alignment with Islamic financial principles. The two foundational account types for this practice are Mudarabah (profit-sharing) and Wadiah (safekeeping with principal protection). Setting up recurring transfers on payday to these accounts is the most effective method for building consistent savings toward goals like Hajj, Ramadan, and zakat. Amanahfund’s halal-first approach to budgeting is built around exactly this kind of purposeful, values-driven financial behavior. When you automate halal savings transfers correctly, your money moves before you can spend it.

What types of halal savings accounts support automated transfers?

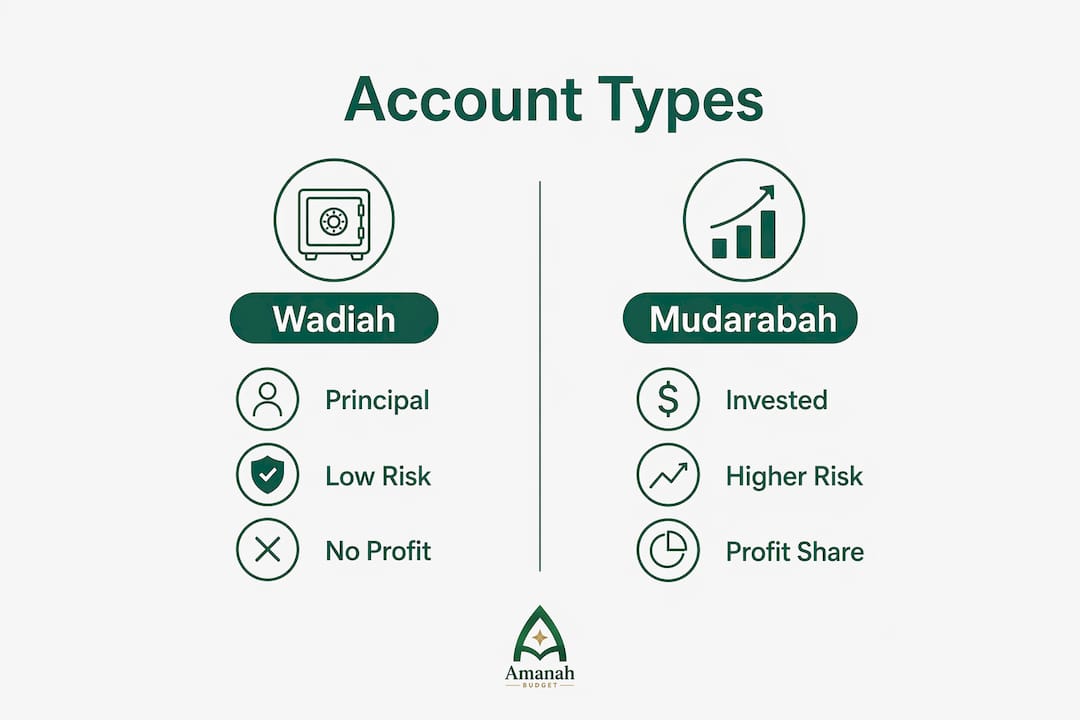

The right account type determines how your automated transfers grow and what protections you receive. Two Shariah-compliant structures dominate the space.

Wadiah accounts operate on a safekeeping principle. The bank holds your funds and guarantees the return of your principal. No profit is expected or promised. This makes Wadiah ideal for emergency funds or short-term goals where capital protection matters more than growth.

Mudarabah accounts work differently. You provide the capital, and the bank invests it according to Shariah guidelines. Profits are shared at a pre-agreed ratio. Returns are variable, not fixed, which keeps the arrangement free from riba (interest). Mudarabah accounts involve profit-sharing with variable returns, while Wadiah accounts provide principal protection without expected profit. Misunderstanding this distinction leads to real disappointment when returns do not match fixed-interest expectations.

A practical approach for Muslim families is to split savings across both account types. Liquid funds for near-term needs belong in Wadiah. Longer-term wealth building belongs in Mudarabah. Some Islamic finance practitioners recommend keeping three to six months of expenses in liquid accounts before directing surplus toward profit-sharing vehicles.

Digital Islamic banking platforms allow creation of up to 60 distinct sub-accounts or “pockets” for separate savings goals without extra fees. That means you can label one pocket for Hajj, another for Eid, another for education, and another for emergencies, all within a single platform. Each pocket receives its own automated transfer on a schedule you set.

| Account feature | Wadiah | Mudarabah |

|---|---|---|

| Principal protection | Yes | No |

| Expected profit | None | Variable (profit-sharing ratio) |

| Best for | Emergency funds, short-term goals | Long-term wealth building |

| Automation compatibility | High | High |

| Shariah compliance basis | Safekeeping contract | Profit-sharing contract |

Pro Tip: Label each savings pocket with a specific goal and a target date. Vague buckets like “savings” invite spending. Named pockets like “Hajj 2027” create accountability.

Which tools and fintech platforms enable halal savings automation?

Islamic fintech has moved well beyond basic banking. Major Islamic fintech platforms now offer recurring investment features that significantly increase consistency in wealth-building contributions after automation setup. The key phrase is “after setup.” The initial configuration takes effort. After that, the system runs without you.

Here are the core categories of tools that support halal savings automation:

- Islamic digital banks with multi-pocket features. These platforms let you create named sub-accounts and schedule recurring transfers to each one. No manual transfers required after setup.

- Halal robo-advisors and auto-invest platforms. These direct your contributions into Shariah-screened funds automatically. They handle the investment selection so you do not have to monitor markets.

- Budgeting apps with bank connectivity. Apps that connect to your bank through services like Plaid can track spending, flag non-halal categories, and help you calculate how much to automate each month.

- Banking-as-a-Service enabled apps. Platforms connected with Banking-as-a-Service enable automation in a few taps without additional effort. These are typically mobile-first and built for everyday Muslim families.

AI is reshaping the compliance side of this equation. AI integration in Islamic banking reduces Shariah compliance checking from weeks to minutes. Banks report up to a 78% reduction in pre-scholar screening time using proprietary AI systems. That speed means new halal products reach users faster, and automated transfers can be verified as compliant in near real time.

Pro Tip: Before choosing a platform, confirm it publishes its Shariah supervisory board membership and annual compliance reports. Transparency here is non-negotiable.

How to set up automated halal savings transfers step by step

Setting up a working system requires three things before you touch any app: a Shariah-compliant account, a clear set of savings goals, and a realistic monthly transfer amount. Without all three, automation becomes a guessing exercise.

Step 1: Open the right accounts

Open at least one Wadiah account for liquid savings and one Mudarabah account for longer-term goals. If your platform supports multiple pockets, create a separate pocket for each goal. Hajj, Umrah, Ramadan, education, and emergency funds each deserve their own labeled space.

Step 2: Calculate your transfer amounts using sinking fund principles

A sinking fund divides a known future expense by the number of months until you need it. Sinking fund strategies divide expected annual costs by 11–12 months to determine monthly automated transfer amounts. If Hajj will cost $8,000 and you have 20 months, your monthly transfer is $400. This removes guesswork and makes the goal concrete.

Use a savings calculator to run these numbers before you set up any recurring transfer.

Step 3: Schedule transfers on payday

Automate transfers to trigger the same day your paycheck arrives. This enforces the Islamic principle of saving before spending, not after. The shift moves saving behavior from “spending after saving” to “saving intentionally before spending.”

Step 4: Link accounts and configure automation

Connect your checking account to your savings platform. Set the transfer amount, frequency (weekly, biweekly, or monthly), and destination pocket. Most platforms complete this in under five minutes.

Step 5: Monitor and rebalance periodically

Automation does not eliminate the need for oversight. Manual rebalancing is necessary periodically to ensure asset allocation between liquid and invested funds aligns with risk profiles and goals. This is especially true for Mudarabah accounts, where profit-sharing ratios and market conditions can shift your allocation over time.

| Setup step | Key action | Consideration |

|---|---|---|

| Open accounts | Choose Wadiah and/or Mudarabah | Match account type to goal timeline |

| Calculate amounts | Apply sinking fund formula | Divide total goal by months remaining |

| Schedule transfers | Set payday trigger | Automate before discretionary spending |

| Link accounts | Connect via app or bank portal | Confirm Shariah compliance of platform |

| Rebalance | Review quarterly | Adjust for goal changes and returns |

Common challenges and mistakes in halal savings automation

Automation creates consistency, but it also creates blind spots. These are the mistakes Muslim families make most often.

- Goal creep from pooled funds. When all savings sit in one account, money meant for Hajj quietly funds an impulse purchase. Segregating savings into multiple labeled pockets prevents this. Each pocket has one purpose and one purpose only.

- Misunderstanding Mudarabah returns. Families who expect fixed monthly returns from profit-sharing accounts are setting themselves up for frustration. Users must discern the difference between profit-sharing and safekeeping accounts to set realistic expectations. Islamic banks do not pay fixed interest. They share profit or safeguard principal.

- Ignoring inflation on long-term goals. A Hajj fund that grows slowly may lose real value over five years. Fixed-fee, price-lock savings models offer inflation protection certified as halal by scholars. This guarantees value stability and certainty for long-term savings without riba. If your platform offers this feature, use it for goals that are three or more years away.

- Setting and forgetting without review. Automation handles the transfers. It does not handle life changes. A new baby, a job change, or a shift in Hajj costs all require you to revisit your transfer amounts.

- Choosing non-compliant platforms. Not every app that calls itself “Islamic” has a verified Shariah supervisory board. Always confirm certification before connecting your accounts.

“Automating Islamic finances builds discipline and fulfills spiritual obligations by binding money to the right purpose before it can be spent.” — Bank Jago on Islamic finance automation

Key Takeaways

Automating halal savings transfers works best when you combine Shariah-compliant account types, goal-specific pockets, sinking fund calculations, and periodic manual rebalancing.

| Point | Details |

|---|---|

| Choose the right account type | Use Wadiah for principal protection and Mudarabah for profit-sharing growth. |

| Segregate every goal | Create a labeled pocket for each savings goal to prevent misuse of funds. |

| Apply sinking fund math | Divide your total goal amount by months remaining to set the right transfer amount. |

| Automate on payday | Schedule transfers to trigger when income arrives, before discretionary spending begins. |

| Rebalance quarterly | Review allocations every three months to stay aligned with goals and Shariah compliance. |

Why automation and intention belong together

I have spent years watching Muslim families build detailed savings plans that fall apart within three months. The problem is almost never the plan. It is the gap between intention and action. You intend to transfer funds to your Hajj account every month. Then rent goes up, a car needs repair, and the transfer gets skipped. Then skipped again.

Automation closes that gap. When the transfer happens before you see the money in your checking account, the decision is already made. That is not just a behavioral finance trick. It reflects a genuine Islamic principle: binding your wealth to its purpose before desire can redirect it.

What I find most encouraging about the current state of halal fintech apps is that the compliance infrastructure is finally catching up to the automation infrastructure. AI-driven Shariah screening means that new products can be verified faster, and families can trust the tools they use. That trust matters. You should not have to choose between convenience and your deen.

The one thing I would caution against is treating automation as a replacement for engagement. Review your goals every quarter. Recalculate your sinking funds when costs change. Automation is a tool for discipline, not a substitute for it. The families who build real wealth through halal savings are the ones who combine the system with the intention behind it.

— Imran

Amanahfund: halal budgeting built for Muslim families

Amanahfund’s Amanah Budget app is built specifically for Muslim families who want their financial tools to reflect their values. It includes a zakat calculator, dedicated Hajj and Umrah savings goals, halal-aware spending categories, and AI-powered transaction categorization. You can connect your bank accounts securely through Plaid and share household budgets with your spouse or family members.

For families working through their Hajj savings strategies, Amanahfund provides the structure to set up goal-specific pockets and track progress in one place. No ads. No interest-based products. No selling your data. Just a budgeting app built by Muslims, for Muslims, with your dunya and your deen both in mind.

FAQ

What is an automated halal savings transfer?

An automated halal savings transfer is a scheduled, recurring movement of funds into a Shariah-compliant account such as a Wadiah or Mudarabah account. The transfer happens automatically, typically on payday, without requiring manual action each time.

What is the difference between Wadiah and Mudarabah accounts?

Wadiah accounts safeguard your principal without offering profit, while Mudarabah accounts invest your funds and share profits at a pre-agreed ratio. Choose Wadiah for short-term or emergency savings and Mudarabah for longer-term wealth building.

How do I calculate how much to automate each month?

Use the sinking fund method: divide your total savings goal by the number of months until you need the funds. If you need $6,000 for Umrah in 12 months, automate $500 per month. A budget planner can help you run these calculations accurately.

How many savings goals can I automate at once?

Digital Islamic banking platforms support up to 60 separate sub-accounts or pockets, each receiving its own automated transfer. You can run goals for Hajj, Ramadan, education, and emergencies simultaneously without extra fees.

Do I still need to monitor my accounts after setting up automation?

Yes. Periodic manual rebalancing is necessary to keep your asset allocation aligned with your goals and Shariah compliance requirements, especially for Mudarabah accounts where profit-sharing returns can shift your allocation over time.

Recommended

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account