Joint Budgeting for Spouses Explained: A Practical Guide

TL;DR:

- Joint budgeting for spouses involves shared financial management that promotes transparency, trust, and shared goals. The most effective models include hybrid accounts for income differences, proportional expense splits based on income, and fixed personal allowances to reduce conflict. Regular communication and documented rules ensure long-term harmony and help address common challenges like income disparity and changing financial circumstances.

Joint budgeting for spouses is defined as a shared financial management system where both partners combine income tracking, expense allocation, and savings goals into one coordinated plan. This approach to financial planning for couples does more than organize money. It creates transparency, reduces conflict, and aligns both partners on what matters most. Whether you use a single joint account, keep finances separate, or blend both, the structure you choose shapes how you communicate about money every day. This guide covers the core models, fair expense-splitting methods, and communication habits that make joint finances for couples work long-term.

What joint budgeting structures do couples typically use?

Couples generally choose from three account structures when setting up a shared budget plan for married couples: fully joint, fully separate, or a hybrid of both. Each model suits different income situations and relationship dynamics.

| Structure | How it works | Best for |

|---|---|---|

| Fully joint | All income pools into one shared account; all expenses paid from it | Couples with similar incomes and full financial transparency |

| Fully separate | Each partner keeps individual accounts; shared bills are split | Couples who prioritize financial independence |

| Hybrid | Joint account for shared expenses; separate accounts for personal spending | Couples with income differences who want both transparency and autonomy |

The hybrid setup is the most widely preferred model when incomes differ, because it preserves personal autonomy while keeping shared goals visible to both partners. This matters because one partner earning significantly more can create subtle power imbalances when all money is pooled without clear rules.

The fully joint model works well for couples who share similar financial values and want complete visibility. Joint account holders are co-owners with equal rights to deposit, withdraw, and view transaction history at any time. That legal equality is meaningful. It means neither partner is an authorized user dependent on the other’s permission. Trust and clear communication are non-negotiable when both people hold that level of access.

The fully separate model suits couples who entered the marriage with distinct financial lives and prefer to keep them that way. The practical downside is that splitting every shared bill requires constant coordination, which can itself become a source of friction. A shared budget app reduces that friction by giving both partners visibility without requiring a single merged account.

How do spouses fairly split shared expenses?

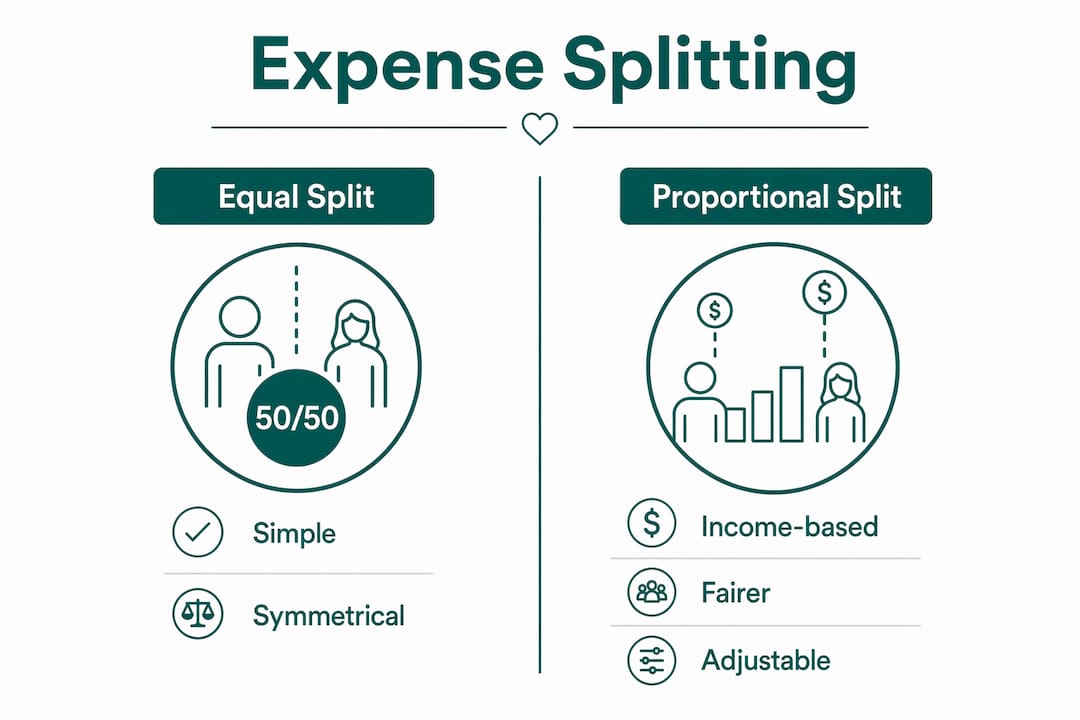

Fair expense splitting is one of the most debated topics in couple budgeting tips, and the answer depends almost entirely on income parity. Two methods dominate: the 50/50 split and the proportional split.

The 50/50 split divides every shared expense equally regardless of income. It feels simple and symmetrical, but it places a heavier burden on the lower-earning partner as a percentage of their take-home pay. If one spouse earns $4,000 per month and the other earns $7,000, splitting a $2,500 rent payment equally means the lower earner contributes 31% of their income versus 18% for the higher earner. That gap compounds across every shared expense.

Proportional splits based on income ratio are fairer when incomes differ significantly. Here is how to calculate it:

| Spouse | Monthly income | Income share | Contribution to $2,500 rent |

|---|---|---|---|

| Spouse A | $4,000 | 36% | $900 |

| Spouse B | $7,000 | 64% | $1,600 |

Both partners contribute the same percentage of their income, which keeps the financial burden proportional. This model tends to be more sustainable over time because neither partner feels financially squeezed by the arrangement.

Documenting contribution rules in writing prevents arguments when incomes shift. A job change, a promotion, or a period of reduced hours can all disrupt a verbal agreement. A written record of the agreed percentage, reviewed every six months, removes ambiguity before it becomes resentment.

Pro Tip: Set a calendar reminder every six months to review your income figures and recalculate contribution percentages. A 10-minute review twice a year prevents months of unspoken frustration.

A third approach is category-based division, where each partner takes full ownership of specific expense categories. One spouse covers rent and utilities; the other covers groceries and childcare. This works when both partners are organized and trust each other to pay on time, but it can create blind spots if one category consistently runs over budget without the other partner knowing.

How to set personal spending allowances and why they matter

A personal spending allowance is a fixed monthly amount each spouse can spend without explanation or approval from the other. This is one of the most underused tools in joint income management, and one of the most effective.

Small fixed allowances prevent every personal purchase from becoming a negotiation, which directly reduces conflict. When every coffee, book, or gym class requires justification, the budget starts to feel like surveillance rather than a shared plan. That dynamic erodes trust faster than overspending does.

Here is what a personal allowance system accomplishes:

- It gives each partner genuine financial autonomy within a shared framework

- It removes the need to justify personal preferences to each other

- It sets a clear boundary between shared expenses and individual spending

- It reduces the emotional weight of the monthly budget review

- It prevents one partner from feeling financially controlled by the other

The starting amount matters less than the principle. Many couples begin with $50 to $100 per person per month and adjust based on income and lifestyle. What matters is that both partners receive the same amount, regardless of who earns more. Equal allowances signal equal respect within the partnership.

Pro Tip: Treat personal allowances as non-negotiable line items in your shared budget, the same way you treat rent or utilities. If the budget is tight, reduce shared expenses before cutting personal allowances.

Reviewing allowances annually keeps them relevant. A couple that set $75 allowances three years ago may find that figure no longer reflects their actual needs or income. The benefits of shared household budgets include exactly this kind of structured flexibility, where the plan adapts to the couple rather than the couple adapting to a rigid plan.

Strategies to maintain financial harmony with joint budgeting

The most common source of money disputes between spouses is not a lack of income. Money conflicts stem from unclear discretionary spending boundaries and misaligned priorities. The fix is structural, not financial.

Regular money meetings are the single most effective habit for couples managing joint finances. Structured weekly meetings with a fixed agenda reduce money-related conflicts by over 40%. That is a significant reduction from a habit that takes 20 to 30 minutes per week.

A productive money meeting follows this format:

- Review account balances and recent transactions together

- Confirm upcoming bills and shared expenses for the next two weeks

- Check progress toward shared savings goals such as emergency funds or Hajj savings

- Raise any spending decisions above an agreed threshold (for example, any purchase over $200)

- Adjust the budget if income or expenses have changed

- Close with one shared financial win from the past week

That last step matters more than it sounds. Ending on a positive note keeps the meeting from feeling like a performance review and reinforces that you are working toward the same goals.

“Budgeting for couples works best when it is treated as a communication tool rather than a math exercise. Agreeing on the rules is what makes the plan sustainable.” — The Penny Hoarder

Aligning on account structure and contribution method before building the budget minimizes conflict from the start. Couples who skip this step often find themselves arguing about process rather than progress. Most couples also benefit from selecting three to four core shared goals such as an emergency fund, a family vacation, or retirement savings to anchor their budgeting decisions. Clear goals give the budget a purpose beyond expense management.

Common challenges couples face with joint budgeting

Even well-designed budgets run into real-world friction. These are the most common challenges and how to address each one directly:

- Income disparity: One partner earning significantly more creates tension in a 50/50 model. Switch to a proportional split and document the agreed percentages in writing to remove ongoing negotiation.

- Privacy concerns: Some partners need a degree of financial privacy, particularly around personal purchases or gifts. Personal allowances solve this without requiring full financial separation.

- Changing financial situations: A job loss, a new child, or a career shift can make the current budget unworkable. Build a six-month review into the budget calendar so adjustments happen proactively rather than reactively.

- Ad hoc spending disputes: Arguments about unplanned purchases are almost always a symptom of unclear rules. Set a household spending threshold above which both partners must agree before a purchase is made.

- Resistance to transparency: If one partner is reluctant to share financial information, the issue is usually trust rather than money. Addressing family financial conflicts early, before they calcify into habits, is far easier than resolving them after years of avoidance.

If a couple consistently struggles despite clear rules and regular meetings, a session with a financial counselor or a trusted community advisor can provide neutral ground for the conversation.

Key takeaways

Joint budgeting for spouses works when both partners agree on a clear account structure, a fair contribution method, and personal spending allowances before building the budget itself.

| Point | Details |

|---|---|

| Choose the right structure | Hybrid accounts suit most couples with income differences, combining transparency with personal autonomy. |

| Use proportional splits | Splitting expenses by income percentage keeps the financial burden equal for both partners. |

| Set personal allowances | Fixed no-questions-asked spending amounts reduce conflict and preserve individual autonomy within the shared plan. |

| Hold regular money meetings | Weekly structured check-ins with a fixed agenda reduce money conflicts and keep both partners aligned. |

| Document contribution rules | Written agreements on percentages prevent disputes when incomes change and remove ambiguity from the process. |

What I have learned from watching couples budget together

Couples who struggle with money rarely have a math problem. They have a communication problem that shows up in the numbers. I have seen spouses with modest incomes manage beautifully together, and high-earning couples tear each other apart over grocery receipts. The difference is almost always whether they agreed on the rules before the money moved.

The advice to “just combine everything” is well-intentioned but often wrong. Full financial merger works for some couples and creates resentment in others. The hybrid model is not a compromise. For many couples, it is the most honest reflection of how two adults with distinct histories and preferences actually live together.

What I would caution against is treating the budget as a finished document. A budget that is not reviewed is not a budget. It is a wish list. The couples who get this right treat their monthly money meeting the same way they treat a prayer time or a family dinner. It is scheduled, it is protected, and it is not optional.

The other thing I would say plainly: if your budgeting system makes one partner feel monitored or controlled, the system is wrong regardless of how mathematically sound it is. Financial tools should reflect the values of the people using them, including respect, trust, and shared purpose.

— Imran

Start managing your joint finances with Amanahfund

Amanahfund is built specifically for Muslim families who want their financial tools to reflect their values. The Amanah Budget app lets spouses share a household budget, track spending with halal-aware categories, and save intentionally toward goals like Hajj, Umrah, Ramadan, and education. Both partners can connect bank accounts securely through Plaid and receive AI-assisted transaction categorization so your money meeting takes minutes, not hours. No ads, no interest-based products, and no selling your data. If you are ready to put your joint finances on a foundation that honors both your dunya and your deen, Amanahfund is where to start.

FAQ

What is joint budgeting for spouses?

Joint budgeting for spouses is a shared financial management system where both partners coordinate income tracking, expense allocation, and savings goals together. It can use a single joint account, separate accounts, or a hybrid of both depending on the couple’s income and preferences.

Is a 50/50 expense split always fair for couples?

A 50/50 split is only fair when both partners earn similar incomes. When incomes differ significantly, a proportional split based on each partner’s share of total household income distributes the financial burden more equitably.

How much should personal spending allowances be?

Most couples start with $50 to $100 per person per month as a no-questions-asked personal allowance. The exact amount matters less than the principle: both partners receive equal amounts, and the allowance is treated as a fixed budget line item.

How often should couples review their joint budget?

Couples benefit from a brief weekly money meeting to review transactions and upcoming expenses, plus a more thorough review every six months to adjust contribution percentages if incomes have changed.

What is the biggest cause of money conflicts between spouses?

Money disputes between spouses most often stem from unclear discretionary spending boundaries and misaligned priorities, not from a lack of money itself. Clear written rules and regular check-ins address the root cause directly.

Recommended

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account