The Role of Husband and Wife in an Islamic Budget

TL;DR:

- In Islamic marriage, the husband is legally responsible for providing housing, food, clothing, and healthcare, regardless of the wife’s income.

- The wife maintains full ownership of her earnings and is not required to contribute to household expenses unless voluntarily chosen, emphasizing her financial independence.

The role of husband and wife in an Islamic budget is defined by a clear legal framework: the husband bears a binding financial obligation to provide for the family, while the wife’s income remains exclusively hers. This principle, known as nafaqah, is not a cultural custom. It is a structured part of Islamic family law recognized across all four major madhabs. Understanding these distinct roles is the first step toward building a household budget that reflects both your deen and your practical financial reality.

What are the husband’s financial responsibilities in Islam?

The husband’s financial obligation under nafaqah covers housing, food, clothing, and reasonable healthcare for his wife and children. This obligation holds regardless of the wife’s income or wealth. A wife who earns more than her husband still retains her full right to nafaqah. That is not a technicality. It is a deliberate protection built into Islamic law.

The rationale behind nafaqah is rooted in the concept of dhimmah, which treats each spouse as a separate economic entity. Marriage in Islam does not merge assets or liabilities. The husband manages household expenses as a financial steward, not as the sole owner of family wealth. This distinction matters enormously when couples sit down to build a budget together.

The husband’s core financial duties include:

- Housing: A private, safe dwelling appropriate to the family’s standard of living

- Food: Regular meals for the wife and children

- Clothing: Seasonal and appropriate clothing for the household

- Healthcare: Reasonable medical expenses for the wife and children

- Education: Basic educational needs for children fall within the scope of nafaqah in most scholarly opinions

Pro Tip: Before setting a household budget, the husband should calculate the full cost of nafaqah obligations first. These are non-negotiable line items, not optional contributions. Treat them as fixed expenses before allocating anything else.

Does the wife have to contribute to household expenses?

The wife has no religious or legal obligation to contribute her income to household expenses. Her earnings are fully her own, and marriage does not change that. Any contribution she makes is an act of generosity, not a duty. Scholars across the Hanafi, Maliki, Shafi’i, and Hanbali schools agree on this point.

This is one of the most misunderstood aspects of financial roles in marriage Islam. Many couples, especially in dual-income households, assume that both spouses must split bills equally. That assumption has no basis in Islamic law. A wife who chooses to pay for groceries or utilities is doing something praiseworthy. But she cannot be pressured, expected, or guilted into it.

A few key principles that govern the wife’s financial role:

- Her income, savings, and investments belong to her alone

- She may choose to contribute to shared expenses voluntarily

- Voluntary contributions must not be weaponized in marital power dynamics

- If she contributes, it does not reduce her right to nafaqah

- Her financial independence is a protection, not a privilege to be negotiated away

Recognizing this reality actually reduces financial resentment in many marriages. When both spouses understand that her contribution is a gift rather than an obligation, it shifts the dynamic from obligation to cooperation.

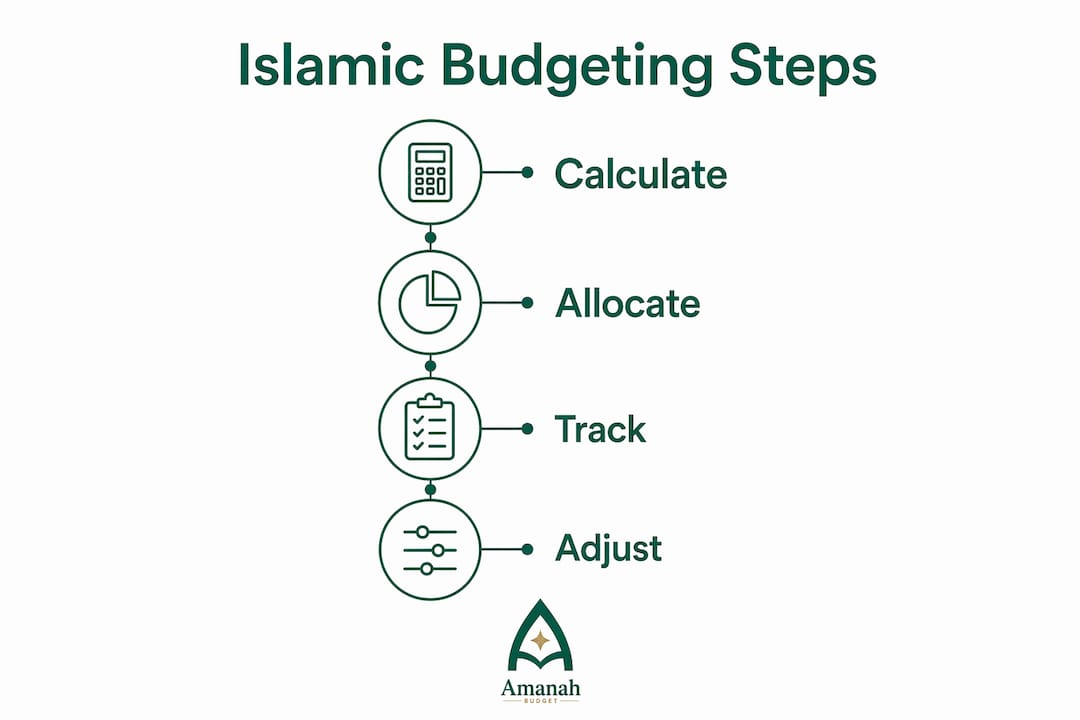

Practical Islamic budgeting frameworks for couples

The three-account model is the most practical structure for Muslim couples. It keeps individual assets separate per Islamic law while supporting shared household management. Each spouse maintains a personal account, and both contribute to a joint account for shared household costs. This structure also makes zakat calculation cleaner, since each spouse’s individual wealth is tracked separately.

A halal budget structure should prioritize expenses in this order:

| Category | Allocation Guidance |

|---|---|

| Nafaqah (necessities) | 50–60% of household income |

| Zakat | 2.5% of qualifying wealth above nisab |

| Debt repayment | Prioritized after necessities |

| Savings and emergency fund | 10–15% of income; start with a $1,000 buffer |

| Sadaqah and charity | Fixed budget item, not ad hoc giving |

Families should allocate 50–60% of income to necessities and 10–15% to savings and debt repayment. Zakat sits at 2.5% on qualifying wealth held above nisab for one full lunar year. Treating zakat as a fixed budget line rather than a year-end surprise prevents the last-minute scramble that many families experience in Ramadan.

Experts recommend tracking combined spending for 30 days before setting any budget goals. That baseline reveals actual spending patterns rather than assumed ones. Couples often discover that their real spending on food, transportation, or subscriptions differs significantly from what they estimated.

Pro Tip: Assign budget categories based on skills and availability, not gender. If the wife is better at tracking grocery spending, she manages that category. If the husband handles utility payments, he owns that line. Distributed management based on competence, not tradition, produces better results.

For a detailed walkthrough of setting up your household categories, the family halal budget setup guide from Amanahfund covers the full structure from necessities to savings goals.

How can couples manage financial decision-making effectively?

Shura, the Islamic principle of mutual consultation, is the foundation of sound financial decision-making in marriage. Monthly financial meetings prevent resentment and keep spending aligned with shared values. These meetings do not need to be formal. A 30-minute review of the joint account, upcoming expenses, and zakat obligations is enough.

Effective financial communication between spouses includes:

- Review the joint account together at the start of each month

- Discuss upcoming large expenses such as school fees, medical bills, or travel

- Confirm zakat obligations and set aside funds throughout the year rather than calculating at the last minute

- Revisit savings goals for Hajj, Umrah, Eid, or emergencies

- Address any disagreements about spending before they become patterns

Pre-marriage financial habits predict post-marriage financial harmony more reliably than income levels. Couples who discuss budgets, obligations, and financial values before marriage experience fewer conflicts afterward. If that conversation did not happen before the nikah, it is worth having now.

Financial control is a form of harm in Islamic ethics. A husband who withholds nafaqah or a wife who uses her voluntary contributions as leverage both violate the spirit of the marital contract. For practical guidance on resolving disagreements when they arise, Amanahfund’s resource on resolving budgeting disagreements offers concrete steps grounded in Islamic principles.

Common budgeting challenges and how Islamic principles guide solutions

Muslim couples face specific financial tensions that generic budgeting advice does not address. Islamic principles provide clear guidance for each one.

-

Misunderstanding nafaqah scope. Some husbands underestimate what nafaqah covers, leading to resentment when wives expect more. Reviewing the full scope of nafaqah obligations together removes ambiguity and sets fair expectations.

-

Dual-income disparities. When one spouse earns significantly more, resentment can build if contributions feel unequal. The Islamic framework resolves this cleanly: the husband covers necessities, and any additional contribution from either spouse is voluntary and appreciated, not expected.

-

Ad hoc zakat and charity. Many families give zakat at 2.5% only when prompted, rather than planning for it throughout the year. Setting aside a small monthly amount toward the annual zakat obligation prevents financial strain in Ramadan. Understanding the difference between zakat and sadaqah also helps couples plan their charitable giving with intention rather than impulse.

-

Niyyah in spending. Intention matters in Islamic ethics. Couples who frame their budget as an act of worship, not just financial management, make more consistent and values-aligned decisions. Viewing wealth as a trust from Allah, rather than personal property to protect, shifts the entire dynamic of how couples budget in Islam.

Key takeaways

The husband’s nafaqah obligation and the wife’s financial independence are the two fixed pillars of Islamic budgeting for couples. Every practical framework builds from these two principles.

| Point | Details |

|---|---|

| Husband’s nafaqah is binding | Covers housing, food, clothing, and healthcare regardless of the wife’s income. |

| Wife’s income is fully hers | No obligation to contribute to household expenses; any contribution is voluntary. |

| Three-account model works best | Joint account for shared costs plus separate personal accounts preserves Islamic asset separation. |

| Zakat needs intentional planning | Set aside funds monthly to meet the 2.5% obligation without a last-minute scramble. |

| Shura prevents financial conflict | Monthly financial meetings keep both spouses aligned and reduce resentment. |

Why I think most Muslim couples get the financial roles backwards

Most couples I have seen struggle with money in marriage are not struggling because of income. They are struggling because they never clearly defined who owes what to whom. The husband assumes the wife will split bills. The wife assumes the husband will cover everything. Neither assumption is fully correct, and neither spouse has read the actual framework their faith provides.

The Islamic model is genuinely sophisticated. It protects the wife’s financial independence in a way that most modern legal systems still do not fully replicate. A wife in an Islamic marriage has a legal claim to her husband’s provision that exists independently of her own wealth. That is not a burden on the husband. It is a structure that removes the financial anxiety that plagues so many marriages.

What I have found is that couples who treat wealth as an amanah, a trust from Allah, stop fighting over money. They start managing it together. The budget becomes a shared act of stewardship rather than a negotiation over who pays for what. That mindset shift is more powerful than any spreadsheet or app. But the tools help too, especially when they are built around the values you already hold.

— Imran

Amanahfund: built for the way Muslim families actually budget

Muslim families need budgeting tools that understand nafaqah, zakat, and halal spending categories from the start. Generic apps do not account for any of that.

Amanahfund is a halal-first budgeting app built specifically for Muslim families. Couples can share a household budget, track spending with halal-aware categories, calculate zakat using their preferred madhab, and save intentionally for Hajj, Umrah, Ramadan, and Eid. Bank accounts connect securely through Plaid, and AI-assisted categorization keeps transactions organized without manual entry. No ads. No interest-based products. No selling of user data. For families ready to manage their household halal spending with their values intact, Amanahfund is the practical next step. Visit Amanahfund to get started.

FAQ

What is nafaqah in Islamic marriage?

Nafaqah is the husband’s binding legal obligation to provide his wife and children with housing, food, clothing, and healthcare. This obligation holds regardless of the wife’s income or financial status.

Does a working wife lose her right to financial support?

No. A wife who earns her own income retains her full right to nafaqah. Her husband’s obligation to provide does not decrease because she works.

Is the wife required to contribute to household expenses in Islam?

The wife has no religious or legal obligation to contribute her income to household expenses. Any contribution she makes is voluntary and should never be treated as an expectation or used as leverage.

What is the best budgeting structure for Muslim couples?

The three-account model works best: a joint account for shared household costs and separate personal accounts for each spouse. This preserves Islamic asset separation and simplifies zakat calculation.

How should Muslim couples handle zakat in their budget?

Zakat is 2.5% of qualifying wealth held above nisab for one full lunar year. Couples should set aside funds monthly throughout the year rather than calculating the full amount at the last minute during Ramadan.

Recommended

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- How Muslim couples can resolve budgeting disagreements — Amanah Budget Blog

- How Muslim couples can resolve budgeting disagreements — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account