The Role of Niyyah in Spending: An Islamic Guide

TL;DR:

- Niyyah is the internal conscious intention behind each financial action, transforming spending into worship or mere habit. It influences whether transactions like zakat or support are spiritually rewarding, depending on heart orientation rather than outward form. Incorporating niyyah through daily renewal and mindful categorization aligns financial decisions with Islamic values, enhancing spiritual accountability and reward.

Niyyah is defined as the conscious intention behind an action, and its role in spending is to transform every financial decision into either an act of worship or a missed opportunity for spiritual reward. In Islamic finance, the distinction between a routine purchase and a rewarded deed rests entirely on the intention held in the heart. Classical scholars from the Hanafi, Maliki, Shafi’i, and Hanbali schools all affirm that niyyah is the condition that determines whether a financial act earns divine acceptance. Understanding the role of niyyah in spending is not an abstract theological exercise. It is a practical framework that shapes how Muslims budget, give zakat, spend on family, and evaluate every transaction.

How does niyyah shape financial decisions in Islamic jurisprudence?

Classical Islamic jurisprudence treats niyyah as the foundational condition for any deed to carry spiritual weight. Intention is the essential condition for acts to be accepted, including financial actions like giving zakat or earning halal income. Without it, the same physical act of handing over money is either worship or mere habit.

Scholars define niyyah as an internal heart orientation, known in Arabic as qasd. Niyyah is the brief internal awareness before an act, not a fixed verbal recitation. You do not need to say anything aloud. The conscious awareness in your heart before you spend is sufficient and, in fact, is what counts.

This principle has direct consequences for financial life. Paying zakat with the intention of fulfilling a divine obligation earns full spiritual reward. Paying the same amount without that awareness is a transfer of funds, nothing more. The same logic applies to supporting your family, giving sadaqah, or even spending on lawful necessities. Intention is what separates the mundane from the meaningful.

Prophetic tradition reinforces this. The hadith recorded by Imam al-Bukhari and Imam Muslim states that actions are judged by intentions, and every person receives what they intended. This is not a peripheral teaching. It is one of the most foundational principles in Islamic ethics, and it applies directly to how you manage your money.

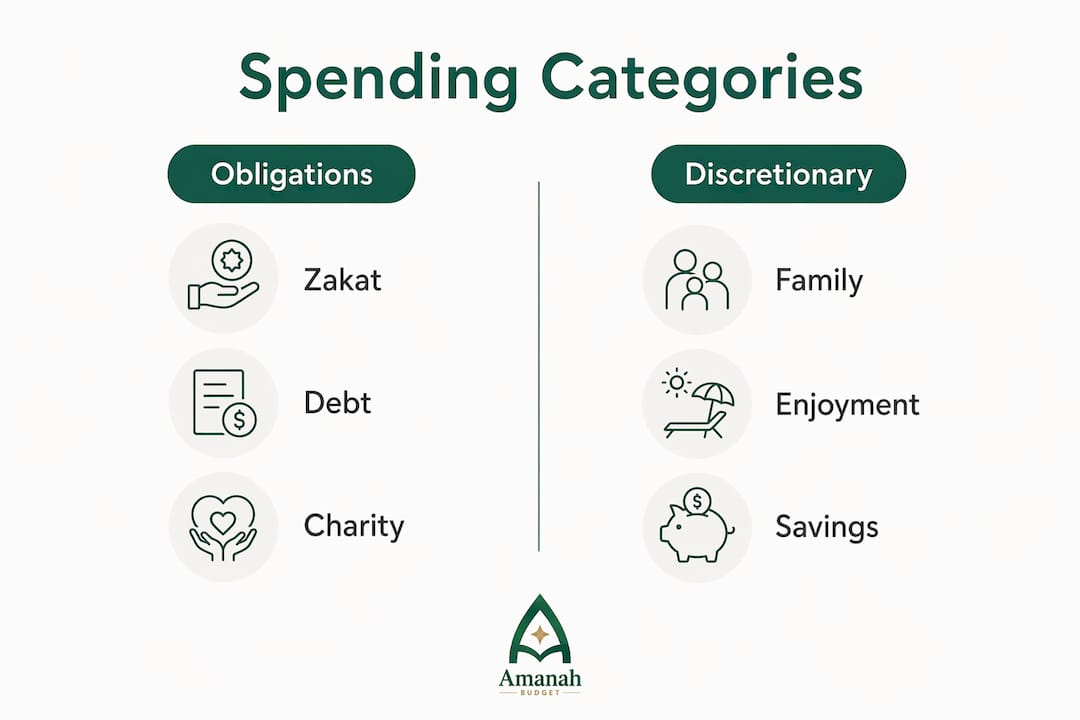

Islamic spending categories shaped by intention

Modern Islamic financial mindfulness organizes spending into categories defined by both function and intent. Spending categories focused on intention prioritize obligations and charity over discretionary expenses. Understanding where each dollar falls helps you spend with awareness rather than autopilot.

| Spending Category | Examples | Intention Consideration |

|---|---|---|

| Obligations | Zakat, debt repayment | Must be fulfilled with conscious niyyah for full reward |

| Halal necessities | Food, housing, medical care | Intention to maintain health and fulfill family duties |

| Halal discretionary | Vacations, hobbies, dining out | Permissible with sincere intention; avoid israf and riya |

| Charity beyond zakat | Sadaqah, sponsoring orphans | Highest reward when given sincerely for Allah’s pleasure |

| Items requiring review | Subscriptions, entertainment | Requires honest self-examination of purpose and benefit |

The framework of muhasaba, or spiritual self-accounting, is the tool scholars recommend for auditing your spending against these categories. Regular self-review of spending with spiritual criteria helps maintain financial discipline and alignment with Islamic values. Muhasaba is not guilt. It is honest reflection, asking yourself whether your spending reflects your stated values.

Two markers guide this review: ma’ash, which refers to your worldly living needs, and ma’ad, which refers to your return to Allah and your preparation for the hereafter. Spending that serves both markers simultaneously, such as feeding your family with the intention of fulfilling your duty to them and to Allah, earns reward on both dimensions.

Avoiding israf (wasteful spending) and riba (interest-based transactions) are non-negotiable boundaries. Islamic financial mindfulness uses muraqabah to avoid riba and israf, assessing spending through these spiritual criteria. Muraqabah means self-observation with the awareness that Allah sees every transaction.

Pro Tip: Before categorizing a purchase, ask yourself one question: “Am I spending this to fulfill a need, serve my family, or please Allah?” If the honest answer is yes, you are in the right category. If the answer is unclear, that is your signal to pause.

Can discretionary spending be an act of worship?

Discretionary spending is permissible and can earn spiritual reward when the intention is sincere and the spending is reasonable. This corrects a common misconception that enjoyment is inherently wasteful for a Muslim. Spending on lawful enjoyment is permissible and can be rewarded if the intention is pleasing Allah and spending avoids riya and israf.

The key distinction is between riya (showing off) and sincere intention. Buying a quality meal for your family with the intention of honoring them and maintaining their health is worship. Buying the same meal to impress others or to signal status is riya, which strips the act of its reward. The external action is identical. The internal orientation determines the outcome.

Scholars also clarify that reasonable spending is not a fixed dollar amount. Intention acts as a dynamic internal filter defining reasonable spending by context, income, need, and moderation. A family earning $40,000 annually and a family earning $200,000 annually will have different thresholds for what constitutes moderation. Niyyah guides you to assess your own context honestly.

Here are practical ways to maintain sincere intention during discretionary spending:

- Renew your intention before each purchase. A brief moment of awareness before you spend is all that is required. Ask whether this purchase serves a lawful purpose.

- Check for riya. If the primary motivation is how others will perceive you, reconsider the purchase or recalibrate your intention.

- Apply the moderation test. Would a reasonable, God-conscious Muslim in your income bracket consider this excessive? If yes, scale back.

- Connect spending to gratitude. Spending on lawful enjoyment with gratitude to Allah for the provision transforms the act into acknowledgment of His blessing.

Pro Tip: When making a larger discretionary purchase, write down your intention beforehand. This simple act of articulating your niyyah in a journal or notes app makes the internal orientation conscious and deliberate, which is exactly what classical scholars describe as the heart of the practice.

Practical steps to integrate niyyah into daily budgeting

Applying intention in financial decisions requires structure, not just goodwill. Spiritual budgeting skills include daily niyyah renewal, mindful questioning of purchases, and reviewing budgets with Islamic values in mind. Here is a practical framework you can follow.

-

Begin each day with a renewed intention for your finances. Before you check your bank account or make any transaction, take a moment to state internally that your financial management today is an act of stewardship over the amanah (trust) Allah has given you.

-

Ask three questions before every non-routine purchase. First: Is this halal? Second: Is this necessary or excessive given my circumstances? Third: What is my honest motivation for this purchase? These questions take seconds and create a habit of mindful spending.

-

Categorize your monthly budget by intention, not just function. Separate your obligations from your discretionary spending. Label your zakat line as an act of worship. Label your family food budget as fulfilling your duty of care. This reframing, as described in Islamic spending accountability, turns budgeting into a spiritual audit rather than a spreadsheet exercise.

-

Conduct a monthly Islamic budget review. At the end of each month, review your spending against your stated intentions. Did your discretionary spending reflect your values? Did you fulfill your obligations? The Amanah Budget blog’s guide on reviewing your budget Islamically offers a structured approach to this practice.

-

Use tools built for this purpose. Generic budgeting apps do not recognize zakat, sadaqah, or Hajj savings as distinct categories. Amanahfund’s Amanah Budget app is built with halal-aware spending categories, a zakat calculator, and savings goals for Hajj and Umrah. These features make intention-aligned budgeting practical rather than theoretical.

Sustaining intention until completion of financial acts is recommended and linked to greater reward in Islamic worship practices. This means your niyyah is not a one-time event at the start of a transaction. Renewing it throughout a financial act, such as during a month of consistent zakat savings, deepens the spiritual benefit.

Key Takeaways

Niyyah transforms every financial act into worship when the intention is sincere, the spending is lawful, and the purpose aligns with seeking Allah’s pleasure.

| Point | Details |

|---|---|

| Niyyah is internal, not verbal | The conscious heart orientation before spending is what earns spiritual reward, not a spoken phrase. |

| Spending categories reflect intention | Obligations, necessities, discretionary, and charity each carry different intention requirements and spiritual weight. |

| Discretionary spending can be worship | Lawful enjoyment earns reward when intention is sincere and spending avoids riya and israf. |

| Reasonable spending is context-dependent | Niyyah acts as a personal filter for moderation based on income, need, and circumstance. |

| Daily renewal strengthens practice | Renewing intention before and during financial acts deepens spiritual reward and financial mindfulness. |

Why I think most Muslims underestimate niyyah in their finances

Most conversations about Islamic finance focus on what is prohibited: riba, haram industries, speculative investments. Those boundaries matter. But the deeper transformation comes from what niyyah does to the permissible. I have seen families who avoid every haram transaction but still feel spiritually disconnected from their money. The missing piece is almost always intention.

When I shifted from thinking about my budget as a restriction tool to thinking about it as a record of my stewardship before Allah, everything changed. Paying the electric bill became an act of providing shelter for my family. Buying groceries became fulfilling the duty of care. None of these acts changed externally. The intention behind them changed everything internally.

The harder challenge is consistency. Renewing niyyah daily requires discipline. There will be months where you spend on autopilot and only realize it during your monthly review. That is not failure. That is exactly what muhasaba is for. The Islamic view on wealth tracking frames this accountability not as judgment but as honest stewardship.

Wealth is an amanah. You did not earn it alone, and you will be asked about how you used it. That awareness, held sincerely in the heart before every financial decision, is niyyah in its most practical form.

— Imran

Start budgeting with intention using Amanahfund

Knowing the principles of niyyah in spending is the first step. Applying them consistently requires tools that speak your language.

Amanahfund’s Amanah Budget app is built specifically for Muslim families who want their financial tools to reflect their values. It includes halal-aware spending categories, a zakat calculator that supports multiple madhabs, and dedicated savings goals for Hajj, Umrah, Ramadan, and Eid. Every feature is designed to support intention-aligned budgeting from day one. No ads, no interest-based products, and no selling your data. If you are ready to turn your halal budgeting practice into a daily act of worship, Amanah Budget is built for exactly that.

FAQ

What does niyyah mean in the context of spending?

Niyyah means the conscious intention held in the heart before a financial act. In spending, it is the internal awareness of why you are making a purchase and whether it aligns with seeking Allah’s pleasure.

Does niyyah need to be spoken aloud before a financial transaction?

No. Niyyah is an internal heart orientation, not a verbal formula. The conscious awareness before the act is sufficient for it to count as an intention in Islamic jurisprudence.

Is spending on personal enjoyment considered wasteful in Islam?

Not when the intention is sincere and the spending is moderate. Spending on lawful enjoyment is permissible and can earn reward if it avoids riya (showing off) and israf (excess).

How can I apply niyyah to my monthly budget?

Categorize your spending by intention rather than just function, renew your intention daily before financial decisions, and conduct a monthly review using Islamic values as your criteria. Tools like Amanahfund’s Amanah Budget app support this process with halal-aware categories built in.

What is the difference between israf and reasonable discretionary spending?

Israf is spending that exceeds genuine need without a lawful purpose, while reasonable discretionary spending is proportionate to your income and serves a lawful benefit. Intention acts as a personal filter that defines the boundary based on your specific context and circumstances.

Recommended

- Spending Accountability in Islam: A 2026 Guide — Amanah Budget Blog

- The Role of Deen in Family Finances: A Muslim Guide — Amanah Budget Blog

- The Role of Deen in Family Finances: A Muslim Guide — Amanah Budget Blog

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account