How to Calculate Zakat on a Savings Account

TL;DR:

- Zakat on savings accounts is 2.5% of your net liquid wealth after deducting short-term debts, payable annually if above the nisab threshold. All liquid assets, including foreign currency and digital wallets, are pooled and assessed together on your zakat date, with interest earned donated as charity. Using the silver nisab is recommended, and consistency in calculating on the hawl date simplifies fulfilling this obligation.

Zakat on savings accounts is defined as a 2.5% annual obligation on your net qualifying liquid wealth, payable once your total balance has exceeded the nisab threshold for a full lunar year (hawl). Savings accounts are treated as liquid monetary assets, placing them in the same category as cash held at home or in a digital wallet. To calculate zakat on a savings account, you need four pieces of information: your zakat anniversary date, your total combined balance across all accounts, any eligible short-term debts, and the current nisab value. This guide walks through each step so you can fulfill your obligation with confidence and clarity.

What accounts and assets count toward your zakat calculation?

All liquid zakatable assets must be combined into a single total before you test against the nisab threshold. This means you do not assess each account individually. Every qualifying account and holding is pooled together, and debts reduce the net total.

The following assets are included in your zakatable wealth:

- Savings accounts at any bank or credit union, regardless of account type or purpose label

- Checking accounts, including balances you use for everyday spending

- Money market accounts and high-yield savings accounts

- Cash held at home or in a physical wallet on your zakat date

- Digital wallets such as PayPal, Venmo, or Apple Cash balances

- Foreign currency holdings, converted to your local currency at the exchange rate on your zakat date

Earmarked or purpose-held money does not exempt it from zakat. If you have a savings account labeled “Hajj fund” or “emergency fund,” the balance still counts. The Islamic ruling does not recognize internal account labels as a basis for exclusion. The only valid deductions are eligible debts, which are addressed in the calculation steps below.

Multiple currencies require one extra step. Convert each foreign currency balance to your primary currency using the spot exchange rate on your zakat anniversary date, then add the converted amounts to your total. This keeps the calculation consistent and avoids discrepancies caused by currency fluctuation across the year.

How do you know if your savings meet the nisab threshold?

Nisab is the minimum wealth threshold that triggers a zakat obligation. Nisab equals 87.48 grams of gold or 612.36 grams of silver, valued at current market prices on your zakat due date. These two benchmarks produce different dollar amounts, and the gap between them can be significant depending on the gold-to-silver price ratio.

Most scholars recommend using the silver nisab when calculating zakat on cash and savings. The silver nisab is lower, which means more Muslims meet the threshold and fulfill their obligation. Using the gold nisab for cash savings can result in a higher cutoff that excludes wealth that Islamic jurisprudence generally considers zakatable.

To find the current silver nisab value, multiply 612.36 grams by the current silver spot price in your currency. Reputable sources such as the National Zakat Foundation and IslamicFinanceCalculator.com publish updated nisab values regularly. Check the value on your specific zakat date, not a general estimate from earlier in the year.

Pro Tip: Set a calendar reminder one week before your zakat anniversary date to look up the current nisab value. Silver prices shift daily, and using an outdated figure can lead to an incorrect calculation.

If your total net zakatable wealth falls below the nisab on your zakat date, no zakat is due for that year. The clock on your hawl also resets if your wealth drops below nisab at any point during the year, even if it recovers before your anniversary date.

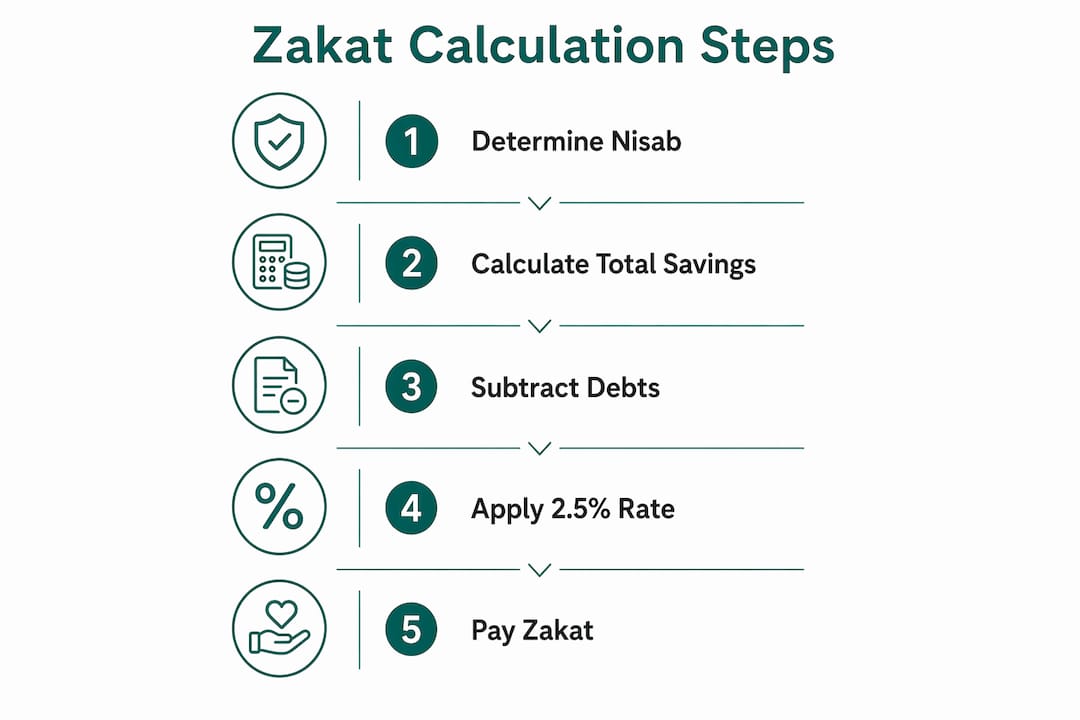

Step-by-step: how to calculate zakat on savings accounts

The correct zakat calculation uses the balance on your hawl date, not an average, highest, or lowest balance across the year. This is a common source of error. Pull your actual bank statement for that specific date.

Follow these steps in order:

- Set your zakat anniversary date (hawl). This is the date when your wealth first reached or exceeded the nisab. If you are unsure of the exact date, a consistent date like the first of Ramadan is widely accepted as a practical approximation.

- Gather all account balances on that exact date. Log into each bank account, check your statements, and record the closing balance for your hawl date.

- Add all balances together. Include cash at home, digital wallets, and converted foreign currency amounts.

- Subtract eligible short-term debts. Only debts due within the next 12 months reduce your zakatable total. Long-term liabilities like a mortgage reduce your zakat only by the installments due in the coming year, not the full outstanding balance.

- Compare your net total to the nisab. If your net wealth is below nisab, no zakat is due.

- Apply the 2.5% rate. Multiply your net zakatable wealth by 0.025 to find the amount owed.

Example calculation

| Item | Amount (USD) |

|---|---|

| Savings account balance | $12,000 |

| Checking account balance | $3,500 |

| Cash at home | $200 |

| Total gross zakatable wealth | $15,700 |

| Short-term debts due within 12 months | $1,200 |

| Net zakatable wealth | $14,500 |

| Nisab (silver, approximate 2026 value) | $550 |

| Zakat due (2.5% of $14,500) | $362.50 |

This table assumes the silver nisab is met and the hawl condition is satisfied. Adjust the debt figure to reflect only obligations due within the next year.

How should you handle interest (riba) on a conventional savings account?

Interest earned on conventional savings accounts is considered riba and must be given away as charity (sadaqah). It cannot be counted as personal income or retained as part of your wealth. This process is called tatheer, meaning purification, and it is separate from your zakat obligation.

Two approaches are widely accepted among scholars:

- Deduct interest before calculating zakat. Subtract the total interest earned during the year from your account balance before applying the 2.5% rate. This keeps the riba out of your zakatable base entirely.

- Pay zakat on the full balance, then donate interest separately. Calculate and pay zakat on the total balance including interest, then donate the interest amount to a non-profit or charitable cause as sadaqah.

“Separating the zakat obligation from the purification of unlawful income like interest helps avoid double counting and keeps the process ethically sound.” — Zakat and Purification Handling

Both approaches are valid. The key principle is that interest does not reduce your zakat principal but must be removed from your personal wealth through charitable giving. Keeping a record of interest earned throughout the year makes this straightforward at calculation time.

Pro Tip: If you hold a conventional savings account while transitioning to a halal-first financial setup, track your interest earnings monthly in a separate note or spreadsheet. This makes the tatheer process clean and stress-free at year end.

Special considerations: zakat on children’s savings accounts and multiple accounts

Zakat on a child’s savings account depends on ownership and the school of thought (madhab) you follow. Under the Hanafi madhab, minors are generally exempt from zakat until they reach puberty. Under the Maliki, Shafi’i, and Hanbali madhabs, a guardian is responsible for paying zakat on behalf of the child if the child’s wealth meets nisab and hawl conditions.

Ownership is the determining factor, not the account holder’s name. If a savings account is legally the child’s property, the ruling above applies. If the account is held in the child’s name but the funds are actually the parent’s savings, the parent pays zakat on those funds as part of their own zakatable wealth.

For households managing multiple accounts, the process is straightforward:

- Combine all personal savings accounts, checking accounts, and cash holdings into one total

- Do not calculate zakat separately on each account

- Use the same hawl date for all accounts to maintain consistency

- Convert foreign currency accounts before adding them to the total

- Apply a single nisab check and a single 2.5% calculation to the combined net figure

Consistency in your annual calculation date matters more than precision in tracking every fluctuation. Misunderstanding the hawl condition is one of the most common practical errors. Zakat is only due if your wealth has remained above nisab for the full lunar year. If it dipped below at any point, the hawl resets from the date it returned above nisab.

For families building a halal budgeting practice, maintaining a dedicated zakat record alongside your household budget removes the guesswork from this annual obligation.

Key takeaways

Accurate zakat on savings requires combining all liquid assets on your hawl date, subtracting only short-term debts, and applying 2.5% to the net total if it exceeds the silver nisab.

| Point | Details |

|---|---|

| Use the hawl date balance | Record the exact balance on your zakat anniversary date, not an average or estimate. |

| Silver nisab for cash savings | Most scholars apply the silver nisab (612.36 grams) to cash and savings accounts. |

| Combine all accounts | Pool every savings account, checking account, and cash holding before calculating. |

| Treat interest as riba | Donate interest earned as sadaqah separately; do not include it in your personal wealth. |

| Children’s accounts vary by madhab | Hanafi madhab exempts minors; other madhabs require guardian payment if nisab is met. |

My honest view on zakat and modern savings

I have worked with Muslim families on their finances long enough to know that zakat calculation anxiety is real. People delay, second-guess themselves, or avoid the calculation entirely because they are unsure whether they are doing it right. That hesitation is understandable, but it is also unnecessary.

The mechanics of zakat on savings are genuinely straightforward once you understand three things: the hawl date, the nisab threshold, and the treatment of debts. The complexity people feel usually comes from not having a consistent system, not from the calculation itself. If you set one annual date, pull your statements on that date every year, and keep a simple record of short-term debts and interest earned, the entire process takes under an hour.

The interest question is where I see the most confusion. Many people either ignore it entirely or overcomplicate it. The practical answer is simple: track your interest monthly, donate it to charity at year end, and keep a note of what you gave. That is tatheer done properly, without stress.

Technology genuinely helps here. A halal-first budgeting app that tracks your balances, flags interest income, and applies your preferred madhab’s rules removes most of the friction. The goal is not perfection on the first attempt. The goal is a consistent, honest practice that grows more confident each year. Zakat is an act of worship. Approach it with the same care you bring to salah, and the numbers will follow.

— Imran

Calculate your zakat with Amanahfund

Fulfilling your zakat obligation accurately starts with having the right tools. Amanahfund’s halal budgeting app is built specifically for Muslim families who want their financial tools to reflect their values. The zakat calculator inside Amanah Budget supports multiple madhabs, pulls live nisab values, and lets you aggregate balances across accounts so you always calculate from the correct figure.

Amanah Budget connects securely to your bank accounts through Plaid, categorizes transactions with halal-aware labels, and keeps your zakat records organized year over year. No ads, no interest-based products, and no selling your data. If you want a single place to manage your savings, track your zakat, and plan for Hajj or Eid, Amanah Budget is built for exactly that. Visit Amanahfund to get started.

FAQ

What is the zakat rate on a savings account?

Zakat on savings accounts is 2.5% of your net zakatable wealth, calculated on your zakat anniversary date after subtracting eligible short-term debts.

Does zakat apply to every savings account separately?

No. You combine all savings accounts, checking accounts, and cash holdings into one total, then apply a single nisab check and 2.5% calculation to the net figure.

What is the nisab threshold for savings in 2026?

Nisab for cash savings is typically based on the silver standard: 612.36 grams of silver valued at current market prices on your zakat due date. Check a current silver spot price to find the exact dollar amount.

Do I pay zakat on interest earned in my savings account?

Interest (riba) is not included in your zakatable wealth. You must donate it as sadaqah separately, either by deducting it before your zakat calculation or by giving it to charity after paying zakat on the full balance.

Is zakat due on my child’s savings account?

Under the Hanafi madhab, minors are generally exempt until puberty. Under the Maliki, Shafi’i, and Hanbali madhabs, a guardian pays zakat on the child’s behalf if the account meets nisab and hawl conditions.

Recommended

- How to Calculate Zakat on Your Wealth: A Complete 2026 Guide — Amanah Budget Blog

- How to Calculate Zakat on Your Wealth: A Complete 2026 Guide — Amanah Budget Blog

- Amanah Budget Blog — Islamic Finance, Zakat, and Halal Budgeting Guides

- Is Cryptocurrency Zakatable? What Muslim Investors Need to Know — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account