Islamic View on Wealth Tracking: 2026 Guide

TL;DR:

- Islamic wealth tracking involves monitoring zakatable assets relative to nisab and hawl in accordance with Shariah. It is a spiritual act of accountability to Allah that ensures correct zakat fulfillment and responsible wealth management.

The Islamic view on wealth tracking is defined as the religious and financial practice of monitoring zakatable assets relative to nisab and hawl, in full compliance with Shariah principles. This is not optional financial hygiene. Wealth tracking in Islam is an act of worship, a form of accountability to Allah, and the foundation for fulfilling zakat obligations correctly. Islamic finance principles prohibit riba (interest), gharar (excessive uncertainty), and maysir (gambling), which means tracking wealth also requires monitoring the nature and source of every asset. Understanding how nisab, hawl, and asset categorization work together gives you a complete picture of what responsible wealth management in Islam actually demands.

What is the islamic view on wealth tracking?

The two conditions that trigger zakat obligation are nisab and hawl. Every Muslim who tracks wealth for religious purposes must understand both before calculating anything else.

Nisab is the minimum threshold of zakatable wealth. It is defined in gold and silver equivalents. The gold nisab equals approximately 85 grams of gold, and the silver nisab equals approximately 595 grams of silver. Scholars recommend using whichever threshold applies to your specific madhab and local scholarly guidance.

Hawl is the lunar year holding period. Zakat becomes obligatory only when zakatable wealth reaches nisab and stays above that threshold for one full lunar year, which equals approximately 354 days. The hawl clock starts the day your wealth first crosses the nisab line.

Here is what this means practically:

- You do not need to track each dollar or each asset individually across the year.

- Scholars agree that the hawl applies to your total zakatable wealth, not to individual amounts or individual acquisitions.

- If your total zakatable wealth drops below nisab at any point during the year, the hawl resets when nisab is reached again.

- Continuous holding above nisab counts as an ongoing hawl, even if the specific assets change.

- Using the solar calendar for zakat timing contradicts Sharia guidance. The hawl must be counted using the Islamic lunar calendar.

Pro Tip: Pick a fixed Islamic date, such as the 1st of Ramadan, as your annual zakat checkpoint. This is a permitted and widely recommended method that removes the stress of tracking the exact day nisab was first met.

The practical takeaway here is significant. You are not required to obsess over daily fluctuations. What matters is whether your total zakatable wealth remains above nisab at the end of the hawl period.

Which assets are zakatable vs. non-zakatable?

Zakatable wealth is distinct from total net worth. Practical guides show that zakatable wealth often comprises 25–60% of net worth for many Muslims. Getting this distinction right prevents both overpaying and underpaying zakat.

| Asset Type | Zakatable? |

|---|---|

| Cash and bank savings | Yes |

| Stocks and equity investments | Yes (market value at zakat date) |

| Business inventory and trade goods | Yes |

| Gold and silver held as investment | Yes |

| Primary residence | No |

| Personal vehicle | No |

| Household furniture and clothing | No |

| Retirement accounts (accessible funds) | Depends on madhab |

Assets subject to zakat include cash, stocks, business inventory, precious metals, and livestock. Their valuation is based on market value at the zakat date, not at the time of purchase. This is why a fixed annual calculation date simplifies everything.

Many Muslims make the error of calculating zakat on their entire net worth. A family home worth $500,000 is not zakatable. A savings account holding $30,000 is. Separating these two figures is the first practical step in accurate wealth management in Islam.

In practice, Muslims who track wealth carefully often maintain two separate figures: overall net worth for financial planning, and zakatable wealth for obligation calculations. This separation avoids the most common errors in zakat duty fulfillment.

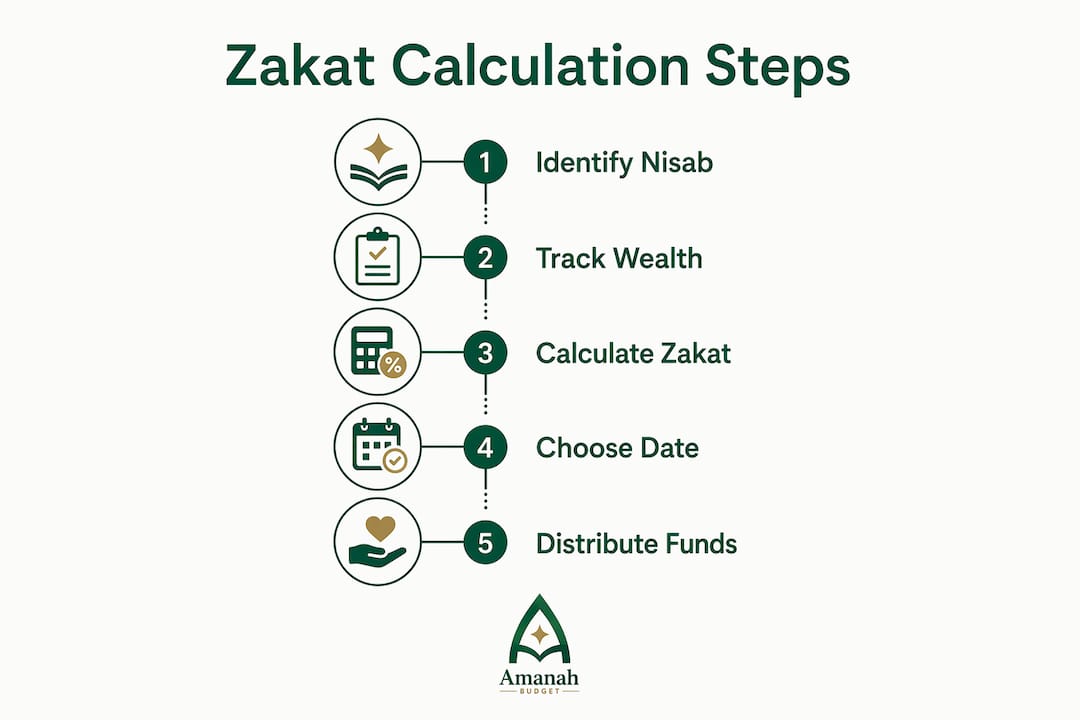

How do you practically track wealth and calculate zakat?

Practical wealth tracking for zakat does not require daily monitoring. It requires one well-organized annual review. Here is a clear method that aligns with Islamic finance principles and Sharia compliance:

-

Choose a fixed Islamic date. The 1st of Ramadan is the most widely used. A fixed-date calculation is a permitted and practical method that balances Sharia compliance with realistic recordkeeping. On that date, you calculate zakat on all zakatable wealth present, regardless of when specific assets were acquired.

-

List all zakatable assets. Pull together the current market value of cash, savings, stocks, gold, silver, and business inventory. Use the values on your chosen date, not historical purchase prices.

-

Subtract zakatable liabilities. Debts due within the year can be deducted from zakatable wealth in most scholarly opinions. Consult your madhab for specifics.

-

Check against nisab. If the remaining zakatable wealth meets or exceeds nisab, zakat is due at 2.5% of the total.

-

Audit your investments for Sharia compliance. Islamic finance prohibits transactions involving riba, gharar, and maysir. This means you must track not just the amount of your wealth but the nature and source of each asset. Segregate any non-Sharia-compliant holdings and seek guidance on purification.

-

Record everything. Keep a simple spreadsheet or use a halal-first app to log asset values, the calculation date, and the zakat amount paid. This record protects you and creates a clear year-over-year picture.

Pro Tip: If you hold stocks, use a halal investment screening tool or consult a Sharia-compliant financial advisor to verify your portfolio before your annual zakat date. Many halal fintech apps now include built-in screening features.

Islamic finance modes like musharakah (partnership) and mudarabah (profit-sharing) form the foundation for halal investing and ethical wealth growth. Tracking which of your assets follow these structures is part of responsible wealth management in Islam.

Why does islam view wealth as a trust, not a possession?

Wealth in Islam is a trust (amanah) from Allah, requiring responsibility, purification through zakat and sadaqah, and ethical use. This is not a peripheral idea. It is the theological foundation that makes wealth tracking a spiritual act, not just a financial one.

“And spend in the way of Allah and do not throw yourselves with your own hands into destruction.” (Quran 2:195)

This framing changes how you approach financial recordkeeping. You are not tracking wealth to protect it or grow it for its own sake. You are tracking it to fulfill your obligations as a steward. Zakat is the mechanism of purification. Hoarding wealth contradicts Islamic teachings when it replaces remembrance of Allah and crowds out generosity.

The distribution obligations in Islam include zakat (obligatory), sadaqah (voluntary charity), and lawful spending on family and community. Tracking your wealth accurately means you can fulfill each of these with confidence. Underpaying zakat due to poor recordkeeping is a religious shortcoming, not just a financial error.

Balanced wealth management in Islam unites financial discipline with social responsibility. Zakat is a mechanism to purify wealth and redistribute blessings within the community. Tracking wealth carefully is therefore vital to social justice as well as personal worship. This is the ethical wealth accumulation model Islam promotes: grow lawfully, track honestly, distribute faithfully.

Key takeaways

The Islamic view on wealth tracking requires monitoring zakatable assets against nisab and hawl, categorizing assets correctly, and aligning all financial practices with Sharia principles as an act of worship.

| Point | Details |

|---|---|

| Nisab and hawl are the triggers | Zakat is due only when zakatable wealth stays above nisab for one full lunar year. |

| Track zakatable wealth separately | Zakatable assets are often 25–60% of total net worth; separate them from overall finances. |

| Use a fixed annual date | Calculating zakat on a set date like 1st Ramadan is permitted and reduces tracking errors. |

| Screen investments for Sharia compliance | Riba, gharar, and maysir disqualify assets; audit your portfolio before each zakat date. |

| Wealth is amanah | Tracking is an act of worship and accountability, not financial anxiety or obsession. |

Wealth tracking as a yearly act of worship

I have spoken with many Muslims who feel genuine anxiety about zakat calculation. They worry they are doing it wrong, that they missed an asset, or that daily fluctuations in their savings account have somehow invalidated their hawl. That anxiety is understandable, but it is also unnecessary.

The scholars are clear: you track total zakatable wealth, not every individual dollar. You pick a date, you calculate honestly, and you pay. The system is designed for real people with real financial lives, not for accountants with perfect records.

What I find most meaningful about the Islamic approach to spending accountability is that it reframes the entire purpose of financial awareness. You are not tracking wealth to feel secure. You are tracking it to give correctly. That shift in motivation changes everything about how you relate to money.

My honest recommendation is to treat your annual zakat calculation as a financial checkpoint, not a test you can fail. Review your zakatable assets, check your investments for Sharia compliance, calculate what you owe, and pay it. Then use the rest of the year to build habits that make next year’s review easier. Tools built around Islamic values, like halal-first budgeting apps, exist precisely to support this kind of intentional, values-aligned financial practice. Use them.

— Imran

Simplify your wealth tracking with Amanahfund

Tracking zakatable assets, calculating zakat by madhab, and keeping your finances Sharia-compliant is a real responsibility. Amanahfund makes it manageable.

Amanahfund’s halal-first budgeting app is built specifically for Muslim families. It includes zakat calculation tools aligned with your preferred madhab, halal-aware spending categories, and AI-powered transaction categorization to help you separate zakatable from non-zakatable assets. You can also set savings goals for Hajj, Umrah, Ramadan, and Eid, and share budgets with your spouse or family. No ads, no interest-based products, and no selling of your data. Visit Amanahfund to start managing your wealth the way your deen intends.

FAQ

What is nisab and why does it matter for zakat?

Nisab is the minimum threshold of zakatable wealth, defined in gold or silver equivalents, that must be met before zakat becomes obligatory. If your total zakatable wealth does not reach nisab, no zakat is due for that year.

Does every asset you own count toward zakat?

No. Assets like your primary residence, personal vehicle, and household items are generally exempt from zakat. Zakatable assets include cash, savings, stocks, gold, silver, and business inventory valued at market price on your calculation date.

How do you track hawl if your wealth fluctuates?

The hawl applies to your total zakatable wealth, not individual assets. If your total stays above nisab throughout the lunar year, the hawl is continuous. If it drops below nisab, the hawl resets when nisab is reached again.

Is it permissible to use a fixed date for zakat calculation?

Yes. Choosing a fixed Islamic date, such as the 1st of Ramadan, is a widely permitted and recommended method. On that date, you calculate zakat on all zakatable wealth present, regardless of when specific assets were acquired.

How do islamic finance prohibitions affect wealth tracking?

Riba, gharar, and maysir are prohibited in Islamic finance, which means tracking wealth also requires reviewing the source and nature of your assets. Interest-bearing accounts and non-Sharia-compliant investments must be identified, segregated, and addressed before your annual zakat calculation.

Recommended

- Amanah Budget Blog — Islamic Finance, Zakat, and Halal Budgeting Guides

- How to Calculate Zakat on Your Wealth: A Complete 2026 Guide — Amanah Budget Blog

- How to Calculate Zakat on Your Wealth: A Complete 2026 Guide — Amanah Budget Blog

- Spending Accountability in Islam: A 2026 Guide — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account