What Is an FSA Spending Account? 2026 Guide

TL;DR:

- A flexible spending account is an employer-sponsored benefit allowing pre-tax contributions for qualified medical and dependent care expenses, reducing taxable income. Unused funds at year’s end are forfeited unless a grace period or carryover option is available, emphasizing careful planning to avoid losing money. FSAs are short-term, employer-owned accounts best suited for predictable expenses, while HSAs offer long-term, portable savings with investment options.

A flexible spending account (FSA) is a tax-advantaged, employer-sponsored benefit that lets you set aside pre-tax dollars to pay for qualified medical and dependent care expenses. The formal industry term is “flexible spending account,” though many people search for it as an FSA spending account. Either way, the core value is the same: you reduce your taxable income while building a dedicated fund for healthcare costs. The IRS sets the 2026 contribution limit at $3,400 for health care FSAs. One critical rule applies from day one: any unused funds at year-end are forfeited unless your employer offers a grace period or carryover option.

What is an FSA spending account and how does it work?

An FSA is established by your employer, not by you directly. You elect a contribution amount during your company’s open enrollment period, and that amount is deducted from your paycheck in equal pre-tax installments throughout the year.

Here is the part most people miss: for a health care FSA, your full elected amount is available on day one of the plan year, even before your payroll deductions have accumulated. If you elect $2,000 and need a $1,500 dental procedure in January, you can pay for it immediately. A dependent care FSA works differently. Reimbursements from that account are limited to the amount you have actually contributed through payroll at the time of the claim.

Who qualifies for an FSA?

Eligibility is straightforward. You must work for an employer that offers an FSA as part of its benefits package. Self-employed individuals do not qualify. Once enrolled, the account covers qualified expenses for you, your spouse, and your dependents, including adult children up to age 26.

Key eligibility points:

- You must be an employee of a company that sponsors an FSA plan

- You enroll only during open enrollment or after a qualifying life event

- No specific health plan type is required, unlike a Health Savings Account (HSA)

- Your spouse and dependents can use the funds even if they are not on your health insurance plan

- Contribution elections are locked for the plan year; changes require a qualifying life event such as marriage or the birth of a child

What can an FSA pay for?

An FSA covers a wide range of qualified medical and dependent care expenses as defined by the IRS. Your employer may impose additional restrictions beyond the IRS list, so always confirm with your plan administrator before assuming an expense qualifies.

Qualified health care FSA expenses include:

- Doctor visit copays and deductibles

- Prescription medications

- Dental care including cleanings, fillings, and orthodontia

- Vision care including eye exams, glasses, and contact lenses

- Over-the-counter medications and first aid supplies

- Mental health services and therapy sessions

- Medical equipment such as blood pressure monitors and crutches

Dependent care FSA expenses cover costs that allow you and your spouse to work or look for work:

- Licensed daycare centers and in-home childcare

- Before and after-school programs

- Summer day camps (not overnight camps)

- Elder care for a dependent parent who lives with you

Employers may impose plan-specific restrictions beyond what the IRS permits, and some treatments require a medical necessity letter before reimbursement is approved. Cosmetic procedures, gym memberships, and most supplements do not qualify under standard IRS rules.

FSA contribution limits, rules, and timing options

Understanding the financial rules of an FSA protects you from losing money. The IRS sets firm annual limits, and your employer controls which flexibility options, if any, are available to you.

| FSA Type | 2026 Contribution Limit | Key Rule |

|---|---|---|

| Health Care FSA | $3,400 per employee | Full amount available on day one |

| Dependent Care FSA | $7,500 per household | Reimbursement limited to accumulated funds |

| Dependent Care FSA (married, filing separately) | $3,750 per person | Same reimbursement rule applies |

| Health Care FSA Carryover | $680 maximum | Employer must opt in; cannot combine with grace period |

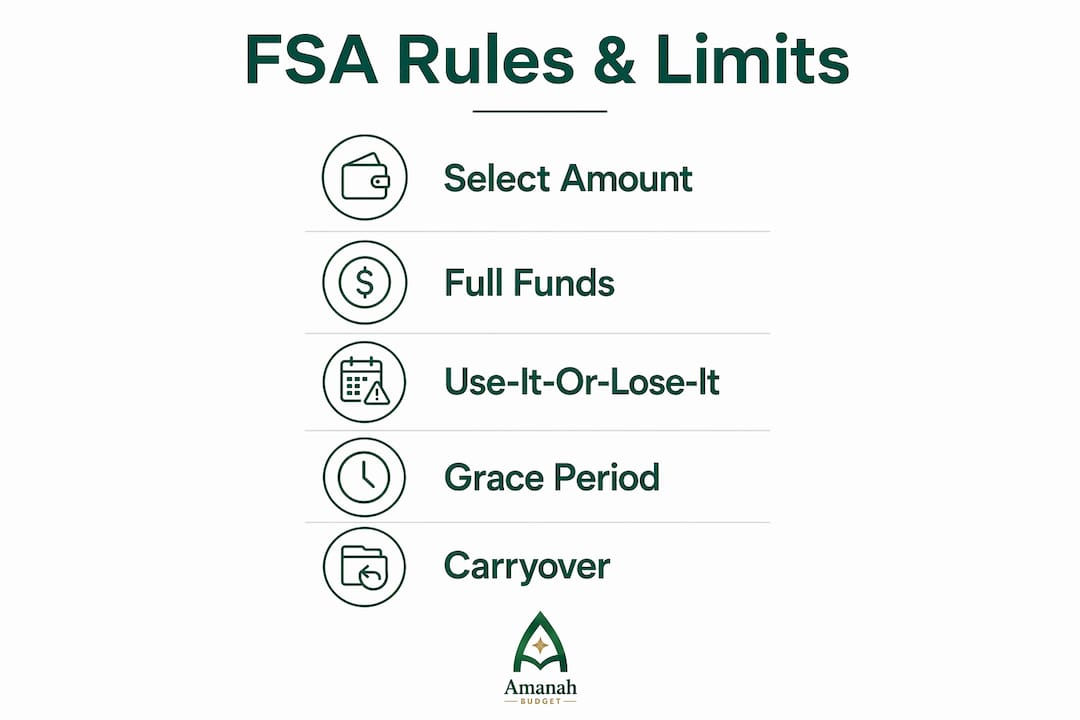

The use-it-or-lose-it rule means any funds remaining in your health care FSA at year-end are forfeited back to your employer. This is the most misunderstood feature of FSAs, and it is the reason careful planning matters.

Employers have two options to soften this rule, but they can only choose one or neither:

Grace period: Your employer extends the spending deadline by 2.5 months into the new plan year. You have until mid-March to spend funds from the prior year.

Carryover: You roll over up to $680 of unused funds into the next plan year. The carryover limit for 2026 funds carried into 2027 is $680.

Neither option is mandatory. Some employers offer no relief at all. Check your Summary Plan Description or ask your HR department before the plan year begins.

Pro Tip: Set a calendar reminder for November 1 each year to review your FSA balance and schedule any remaining qualified expenses before the deadline. Dental cleanings, new glasses, and prescription refills are easy ways to spend down a balance before year-end.

How does an FSA compare to an HSA?

FSAs and HSAs are both tax-advantaged accounts for healthcare expenses, but they serve different purposes and come with different rules. Choosing the wrong one for your situation costs you flexibility and money.

| Feature | Health Care FSA | Health Savings Account (HSA) |

|---|---|---|

| Ownership | Employer-owned | Employee-owned |

| Portability | Forfeited if you leave the employer | Stays with you permanently |

| Health plan requirement | None | Requires a high-deductible health plan (HDHP) |

| Rollover | Up to $680 or 2.5-month grace period | Unlimited rollover, grows indefinitely |

| Investment growth | None | Funds can be invested tax-free |

| Contribution flexibility | Fixed at enrollment | Can adjust anytime during the year |

The key ownership difference is the most consequential. An FSA belongs to your employer. If you leave your job, you lose access to any remaining FSA funds. An HSA belongs to you and follows you to every future employer and into retirement.

FSAs are best for employees who have predictable, near-term medical expenses and want to reduce their tax bill now. HSAs are better for employees on high-deductible plans who want to build long-term tax-free savings. The two accounts are not interchangeable, and you generally cannot hold both a health care FSA and an HSA at the same time.

How to maximize your FSA benefits

Getting the most from your FSA requires honest planning before the year starts and consistent tracking throughout. Overestimating your contributions leads to forfeited funds, which is the most common FSA mistake.

Start by reviewing your medical expenses from the prior year. Add up what you spent on prescriptions, copays, dental work, and vision care. Use that number as your baseline estimate for the coming year. If you have a planned procedure or expect a baby, factor those costs in.

Practical steps to maximize your FSA:

- Estimate conservatively. It is better to contribute slightly less and avoid forfeiture than to overestimate and lose money.

- Use the front-loaded benefit. Schedule large planned expenses early in the year to take advantage of the full balance being available on day one.

- Know your employer’s relief option. Confirm whether your plan offers a grace period or carryover before you finalize your election.

- Keep every receipt. The IRS requires documentation for FSA reimbursements. Store receipts digitally to avoid losing them.

- Track your balance monthly. Knowing your balance prevents end-of-year surprises.

Pro Tip: Using an expense tracking app to log medical spending throughout the year gives you a clear picture of your FSA usage and helps you avoid the year-end scramble.

The average U.S. household spent $6,197 on healthcare in 2024. That figure gives you a useful benchmark when deciding how much to contribute. Pre-tax FSA contributions typically save 20%–40% depending on your tax bracket, which means a $3,000 contribution could save you $600–$1,200 in taxes.

Key takeaways

An FSA spending account is one of the most underused tax benefits available to employees, and the use-it-or-lose-it rule is the only reason it stays that way.

| Point | Details |

|---|---|

| FSA definition | A pre-tax employer-sponsored account for qualified medical and dependent care expenses. |

| 2026 contribution limits | $3,400 for health care FSAs; $7,500 per household for dependent care FSAs. |

| Use-it-or-lose-it rule | Unused funds are forfeited unless your employer offers a grace period or up to $680 carryover. |

| FSA vs. HSA | FSAs are employer-owned and short-term; HSAs are portable, investment-capable, and long-term. |

| Maximize your FSA | Estimate conservatively, schedule large expenses early, and track spending monthly to avoid forfeiture. |

Why fsas deserve more attention than they get

I have watched a lot of people leave real money on the table with FSAs, not because the accounts are complicated, but because they set their contribution in October and never think about it again until March when it is too late.

The most common misconception I see is treating an FSA like a savings account. It is not. It is a spending account with a deadline. The moment you start thinking of it that way, your whole approach changes. You plan your dental appointments, you refill prescriptions on schedule, and you buy the glasses you have been putting off.

The second thing people get wrong is ignoring their employer’s specific plan rules. The IRS sets the outer boundaries, but your employer fills in the details. I have seen plans that exclude certain over-the-counter items the IRS allows, and I have seen plans with no grace period or carryover at all. Reading your Summary Plan Description once a year takes 20 minutes and can save you hundreds of dollars.

For Muslim families especially, an FSA fits naturally into the principle of thoughtful stewardship of resources. Setting aside money intentionally for healthcare, avoiding waste, and planning ahead are all expressions of responsible financial management. Pairing an FSA with a solid family financial plan makes the whole system work better.

My honest advice: review your FSA election every single year. Contribution limits change, your health needs change, and your employer’s plan options may change. Treat it as an annual financial task, not a one-time setup.

— Imran

Plan your healthcare budget with Amanahfund

Managing an FSA well is really a budgeting challenge. You need to estimate annual expenses accurately, track spending throughout the year, and act before deadlines. Amanahfund is built to support exactly that kind of intentional financial planning.

Amanahfund’s halal-first budgeting tools help Muslim families track healthcare spending, plan for annual expenses, and manage household budgets with values built into every feature. Whether you are coordinating FSA spending across a family or planning for Hajj savings alongside medical costs, Amanahfund keeps your full financial picture in one place. Explore how Amanahfund supports your family’s financial wellness with tools designed around your deen and your dunya.

FAQ

What is an FSA spending account used for?

An FSA spending account pays for qualified medical expenses including copays, prescriptions, dental, vision, and over-the-counter items. Dependent care FSAs cover childcare and elder care costs that allow you to work.

Who qualifies for an FSA account?

Any employee whose employer offers an FSA plan qualifies. Self-employed individuals are not eligible, and no specific health insurance plan type is required to open a health care FSA.

What happens to unused FSA funds at year-end?

Unused funds are forfeited under the use-it-or-lose-it rule. Your employer may offer either a 2.5-month grace period or a carryover of up to $680, but is not required to offer either.

Can i change my FSA contribution during the year?

No. Contribution elections are fixed for the plan year once open enrollment closes. The only exception is a qualifying life event such as marriage, divorce, or the birth of a child.

What is the difference between an FSA and an HSA?

An FSA is employer-owned, requires no specific health plan, and has limited rollover. An HSA is employee-owned, requires a high-deductible health plan, and accumulates indefinitely with no forfeiture risk.

Recommended

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account