Penny Wise Household Budget: A Practical Family Guide

TL;DR:

- A penny wise household budget emphasizes deliberate spending, small savings, and attention to large expenses for financial health. It relies on simple, consistent methods like zero-based or envelope budgeting and involves the whole family in planning and tracking progress. Prioritizing effective habits and simplicity helps households avoid overwhelm and maintain long-term financial stability.

A penny wise household budget is a financial strategy that helps individuals and families manage money by tracking spending, prioritizing needs, and saving intentionally without stress or complexity. The term draws from the classic proverb “penny wise, pound foolish,” which has warned against misplaced frugality since the late 16th century. True penny wise budgeting means you pay attention to small savings without losing sight of the bigger financial picture. Methods like the 50/30/20 rule, zero-based budgeting, and envelope budgeting each offer structured ways to put this into practice. Tools like the Pennywise app and Amanahfund’s Amanah Budget app make the day-to-day tracking far more manageable for busy households.

What does being penny wise mean in household budgeting?

Being penny wise in your household budget means you are deliberate about every dollar, but not obsessive about small amounts at the expense of larger financial health. The proverb “penny wise, pound foolish” captures a real trap: someone who clips every coupon but ignores a high-interest credit card balance is saving cents while losing dollars. That imbalance is the core problem this budgeting philosophy addresses.

“Penny wise, pound foolish” is not just a saying. It is a warning that misplaced attention to small savings can cause serious damage to your overall financial position.

The modern relevance is clear. A family that switches to store-brand cereal but keeps three unused streaming subscriptions running is practicing the wrong kind of frugality. The goal is a holistic approach: small savings habits combined with regular attention to your largest expense categories, such as housing, debt, and insurance.

Common pitfalls include cutting grocery spending so aggressively that you buy lower-quality food and spend more on health costs later. Another is skipping routine car maintenance to save money, then facing a repair bill ten times larger. Penny wise budgeting avoids both extremes by treating your finances as a whole system, not a collection of isolated line items.

Pro Tip: Before cutting any small expense, check whether your three largest monthly costs, typically housing, transportation, and food, are optimized first. A single refinance or plan change there can save more than a year of coupon clipping.

How do popular budgeting methods align with penny wise principles?

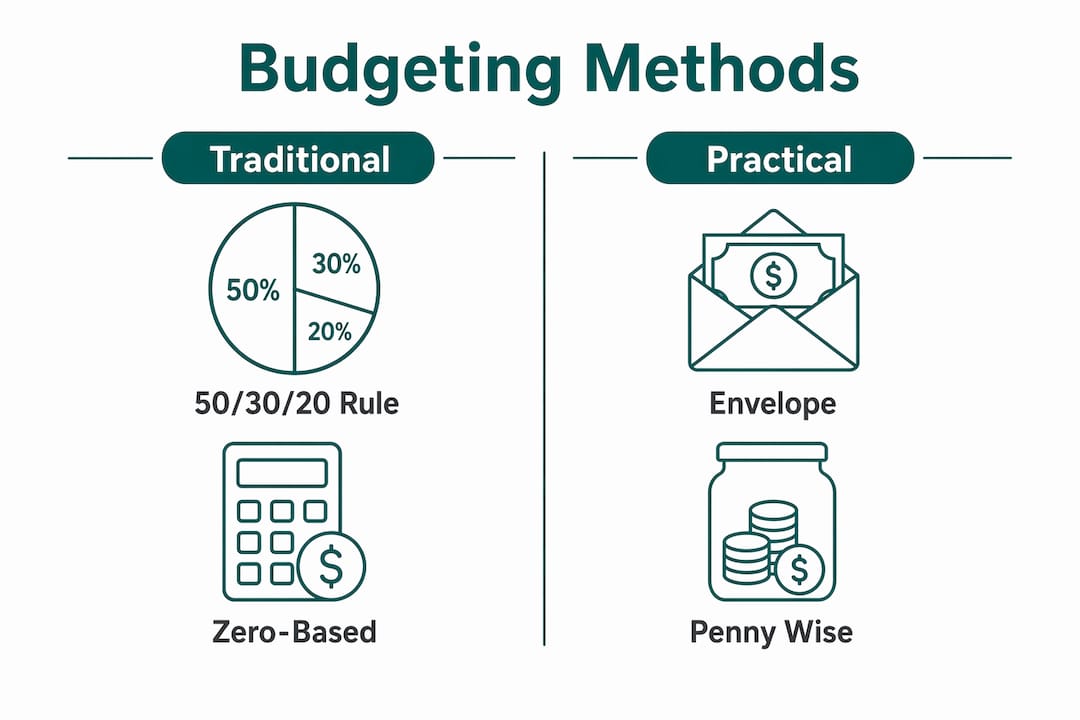

Three budgeting systems dominate personal finance today: the 50/30/20 rule, zero-based budgeting, and envelope budgeting. Each one supports penny wise principles in a different way, and choosing the right fit matters. The most effective method is the one easiest to understand and track consistently, according to Sherman Standberry, CPA. That insight alone rules out overly complex systems for most families.

The 50/30/20 rule allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. It is the easiest to start with and works well for households with relatively stable incomes. The trade-off is that it is less precise, so small spending leaks can go unnoticed within the broad categories.

Zero-based budgeting assigns every dollar of income a specific job until the balance reaches zero. This method forces you to justify each expense, which directly reflects the penny wise mindset. It takes more time to set up but gives families the clearest picture of where money actually goes each month.

Envelope budgeting uses physical or digital cash envelopes for each spending category. Once an envelope is empty, spending in that category stops for the month. This method is especially effective for controlling discretionary spending like dining out or entertainment, areas where households most often overspend without realizing it.

| Method | Best for | Ease of use | Penny wise fit |

|---|---|---|---|

| 50/30/20 rule | Stable income households | High | Moderate |

| Zero-based budgeting | Detail-oriented planners | Medium | High |

| Envelope budgeting | Discretionary spending control | Medium | High |

Notably, 47% of Americans lack any set budget at all. That means the majority of households are managing money reactively rather than intentionally, which is the opposite of penny wise financial planning.

How to create a penny wise household budget that actually works

Building a budget that holds up over time requires more than a spreadsheet. It requires a clear process, realistic categories, and a system your whole household will actually use. Here are the steps that work for most families.

-

Calculate your real take-home income. Use your lowest expected monthly income as the baseline, especially if your household has variable earnings. Budgeting to your lowest income prevents over-commitment during slower months and creates a natural buffer.

-

List every fixed and variable expense. Fixed expenses include rent, mortgage, utilities, and insurance. Variable expenses include groceries, fuel, and clothing. Write down what you actually spend, not what you think you spend. Most families underestimate variable costs by 20 to 30 percent.

-

Categorize spending as needs, wants, or savings goals. Needs come first. Savings goals, including an emergency fund, come before discretionary wants. This ordering is the foundation of effective household budgeting.

-

Build sinking funds for irregular expenses. Variable family expenses such as school fees, car repairs, and medical costs need dedicated sinking funds separate from your emergency savings. Set aside a fixed amount monthly so these costs never catch you off guard.

-

Choose a tracking tool and use it consistently. Apps like Pennywise simplify goal setting and spending tracking without complicated setup. Amanahfund’s Amanah Budget app adds halal-aware categories and zakat calculation for Muslim families who want their financial tools to reflect their values.

-

Review the budget monthly as a household. Involving all family members reduces financial anxiety and builds shared commitment to the goals you have set together.

Pro Tip: Align your bill due dates with your pay cycle wherever possible. When bills and income land in the same week, cash flow management becomes far simpler and you avoid the stress of timing gaps.

Penny wise budgeting tips to cut household expenses effectively

Saving money on everyday expenses does not require dramatic lifestyle changes. The most effective penny pinching strategies are small, repeatable habits that compound over months. Meal planning is one of the highest-impact changes a household can make. It reduces food waste, eliminates last-minute takeout purchases, and makes grocery shopping faster and cheaper. Buying staples in bulk, particularly non-perishables like rice, lentils, canned goods, and cleaning supplies, cuts per-unit costs significantly over time.

Switching to MVNO cellphone providers such as Mint Mobile or Visible instead of major carriers saves households hundreds of dollars each month for identical coverage. The same logic applies to insurance: comparing rates annually on home, auto, and health coverage often reveals savings of 10 to 20 percent that most families leave on the table simply by not reviewing their plans.

Small recurring expenses are where money quietly disappears. A $6 daily coffee, three unused app subscriptions, and a gym membership you visit twice a month can easily total $200 or more per month. Tracking these through a family spending habits review once a quarter surfaces the leaks before they become habits.

Here are practical penny wise habits any household can apply immediately:

- Plan meals for the week before grocery shopping and stick to a written list

- Buy store-brand versions of cleaning products, pantry staples, and over-the-counter medications

- Cancel subscriptions you have not used in the past 30 days

- Switch to MVNO mobile plans if your current plan exceeds $40 per line per month

- Cook in batches on weekends to reduce weekday takeout spending

- Use cashback apps like Rakuten or Ibotta for purchases you already plan to make

- Review your utility usage and switch to LED bulbs, smart thermostats, or off-peak usage schedules

Framing these habits as intentional spending choices rather than restrictions makes them far easier to sustain. You are not depriving yourself. You are choosing where your money goes with purpose.

Key takeaways

A penny wise household budget works because it combines small daily savings habits with clear attention to large financial decisions, preventing both overspending and misplaced frugality.

| Point | Details |

|---|---|

| Balance small and large savings | Cutting small costs matters, but optimizing housing, debt, and insurance saves far more. |

| Choose the right method | Zero-based and envelope budgeting offer the tightest fit for penny wise principles. |

| Build sinking funds | Set aside monthly amounts for irregular expenses to prevent budget disruption. |

| Track small recurring costs | Subscriptions and daily habits can silently drain $150 to $200 or more each month. |

| Involve the whole family | Shared budgeting goals reduce financial anxiety and improve long-term consistency. |

Why simplicity beats complexity in household budgeting

Most families I have worked with do not fail at budgeting because they lack discipline. They fail because their system is too complicated to maintain past the first month. A color-coded spreadsheet with 40 categories sounds thorough, but it collapses the moment life gets busy, which is always.

What actually works is a system simple enough to review in ten minutes on a Sunday evening. Three to five spending categories, one savings goal visible on the fridge, and a monthly family check-in. That is it. The families who sustain budgets long-term are not the ones with the most detailed plans. They are the ones with the most consistent habits.

The emotional side of budgeting is underestimated. When one partner feels controlled by the budget and the other feels ignored, no spreadsheet will fix that. Shared family financial planning that includes honest conversations about values, priorities, and trade-offs is what separates households that thrive financially from those that argue about money every month.

Fluctuating incomes make this harder, but the lowest-income baseline approach handles that well. Budget for your worst month, and every better month becomes a surplus you can direct toward goals. That mindset shift alone changes how budgeting feels. It stops being a constraint and starts being a tool you control.

— Imran

Start your penny wise budget with Amanah Budget

Amanahfund built Amanah Budget specifically for Muslim families who want their financial tools to reflect their values, not just their transactions. The app includes shared household budgeting so spouses and family members can plan together in real time. Halal-aware spending categories, a built-in zakat calculator, and dedicated savings goals for Hajj, Umrah, Ramadan, and Eid make it unlike any general budgeting app on the market. AI-powered transaction categorization handles the tracking automatically, so you spend less time on data entry and more time on decisions that matter. No ads, no data selling, and no interest-based products. Try Amanah Budget and bring your household finances in line with both your goals and your deen.

FAQ

What is a penny wise household budget?

A penny wise household budget is an intentional approach to managing family finances that tracks spending, prioritizes needs over wants, and builds savings habits without ignoring larger financial decisions. It draws from the principle of avoiding being “penny wise, pound foolish” by balancing small savings with attention to high-impact costs.

Which budgeting method works best for families?

The best method is the one your household will actually use consistently. Zero-based budgeting and envelope budgeting align most closely with penny wise principles, while the 50/30/20 rule offers the easiest starting point for households new to formal budgeting.

How do sinking funds help with household budgeting?

Sinking funds are dedicated savings pools for predictable but irregular expenses like school fees, car repairs, or medical bills. Setting aside a fixed monthly amount prevents these costs from disrupting your regular budget when they arrive.

How much can a family save by cutting small expenses?

Eliminating unused subscriptions, switching to store-brand products, and reducing dining out can save a household $150 to $300 or more per month. Switching to an MVNO mobile provider alone can save hundreds of dollars annually compared to major carrier plans.

How do you get the whole family on board with a budget?

Involve every household member in setting the budget goals, not just reviewing the numbers. Research shows that shared financial goals reduce financial anxiety and improve cooperation, making it far more likely the budget will hold over time.

Recommended

- Shared Family Budget App Explained for Households — Amanah Budget Blog

- Shared Family Budget App Explained for Households — Amanah Budget Blog

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account