Shared Family Budget App Explained for Households

Most families don’t fail at budgeting because they lack discipline. They fail because no one is on the same page. One partner checks the account on Monday, the other spends on Wednesday, and by Friday the numbers stop making sense. A shared family budget app explained properly changes that picture entirely. Rather than tracking money alone, these tools bring the whole household into one shared view, making coordination easier and money conversations far less tense. This guide covers how these apps work, what to look for, and how to use them effectively.

Table of Contents

- Key takeaways

- Shared family budget app explained

- Why shared budgeting actually helps families

- Key features to compare when choosing an app

- How to set up and use a shared budget app effectively

- Adapting your budget app as your family grows

- My honest take on shared budgeting tools

- Build your family budget with Amanahfund

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Shared apps go beyond tracking | They create real-time visibility for every family member, replacing guesswork with transparency. |

| Start with one shared category | Build confidence gradually before expanding to a full household budget using the app’s features. |

| Choose the right money structure | Fully joint, split, or hybrid setups all work — the app should match how your family handles money. |

| Monthly reviews sustain success | Short, regular check-ins under 30 minutes keep the budget relevant and the family aligned. |

| Adapt as life changes | Annual reviews help families adjust for new children, school costs, and shifting income patterns. |

Shared family budget app explained

A shared family budget app is a digital tool that lets multiple household members view, manage, and contribute to a single coordinated budget. Unlike a personal budgeting app used by one person, these tools are built around collaboration. Everyone with access can see the same numbers, update spending, and track progress toward shared goals in real time.

Most shared apps offer a core set of features:

- Multi-user access so both partners or multiple family members can log in from their own devices

- Shared dashboards showing total income, total spending, and remaining budget at a glance

- Expense categorization that sorts transactions into labeled buckets like groceries, utilities, or education

- Shared savings goals where the whole family can see progress toward a vacation fund, emergency buffer, or school fees

- Real-time syncing so that when one person makes a purchase, everyone else’s view updates immediately

- Notifications and alerts when spending approaches a limit or a goal is reached

The biggest difference between a shared app and a solo one is the visibility layer. Personal apps help you manage your own money. Shared apps help a household manage money together. That shift from “mine” to “ours” is where most of the value lives.

Pro Tip: Before downloading any app, write down the top three financial frustrations your household has right now. Then check whether the app directly solves those problems. Features matter less than fit.

Why shared budgeting actually helps families

The practical case for using a shared app is straightforward. Average household expenses for families run roughly $85,000 per year, well above the median individual income of $62,000. No single income or single view covers that picture. Shared visibility closes the gap.

But the benefits of shared budgeting go deeper than the numbers.

“Shared access and expense tracking improve communication and replace tense financial talks with real-time visibility and short check-ins.” NerdWallet

That shift matters enormously. When both partners can see the same data, money stops being a source of surprises. The conversation moves from “where did all the money go?” to “we’re $200 away from our Eid savings goal.” That’s a fundamentally different dynamic.

Here are the core benefits families consistently report:

- Less conflict around money. Shared apps reduce guesswork and help couples feel like a financial team rather than two individuals competing over a shared resource.

- Better handling of unpredictable expenses. A shared buffer category visible to everyone means a car repair or medical co-pay doesn’t derail the month.

- Clearer goal alignment. When a Hajj savings goal or emergency fund is visible to the whole family, everyone is naturally more motivated to protect it.

- Support for multiple income streams. Families with variable income, freelance work, or seasonal earnings benefit from a shared view that updates in real time as income comes in.

- Faster course-correction. If one category is overspent by mid-month, you both know immediately and can adjust before the damage compounds.

Understanding why tracking family spending builds better habits is a natural next step once you see these benefits in action.

Key features to compare when choosing an app

Not every budget app for families is built the same way. Choosing well means knowing what criteria actually matter for your household. The table below outlines the most important features and what to look for in each.

| Feature | What to look for |

|---|---|

| Multi-user logins | Each family member should have their own secure login, not a shared password |

| Dashboard visibility | Should show combined income, spending by category, and goal progress in one view |

| Goal tracking | Ability to create named savings goals (e.g., Umrah fund, school fees) with progress bars |

| Expense categorization | Automated or AI-assisted sorting, with the option to customize categories |

| Privacy controls | Option to keep some personal spending visible only to yourself |

| Syncing method | Bank-connected real-time syncing is more reliable than manual entry |

| Cost | Free tiers work for simple tracking; subscriptions typically unlock shared goals and reports |

| Platform support | Both iOS and Android coverage matters if family members use different devices |

Top shared budgeting apps offer multi-user logins, shared dashboards, and customizable goals, though their strengths vary depending on your family’s specific setup. Some are better suited to fully combined finances. Others work well for households that keep some spending separate.

App selection depends heavily on whether your family manages money as fully combined, split equally, or in a hybrid model. A fully combined household needs deep joint visibility. A hybrid household needs an app that can track both shared and personal spending without confusion.

Pro Tip: Look for apps that let you create custom spending categories. Generic categories like “miscellaneous” hide the patterns that matter most. The ability to create categories for Ramadan, Eid, school supplies, or zakat makes the budget actually reflect your family’s real life.

For a broader look at what expense tracking apps offer beyond basic categorization, the practical advantages extend well into savings and goal planning.

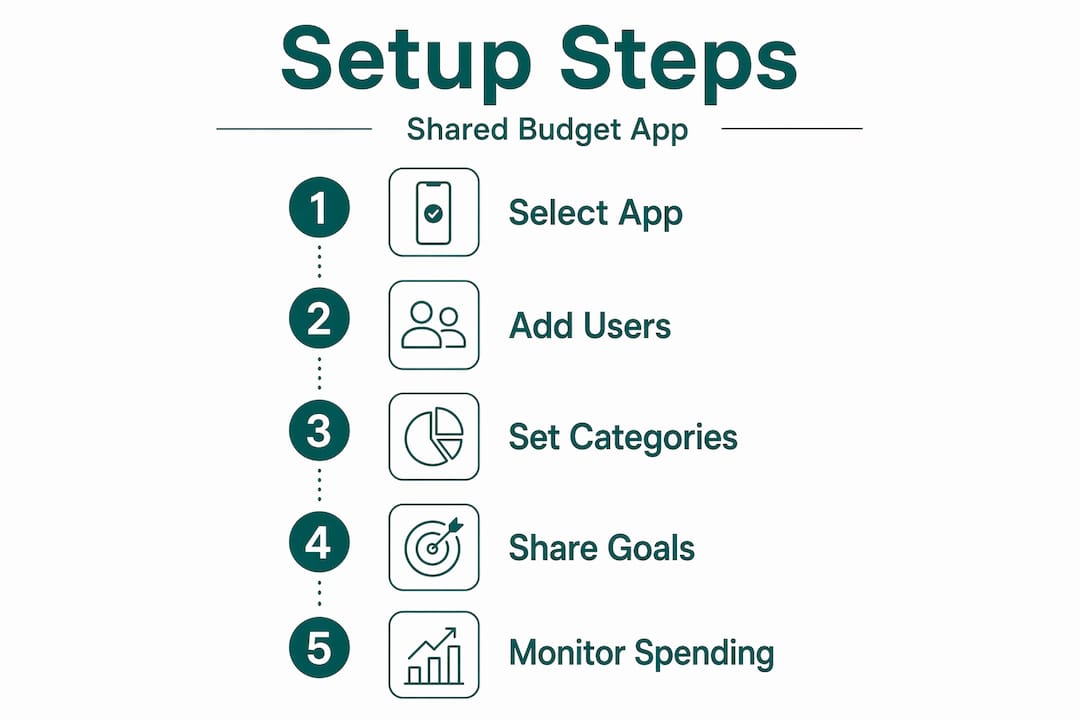

How to set up and use a shared budget app effectively

Getting started is where most families stumble. The app itself is rarely the problem. The setup is. Follow this sequence to build a system that actually sticks.

-

Agree on your budgeting structure first. Before you open the app, decide how your household handles money. Fully joint means all income and all spending are shared. A hybrid setup combines a shared account for household expenses with individual accounts for personal discretionary spending. This balance preserves autonomy while keeping the household bills coordinated.

-

Start with one shared category. Starting with a single budget category helps families build confidence before expanding. Pick the highest-friction area, usually groceries or utilities, and track only that for the first month.

-

Set up named savings goals. Give every goal a specific name and target amount. “Emergency fund” is clearer than “savings.” “Umrah 2027” is more motivating than “travel fund.” Named goals create shared ownership.

-

Assign spending categories and permissions. Most apps let you set budget limits per category. Decide together what those limits are. If the app allows role-based permissions, use them to reflect who owns which spending area.

-

Connect bank accounts for automatic syncing. Manual entry works short-term but breaks down under real life. Secure bank connection through a service like Plaid makes sure every transaction is captured without effort.

-

Schedule a monthly budget review. Monthly reviews under 30 minutes keep families aligned and make the budget sustainable over time. Pick a consistent day, like the first Sunday of each month, and treat it as a standing appointment.

-

Build a shared buffer category. Unexpected expenses are not unusual. They are normal. A dedicated “buffer” or “unexpected” category with a fixed monthly allocation prevents one surprise from blowing up the whole budget.

-

Use notifications intentionally. Turn on alerts for when a category reaches 80% of its limit. That gives you a week to adjust, not a crisis to manage on the last day of the month.

Pro Tip: Avoid starting with a 15-category budget. The more complex the setup, the faster it collapses. Two to four shared categories to start, with a review at 90 days, is a more realistic path to a budget that actually gets used.

For guidance on where Muslim families commonly overspend, knowing those patterns before you set your category limits helps you build a more accurate picture from day one.

Adapting your budget app as your family grows

A budget that fit your household two years ago may not fit today. Life changes, and the budget has to change with it. Family budgets need annual reviews to stay accurate, especially as children grow and new expenses appear.

Key moments to revisit your budget structure include:

- A new child. Childcare, diapers, medical visits, and school supplies all need dedicated categories. Most families underestimate these costs by 30 to 40 percent in the first year.

- Children starting school. Tuition, uniforms, after-school activities, and tutoring can shift your monthly spending significantly. Build those categories before back-to-school season, not after.

- College planning. This typically requires a new long-term savings goal years in advance. The sooner it appears in the app with a monthly contribution, the less pressure it creates later.

- Income changes. A job change, a side income, or a partner returning to work all affect the budget’s foundation. Review income categories before the change takes effect, not after.

- An empty nest. When children leave, household expenses drop but personal and retirement planning often need to increase. Rebalancing the budget at this stage is just as important as at any other.

Most shared budget apps let you archive old categories instead of deleting them. That keeps your historical data intact for reference while the current budget reflects where you actually are today. Reviewing budget strategy annually helps Muslim families stay aligned with both their financial goals and their values as circumstances shift.

My honest take on shared budgeting tools

I’ve worked with enough families to know that most don’t struggle with budgeting because they lack information. They struggle because managing money together is emotionally complex. There’s a real vulnerability in showing another person exactly how you spend, and that discomfort is often what holds families back from using shared tools effectively.

What I’ve found is that the apps that help most are not the most feature-rich ones. They are the ones that make the shared conversation easier. Real-time visibility removes the need for interrogation. When both partners can see the same dashboard, nobody has to ask where the money went. That single shift changes the emotional temperature around money talks completely.

The challenge I see most often is a failure to maintain the system past the first month. The initial setup is exciting. Month three is where it gets hard. Families that commit to even a 20-minute monthly review, even when there is nothing dramatic to discuss, are the ones who actually benefit long term. The review itself is the habit that holds everything together.

My take is that shared budgeting tools are not about control or oversight. They are about building a shared understanding of your household’s financial reality, and making decisions from the same set of facts. That transparency is what builds real financial trust between family members. The app is just the tool that makes it possible.

— Imran

Build your family budget with Amanahfund

Managing household finances as a team requires the right tools and the right values behind them. Amanahfund was built specifically for Muslim families who want their financial tools to reflect their deen, not just their spending habits.

With Amanahfund, you can share household budgets with your spouse or family members, track spending using halal-aware categories, calculate zakat, and save intentionally toward goals like Hajj, Umrah, Ramadan, and education. AI-assisted transaction categorization means less manual work and more time for what matters. No ads. No interest-based products. No selling your data. If you are ready to manage your family finances with both clarity and intention, start with Amanahfund and see how a values-aligned budget app feels different from everything else you have tried.

FAQ

What is a shared family budget app?

A shared family budget app is a digital tool that allows multiple household members to view, manage, and update a single coordinated budget in real time. It differs from personal budgeting apps by focusing on collaboration, shared goals, and joint expense visibility.

How do you use a family budget app effectively?

Start by agreeing on a budget structure, then add one or two shared expense categories before expanding. Schedule monthly reviews and connect bank accounts for automatic syncing to keep the budget accurate without manual effort.

What are the main benefits of shared budgeting for families?

Shared budgeting reduces money-related conflict by replacing tense conversations with real-time visibility. It helps families align on goals, manage unpredictable expenses, and coordinate multiple income streams more effectively.

Do shared budget apps work for hybrid financial setups?

Yes. A hybrid financial setup that combines a shared account for household expenses with individual personal accounts is supported by most collaborative budgeting tools. Look for apps that track both shared and personal spending separately.

How often should a family review their shared budget?

Monthly reviews of under 30 minutes are enough to keep a shared budget on track. Annual reviews are also recommended to adjust for major life changes such as new children, school costs, or shifts in household income.

Recommended

- Why Track Family Spending Habits for Better Budgeting — Amanah Budget Blog

- Household budget share: A guide for Muslim families — Amanah Budget Blog

- Household budget share: A guide for Muslim families — Amanah Budget Blog

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account