Interfaith financial planning: a Muslim family’s guide

Many Muslim families in interfaith households quietly carry a worry that standard financial planning will force them to compromise their Islamic values. The assumption is that conventional tools and advice were built for someone else. But what is interfaith financial planning, really? It is a coordinated approach that brings different faith traditions and financial values into one working system — and for Muslim families in the US, that means halal budgeting, zakat, and faith-aligned goals can sit at the center of your financial life, not at the margins.

Table of Contents

- Understanding interfaith financial planning and Islamic values

- A stage-by-stage roadmap to halal financial goals

- Navigating interfaith complexities: ethics, responsibilities, and joint finances

- Halal budgeting and goal setting for Muslim families in the US

- A unique perspective on interfaith financial planning in Muslim families

- Bring your interfaith financial plan to life with Amanah Budget

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Interfaith financial planning | Coordinates financial decisions across faiths while respecting Islamic values like halal budgeting and investing. |

| Stage-by-stage roadmap | Using a halal life map tailored to your life stage helps align financial goals with Islamic principles consistently. |

| Clear responsibility agreements | Written agreements about financial roles reduce conflicts in interfaith couples more than joint account structures. |

| Halal budgeting steps | Planning includes earning halal, budgeting, paying zakat, saving, and investing in Sharia-compliant ways. |

| Faith-aligned tools | Apps like Amanah Budget provide practical support for Muslim families to manage halal budgets and zakat accurately. |

Understanding interfaith financial planning and Islamic values

Interfaith financial planning coordinates the values of two or more faith traditions within one household’s financial decisions. For Muslim families, that means Islamic principles are not negotiated away — they are built into the foundation of how money is earned, spent, saved, and given.

Islamic financial planning means earning, saving, and growing money in a halal way — no interest (riba), no haram income, and regular zakat. These are not optional extras. They are the pillars that define whether your financial plan is actually working for your deen.

Here are the core Islamic finance principles that belong in every Muslim family’s financial plan:

- No riba (interest): Mortgages, savings accounts, and credit products must be evaluated for interest-based structures. Halal alternatives exist, including murabaha (cost-plus financing) and Islamic savings accounts.

- Halal income: Your income source matters. Any earnings from haram industries, such as alcohol, gambling, or weapons, must be avoided or purified through giving.

- Zakat obligation: Zakat is a mandatory annual giving of 2.5% on eligible wealth above the nisab threshold. It is not charity — it is a financial right owed to those in need.

- Ethical investing: Sharia-compliant investing screens out companies involved in prohibited activities. Halal index funds and Islamic ETFs have grown significantly in recent years.

- Halal spending habits: Money should not be wasted or spent on prohibited goods. Budgeting is an act of amanah (trustworthiness) over the wealth Allah has provided.

Cross-cultural financial planning adds another layer. When spouses come from different faith or cultural backgrounds, their default assumptions about money can differ widely. One partner may see saving as a spiritual obligation; the other may see giving as the highest priority. Interfaith financial strategies bring these perspectives into alignment through honest dialogue and shared written agreements.

Organizations like the faith-consistent investing network at FaithInvest show that faith-based financial frameworks are not niche. They are a growing global movement. For Muslim families, developing a best budgeting strategy anchored in Islamic values is not complicated — but it does require intention and structure.

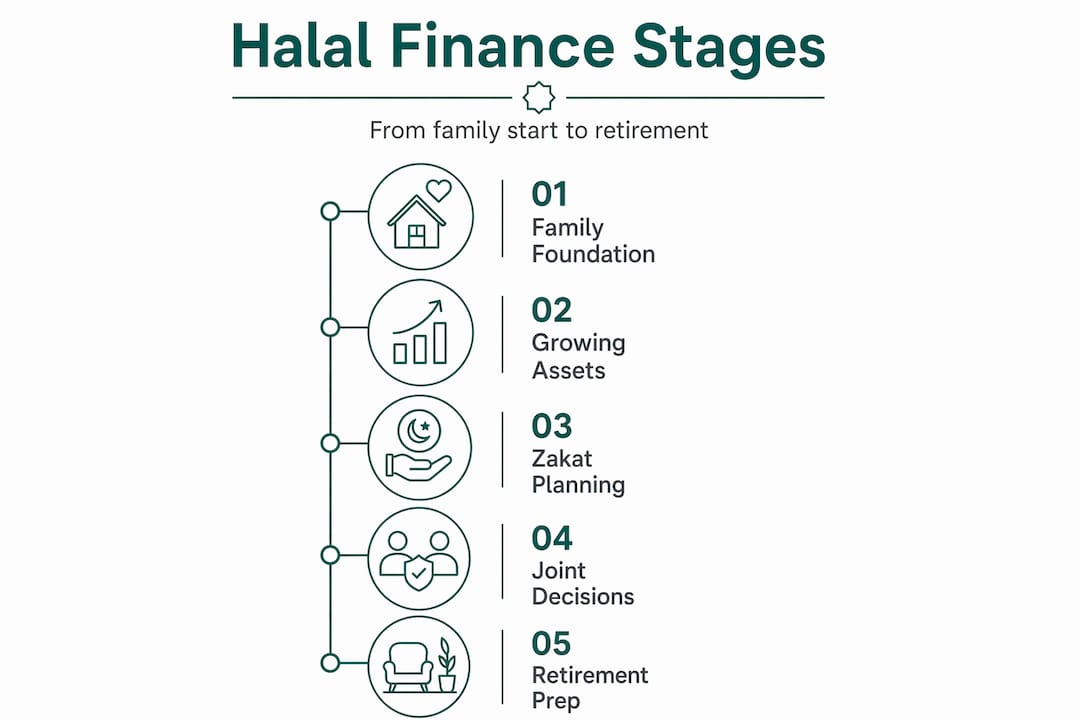

A stage-by-stage roadmap to halal financial goals

With foundational Islamic principles covered, a practical lifecycle framework helps apply these principles at every stage of your family’s financial journey.

A stage-by-stage Islamic finance roadmap explicitly ties financial decisions to halal requirements and life events, rather than treating money as purely numbers. This kind of roadmap is sometimes called the Halal Life Map, and it covers six key stages:

- Student: Focus on avoiding student debt where possible, understanding halal income from part-time work, and building early saving habits.

- First-time homebuyer: Evaluate Islamic mortgage alternatives, compare murabaha or diminishing musharakah products, and build a halal down payment fund.

- Growing family: Prioritize zakat calculation, start Hajj and Umrah savings, set up halal life insurance alternatives like takaful, and budget for children’s Islamic education.

- Established professional: Review investment portfolios for Sharia compliance, increase zakat giving, and build a waqf (charitable endowment) strategy.

- Pre-retirement: Review estate planning with Islamic inheritance rules (faraid), shift investments to lower-risk Sharia-compliant assets, and increase nafl (voluntary) giving.

- Retirement: Live within halal income from savings and investments, continue zakat and sadaqah, and finalize Islamic will and estate documents.

Each stage carries distinct financial priorities. The table below shows how key halal finance areas shift across three core stages:

| Financial area | Growing family stage | Established professional | Pre-retirement |

|---|---|---|---|

| Zakat | Calculate on savings and gold | Includes investments and business | Includes full asset review |

| Investing | Start halal index funds | Diversify Sharia-compliant portfolio | Shift to lower-risk halal options |

| Insurance | Explore takaful options | Review family takaful coverage | Reduce coverage, review needs |

| Estate planning | Basic Islamic will | Update with assets and children | Finalize faraid distribution |

| Savings goals | Hajj, emergency fund | College, Hajj, second property | Retirement income, final Hajj |

Following a stage-by-stage halal budgeting roadmap removes the guesswork. You always know what your halal financial priorities should be right now, not just in theory.

Pro Tip: Set a reminder every six months to revisit your halal financial checklist. As your family grows and your wealth changes, your zakat calculation, savings goals, and investment screening need to grow with you.

Navigating interfaith complexities: ethics, responsibilities, and joint finances

Now that we have a practical framework in place, the harder conversation for many interfaith families is about the everyday friction: who pays for what, how shared spending decisions are made, and where ethical lines are drawn.

Many financial disagreements in interfaith couples are caused less by account type — joint versus separate — and more by mismatched expectations about who is responsible for which financial categories. This is a critical insight. Two people can share one bank account and still have constant conflict if they never agreed on who handles housing costs, who manages discretionary spending, and who is responsible for charitable giving.

A clear financial responsibility map is more useful than any account structure. Here is what to define together:

- Housing costs: Who covers rent or mortgage? Is this shared equally or based on income?

- Religious expenses: Zakat, sadaqah, Ramadan giving, and Hajj savings should be explicitly budgeted. Do not leave these as afterthoughts.

- Debt repayment: Agree on which debts are shared obligations and which are personal.

- Discretionary spending: Define individual spending allowances so neither partner feels monitored.

- Children’s education and Islamic upbringing: Who funds Islamic school fees, Quran classes, and community activities?

On investments, separating ethical screens from financial mechanics helps avoid endless product debates. Agree first on what both partners will not invest in, such as alcohol, interest-based banking, or weapons companies. Once that shared avoid list is written down, choosing the actual fund or account type becomes a practical decision rather than a values debate.

Resources like financial literacy support for interfaith families can also help couples find shared language for money conversations that feel fair and respectful to all parties. This is part of the importance of interfaith financial literacy — it is not just about knowing the rules, but about building the communication skills to apply them together.

For halal spending specifically, tracking budgeting for halal expenses separately from general categories gives Muslim family members visibility over where their values-aligned spending is going each month.

Pro Tip: Write a one-page financial agreement early in your planning process. Cover responsibilities, shared ethical screens, and religious spending commitments. Revisit it annually. This single habit prevents more conflict than any budgeting app alone.

Halal budgeting and goal setting for Muslim families in the US

With budgeting responsibilities clarified, the practical question becomes: how do you actually build a halal budget that holds up in daily life?

Islamic financial planning works in clear steps: earn halal, track your money, budget it, pay zakat, build savings, and invest only in Sharia-approved ways. This is not a complex system. It is a values-first order of operations.

Here is how to apply those steps as a Muslim family in the US:

- Earn halal: Review all income sources. If any income comes from interest or haram industries, calculate what must be purified and given away.

- Track every transaction: You cannot budget what you cannot see. Categorize all spending by halal-aware categories, including food (halal vs. non-halal), entertainment, and charitable giving.

- Build your halal budget: Allocate income across needs, wants, religious obligations, and savings goals. The proportions should reflect your stage on the Halal Life Map.

- Calculate and pay zakat: Learn to calculate zakat accurately based on your assets, savings, and business wealth. Do not estimate.

- Save intentionally: Budget for Hajj, Umrah, Ramadan, Eid, children’s education, and emergencies as separate named goals — not a single “savings” bucket.

- Invest in Sharia-compliant assets: Screened index funds, Islamic ETFs, and halal real estate investments are all accessible in the US market today.

Here is a practical look at how a halal household budget might be distributed:

| Budget category | Recommended range | Notes |

|---|---|---|

| Housing (halal mortgage or rent) | 25–35% | Prefer Islamic finance products |

| Food and halal groceries | 10–15% | Include halal meat and dining |

| Zakat and sadaqah | 2.5–5% | Calculated on eligible wealth |

| Hajj and Umrah savings | 3–8% | Stage-dependent priority |

| Education (Islamic and academic) | 5–10% | Children and self-development |

| Investments (Sharia-compliant) | 10–20% | Based on stage and risk tolerance |

| Emergencies and general savings | 5–10% | Minimum three months’ expenses |

| Discretionary spending | 10–15% | Avoid haram categories |

Use halal budgeting techniques that match your family’s madhab and financial realities. Financial planning for diverse beliefs works best when the tools you use reflect your actual values, not generic categories designed for someone else.

Pro Tip: Technology built specifically for halal budgeting removes the friction of manually sorting transactions into Islamic categories. When your budgeting tool already understands zakat and Hajj savings, your monthly review becomes faster and more accurate.

A unique perspective on interfaith financial planning in Muslim families

Here is something most interfaith financial advice misses entirely: the real challenge is not the account structure or the investment product. It is the assumption that financial harmony requires financial sameness.

Many Muslim families feel pressure to merge every financial decision into a single joint framework. But Islamic marriage actually provides a clear and generous structure. The husband’s financial responsibility (nafaqa) for household expenses is defined. The wife’s wealth remains her own. These roles, when understood and respected, reduce conflict rather than create it. They are not outdated — they are a built-in financial responsibility map that many couples spend years trying to create from scratch.

The importance of interfaith financial literacy is not just about knowing halal investing rules. It is about understanding your own tradition’s financial framework well enough to explain it clearly to a spouse who grew up with different defaults. When you can articulate why zakat is not optional or why riba-free financing matters, those conversations become education rather than argument.

We also see this with financial planning for diverse beliefs more broadly. The families who navigate it best are not the ones who compromise their values. They are the ones who document them. A written agreement about financial roles, ethical screens, and religious giving goals does more work than any sophisticated investment strategy.

Zakat is a useful example. Both partners do not need identical approaches to charitable giving. But when zakat is budgeted, tracked, and paid on time as a household priority, it signals shared intent. That shared intent is what creates financial planning for Muslim families that actually lasts.

The takeaway: interfaith financial strategies do not require complexity. They require clarity. Define the roles, document the ethics, name the goals, and use tools designed for your values.

Bring your interfaith financial plan to life with Amanah Budget

Understanding interfaith financial planning is one thing. Having the right tools to put it into practice daily is another. Amanah Budget was built specifically for Muslim families who want their budgeting experience to reflect their deen from the first transaction.

With Amanah Budget, you can track spending in halal-aware categories, use a built-in zakat calculator based on your preferred madhab, and set dedicated savings goals for Hajj, Umrah, Ramadan, and Eid. Household budgets can be shared with your spouse so both partners see the same picture. There are no ads, no interest-based products, and no selling of your data. If you are ready to apply what you have learned from this halal budgeting guide in a practical, faith-first way, Amanah Budget is where that journey continues.

Frequently asked questions

Is financial planning allowed in Islam?

Yes, financial planning is fully allowed in Islam as long as income, savings, and investments stay within halal boundaries. Intentional money management is itself an act of amanah.

How do Muslim couples handle finances in interfaith marriages?

Many financial disagreements in interfaith couples come from mismatched expectations about financial responsibilities rather than account types. Clear written role agreements reduce conflict far more than combining or separating accounts.

What is halal budgeting?

Halal budgeting is managing money according to Islamic principles, including earning halal income, avoiding interest and haram spending, paying zakat, and investing only in Sharia-compliant ways.

How can I ensure my investments align with Islamic values in an interfaith household?

Agree first on a shared ethical avoid list, then choose specific financial products separately. Separating ethics screens from mechanics keeps investment conversations productive rather than contentious.

Where can I find tools to help with halal budgeting and zakat?

Specialized apps like Amanah Budget offer halal-aware budgeting features, zakat calculators, and dedicated savings plans built specifically for Muslim families in the US.

Recommended

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- Amanah Budget Blog — Islamic Finance, Zakat, and Halal Budgeting Guides

- Amanah Budget — Halal Budgeting App for Muslim Families | Zakat Calculator, Hajj Savings

- Halal Grocery Budgeting: Why Muslim Families Spend More (and How to Plan for It) — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account