The Role of Deen in Family Finances: A Muslim Guide

Many Muslim families separate their faith from their finances without realizing it. They pray, fast, and give to charity, yet when it comes to budgeting, saving, or making spending decisions, those choices happen in a different mental space. The role of deen in family finances is far more pervasive than most people recognize. Islamic teachings touch every dimension of money: how it is earned, how it is spent, how it is shared, and how much is enough. Understanding this connection does not just make you a better Muslim. It makes you a more grounded, clear-headed financial decision-maker.

Table of Contents

- Key Takeaways

- The role of deen in family finances starts here

- Translating Islamic values into daily budgeting

- Amanah and shared household financial responsibility

- Common pitfalls in family finances from an Islamic lens

- Practical steps for halal saving, investing, and planning

- My perspective: faith and finances cannot be separated

- Manage your family finances the halal-first way

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Deen governs all money decisions | Islamic principles shape how you earn, spend, save, and give, not just how you avoid riba. |

| Barakah depends on method and intention | Halal income with gratitude and moderation brings more stability than a larger income earned carelessly. |

| Amanah means shared family responsibility | Treating finances as a collective trust strengthens resilience and consistency in zakat and savings. |

| Budgeting is an act of worship | Tracking expenses and setting value-based priorities is a spiritual discipline, not just a practical one. |

| Pitfalls go beyond haram income | Overspending, showing off, and skipping zakat all erode barakah even when income itself is halal. |

The role of deen in family finances starts here

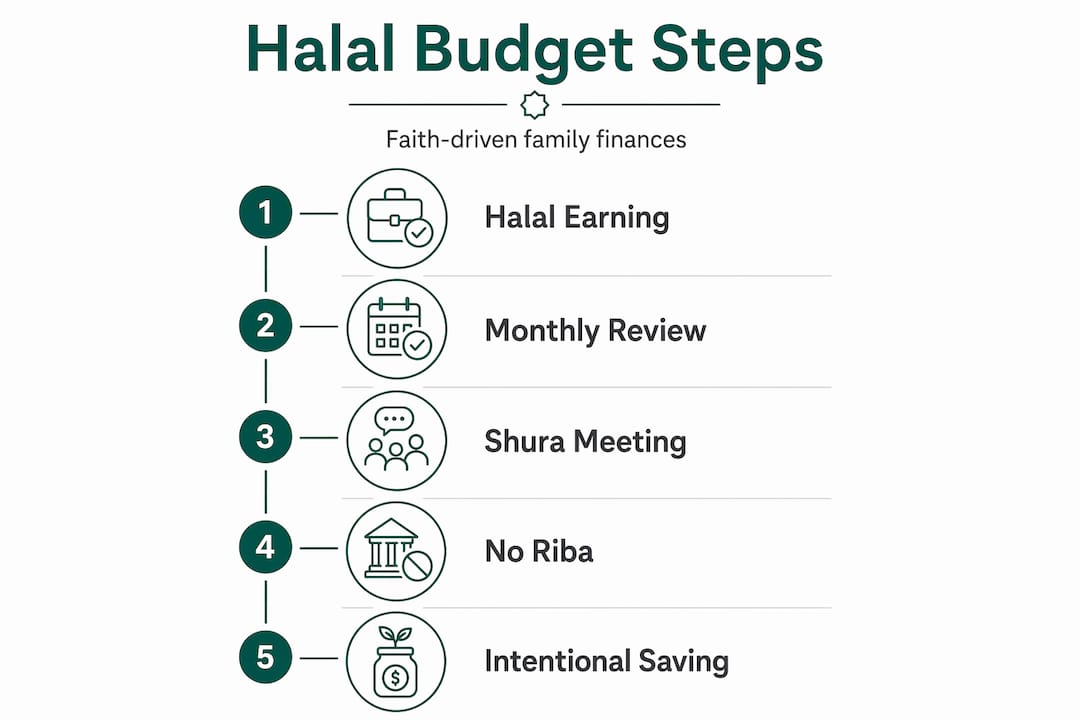

Most conversations about Islamic finance start and end with one word: riba. Avoiding interest-based loans matters deeply, and that prohibition is real. But Islamic financial planning actually involves six interconnected practices: earning halal income, tracking expenses, building value-based budgets, paying zakat regularly, saving consistently, and investing according to Sharia principles. Each one reinforces the others.

The foundation is halal earning. Wealth that comes from permissible sources carries barakah, which translates loosely as divine blessing or increase. The Quran and the Sunnah are explicit that barakah in wealth depends more on earning with gratitude and moderation than on the total amount accumulated. A smaller, clean income often brings more peace than a larger one built on compromise.

Israf, meaning extravagance or wastefulness, is the counterbalance to halal earning. The Prophet ﷺ warned against spending beyond one’s means and rewarded moderate spending for family within reasonable limits. Israf is not only about luxury goods. It includes buying more than you need, spending to impress others, and neglecting family needs in favor of appearances.

Then there is zakat. This is not a voluntary charitable gesture. Zakat is a mandatory wealth redistribution mechanism that purifies individual wealth while improving social cohesion and reducing inequality. Alongside zakat, sadaqah (voluntary charity) multiplies barakah and keeps the household financially connected to the broader community.

“Financial management is not just dunya but ibadah, enriching faith through mindful money stewardship.” — Halal Money Matters

Pro Tip: Write down the Islamic principles you want to honor financially: halal income, no riba, moderate spending, consistent zakat. Post them somewhere visible. What gets named gets practiced.

Translating Islamic values into daily budgeting

The importance of deen in finances only becomes real when it shapes daily decisions. Theory is not enough. You need a household budget that reflects your actual religious priorities, not just generic expense categories pulled from a mainstream app.

Here is a practical sequence for building a deen-aligned family budget:

- Identify your halal income sources first. Before budgeting a single dollar, clarify that your income streams are permissible. If any income source carries ambiguity, address it before it enters your budget.

- Prioritize family needs over wants. Islamic teachings put family welfare first. Housing, food, healthcare, and education come before discretionary spending, entertainment, or lifestyle upgrades.

- Allocate zakat and sadaqah from the top. Treating charitable giving as a fixed budget line, not a leftover, changes your relationship with money. It is not what you give after your needs are met. It is part of the plan from the start.

- Label your spending categories by value, not just by type. Instead of “dining out,” try “family meals” or “hospitality.” This framing keeps your deen visible in the budget itself.

- Track every expense as a spiritual practice. Budgeting reveals your spiritual state and shows whether your spending aligns with your stated values. A budget that never gets reviewed is just a wish list.

- Build an emergency fund as a fard kifayah. Protecting your family from financial shocks is a collective duty in Islam. Three to six months of expenses in a halal savings vehicle is not overcautious. It is responsible stewardship.

For families navigating halal grocery costs specifically, understanding why those expenses run higher and how to plan for them is part of a realistic halal family budget. Deen and financial planning work together best when the budget reflects real life, not an idealized version of it.

Pro Tip: Review your budget once a month with your spouse or family. Frame it as a shura (consultation) meeting. Shared awareness of household finances builds unity and reduces money-related conflict.

Amanah and shared household financial responsibility

One of the most transformative concepts in Islamic financial ethics is amanah: trust. Your family’s finances are not your private property. They are a trust from Allah, given to you temporarily and meant to be managed with care, transparency, and collective wisdom.

Viewing family finances as a shared trust rather than as individual property increases resilience and makes zakat payment more consistent. When spouses and family members see household wealth as a collective responsibility, they are more likely to protect it, grow it ethically, and give from it generously.

Practically, the amanah mindset changes how families communicate about money:

- Spouses discuss major financial decisions together rather than independently.

- Children learn early that money is a tool for responsibility, not just for consumption.

- Savings goals reflect shared values: Hajj, Umrah, education, and family welfare.

- Zakat is calculated and paid as a household, not an afterthought.

“Collective household financial trust enhances resilience and moral consistency in zakat payment.” — Islamic epistemology and household financial responsibility

The amanah mindset also reduces vulnerability to financial shocks. Families who treat money as a collective trust are less likely to take unilateral risks, accumulate secret debt, or make impulsive purchases that harm the household. When everyone is accountable, everyone is protected.

Planning a long-term religious goal like Hajj is one of the clearest ways to practice this. Saving intentionally as a family, tracking progress together, and staying committed through the ups and downs of household finances all reflect the amanah principle in action. Resources like a step-by-step guide on how to save for Hajj can help families turn this aspiration into a concrete plan.

Common pitfalls in family finances from an Islamic lens

Most Muslims know what to avoid in terms of haram income. Fewer recognize the spiritual and financial dangers that come from halal income managed poorly. Spending halal money unwisely is its own category of failure, and it threatens barakah just as surely as haram earnings do.

Here are the most common pitfalls families face and what Islamic teaching says about each:

- Mixing halal and haram income. Even a small haram stream contaminates the blessing in the whole. This applies to interest earned on conventional savings accounts, income from impermissible businesses, and gifts given with conditions that involve wrongdoing.

- Skipping or delaying zakat. Missing zakat is not just a financial oversight. It is a spiritual one. Zakat purifies wealth, and its absence leaves the household’s finances in an impure state. Challenges like poor tracking and unclear nisab calculations are real but solvable.

- Israf disguised as generosity. Hosting lavish gatherings, buying expensive gifts to maintain status, or spending extravagantly at weddings can feel culturally justified. From an Islamic standpoint, they often reflect riya’ (showing off), not true generosity.

- Ignoring debt discipline. Debt in Islam is taken seriously. Dying in debt is considered a burden. Borrowing beyond your means, especially through interest-based instruments, is a compounding problem that erodes both financial and spiritual health.

- Prioritizing dunya accumulation over deen obligations. Delaying Hajj for “a better financial time” while spending freely on lifestyle upgrades is a misalignment. Financial responsibility in Islam means honoring religious obligations before optional desires.

Pro Tip: Do an annual financial review framed as a spiritual audit. Ask yourself: Where is my income from? Is my zakat current? Am I spending to show others or to fulfill genuine needs? This review catches drift before it becomes habit.

Practical steps for halal saving, investing, and planning

Knowing the principles is one thing. Applying them to your household financial plan is another. Here is how deen and financial planning come together in practice.

| Financial Area | Conventional Approach | Halal-First Approach |

|---|---|---|

| Savings account | Interest-bearing bank account | Sharia-compliant savings or current account |

| Investing | Broad market index funds | Halal-screened ETFs or Islamic investment funds |

| Insurance | Conventional insurance policies | Takaful (cooperative risk-sharing) |

| Debt management | Credit cards and revolving credit | Zero-interest financing, qard hasan |

| Charitable giving | Optional, end-of-year | Mandatory zakat plus voluntary sadaqah, budgeted monthly |

With that framework in place, the practical steps follow a logical order:

- Open a halal savings account. Many credit unions and Islamic finance institutions offer interest-free accounts. If your current account generates interest, donate that interest to charity rather than keeping it.

- Calculate your zakat annually and build it into the budget. The nisab threshold and your applicable madhab determine what you owe. A guide on how to calculate zakat walks through this precisely so nothing gets missed.

- Screen your investments. If you hold stocks, mutual funds, or cryptocurrency, verify that they meet Sharia compliance standards. Questions about modern assets matter here: understanding crypto zakat obligations is increasingly relevant for Muslim investors in 2026.

- Set faith-aligned savings goals. Hajj. Umrah. Ramadan preparation. Eid. Your children’s education. These are not luxuries. They are deen priorities, and they deserve dedicated savings buckets with consistent monthly contributions.

- Review your entire financial picture once a year. Financial planning in Islam is an act of worship aimed at earning halal provision and fulfilling family and societal responsibilities. An annual review keeps that intention alive.

My perspective: faith and finances cannot be separated

I have seen what happens when Muslim families treat their finances as a purely secular matter and bring their faith in only for the hard questions, like whether a mortgage is permissible. The result is not just spiritual inconsistency. It is financial anxiety that never fully resolves, because the framework they are using was never built for them.

What I have learned is this: the families who experience real peace around money are almost always the ones who have stopped treating barakah as a nice concept and started treating it as a real variable in their financial decisions. They ask different questions. Not just “Can I afford this?” but “Should I spend this way?” Not just “Is this income halal?” but “Am I earning and spending with gratitude and restraint?”

I have also noticed that most Muslims focus narrowly on avoiding riba while overlooking positive obligations like consistent zakat payment and intentional moderate spending. That is a significant blind spot. The absence of haram is necessary, but it is not sufficient for a financially and spiritually healthy household.

The deeper shift happens when you stop managing money and start stewarding it. That is the amanah frame. And it changes everything. Not just the numbers, but the relationship you have with those numbers, the conversations you have with your spouse, and the habits you model for your children. Financial management as continuous spiritual growth is not idealism. It is the most practical approach I know.

— Imran

Manage your family finances the halal-first way

If you are ready to put these principles into practice, Amanah Budget was built specifically for this. It is a halal-first budgeting app that brings Islamic financial principles into your daily household management without requiring you to piece together generic tools that were never designed with your values in mind.

With the Amanah Budget app, your family can track spending with halal-aware categories, calculate zakat according to your preferred madhab, and save intentionally for Hajj, Umrah, Ramadan, Eid, and education. Budgets can be shared with your spouse or family members, bank accounts connect securely through Plaid, and AI-assisted categorization handles the heavy lifting on transaction tracking.

No ads. No selling your data. No interest-based products. Just a tool built by Muslims, for Muslim families who want both their dunya and their deen reflected in how they manage money. Explore the Islamic finance blog for more practical guidance alongside the app.

FAQ

What is the role of deen in family finances?

Deen shapes every aspect of family finances, from how income is earned (halal sources only) to how it is spent (with moderation), shared (zakat and sadaqah), and saved (for faith-aligned goals). It is a complete financial framework, not just a filter for avoiding haram.

How does zakat fit into a family budget?

Zakat should be treated as a fixed budget line, calculated annually based on your wealth above the nisab threshold and paid from the top of your household income. It is both a spiritual obligation and a practical wealth-purification practice.

What does israf mean for family spending?

Israf refers to extravagance and wastefulness in spending. It includes buying beyond your means, spending to impress others, and neglecting family needs in favor of appearances. It applies even when the income itself is fully halal.

Can budgeting be considered an act of worship in Islam?

Yes. Financial planning in Islam is understood as an act of worship when the intention is to fulfill family responsibilities, earn and spend halal provision, and honor obligations to Allah and community. Tracking your money with that intention transforms a practical task into ibadah.

How do Muslim families approach saving according to Islamic principles?

Muslim families are encouraged to save consistently in halal vehicles, avoid interest-bearing accounts, and set savings goals aligned with religious priorities like Hajj, education, and emergency preparedness. The goal is family welfare and fulfillment of deen obligations, not accumulation for its own sake.

Recommended

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- Amanah Budget Blog — Islamic Finance, Zakat, and Halal Budgeting Guides

- Amanah Budget — Halal Budgeting App for Muslim Families | Zakat Calculator, Hajj Savings

- Halal Grocery Budgeting: Why Muslim Families Spend More (and How to Plan for It) — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account