How Muslim couples can resolve budgeting disagreements

Money arguments are one of the most common sources of tension in any marriage, but for Muslim couples, the stakes feel especially high. You both want to do right by your family and your faith, yet disagreements over spending, saving, and financial priorities can escalate quickly, even when intentions are good. The challenge is real: modern financial pressures collide with Islamic obligations like nafaqah, zakat, and avoiding riba, and most budgeting advice out there simply does not account for those dimensions. As Islamic financial guidance notes, recurring, non-judgmental money conversations grounded in Islamic marital rights form the foundation for lasting financial harmony.

Table of Contents

- Start with Islamic financial rights and obligations

- Structure your household budget: transparency, autonomy, and fairness

- Communicate proactively: scheduled money check-ins and active listening

- Troubleshooting persistent disputes and Islamic fairness

- Budget around halal priorities: zakat, sadaqah, and interest-free savings

- What most guides miss: the real root of money fights in Muslim marriages

- Take your budgeting journey further with halal tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Clarify Islamic rights | Start every discussion by ensuring each spouse understands their Islamic financial duties and personal rights. |

| Balance transparency and privacy | Use agreed budget categories that provide visibility for joint needs but autonomy for personal spending. |

| Prioritize communication | Schedule regular, calm budget meetings using active listening to avoid reactive disputes. |

| Seek fairness and consultation | Always verify obligations are met and use mutual consultation for fairness before considering outside help. |

| Align with halal priorities | Center your budget around zakat, charity, and riba-free savings to foster faith and unity. |

Start with Islamic financial rights and obligations

Before you can resolve a budgeting disagreement, both spouses need to understand what Islam actually says about money in marriage. Many conflicts persist simply because couples are arguing preferences when they should first be clarifying rights and duties.

Nafaqah refers to the husband’s obligatory financial responsibility to provide for his wife and children. This covers housing, food, clothing, and other essential needs appropriate to his means. It is not optional, and it does not depend on whether the wife earns an income. Understanding this removes a major source of confusion: the husband’s income is not simply “shared money” by default.

Equally important is the principle of separate ownership. A wife’s wealth, whether inherited, earned, or gifted, belongs entirely to her. The husband cannot access or use it without her explicit permission. This is a protection, not a limitation. It means her voluntary contributions to household expenses are a gift, not an expectation.

The principle of shura (mutual consultation) applies directly to family financial decisions. Major budget choices, whether to take on debt, how to allocate surplus income, or how to plan for large expenses, should involve both spouses in honest dialogue. As Islamic financial resolution guidance notes, clarifying rights and obligations before debating preferences is the most effective starting point for resolving disputes.

Here is a quick reference for core Islamic financial principles in marriage:

| Principle | What it means in practice |

|---|---|

| Nafaqah | Husband provides essentials; wife’s income is her own |

| Separate ownership | Wife’s wealth requires her consent to use |

| Shura | Major financial decisions require mutual consultation |

| Amanah | Both spouses are trustees of household resources |

Pro Tip: Before your next money conversation, each spouse should write down what they believe their financial rights and responsibilities are. Comparing those lists often reveals where the real disagreement lives.

For a broader look at how these principles shape day-to-day decisions, the best budgeting strategy for Muslim families offers practical frameworks rooted in the same values.

Key points to carry into every financial discussion:

- Clarify Islamic obligations first before negotiating preferences

- Acknowledge that the wife’s financial contribution is always voluntary

- Use shura as a process, not just a concept

- Revisit these foundations whenever disagreements intensify

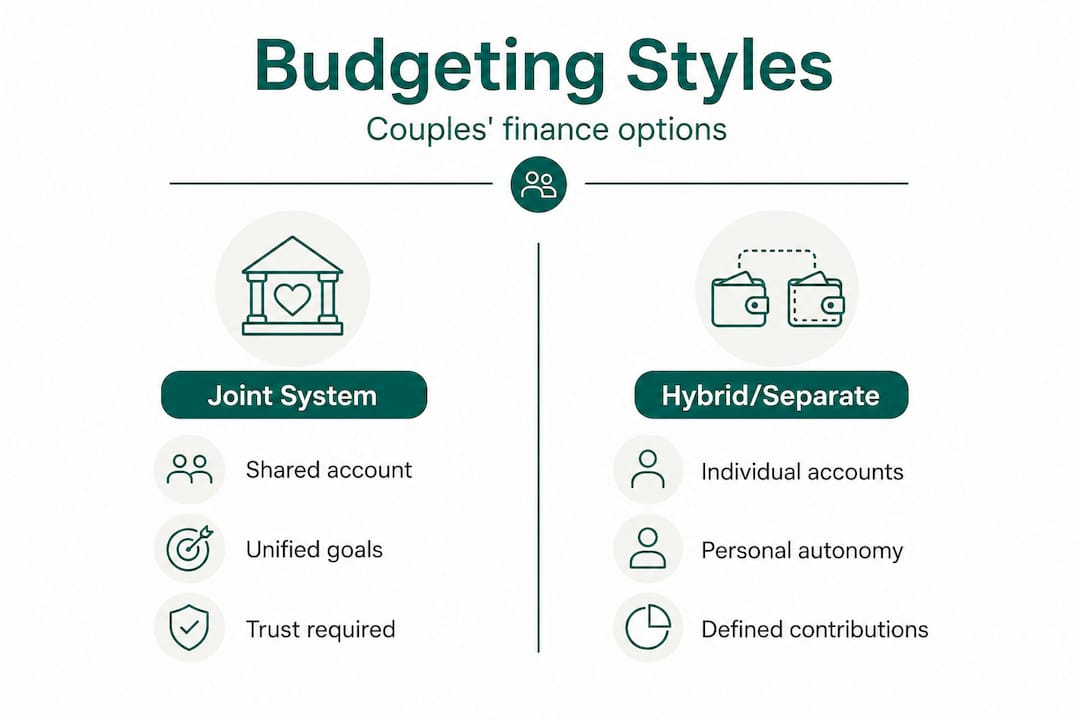

Structure your household budget: transparency, autonomy, and fairness

Once roles and responsibilities are clarified, couples can agree on a system that suits their unique situation. There is no single Islamic-mandated structure for how a couple manages their money day to day. What matters is that the system respects both spouses’ rights and is built on transparency.

There are three common approaches Muslim families use:

Joint budgeting means all income flows into shared accounts and all expenses are managed together. This works well when both spouses are aligned on financial values and trust each other’s spending habits. It requires strong communication and clear agreements about discretionary spending.

Hybrid budgeting combines a shared account for household expenses with individual accounts for personal spending. This is often the most practical model. Each spouse contributes an agreed amount to cover shared costs, and the remainder is theirs to manage independently. As financial transparency guidance notes, personal autonomy and shared visibility can coexist effectively when categories and boundaries are clearly defined.

Separate budgeting keeps finances largely independent, with agreed contributions to shared costs. This can work but requires very clear agreements about who covers what and how shortfalls are handled.

| System | Best for | Key requirement |

|---|---|---|

| Joint | High alignment, shared goals | Strong mutual trust |

| Hybrid | Different spending styles | Clear category agreements |

| Separate | Strong individual autonomy | Explicit contribution rules |

Importantly, Islamic sources confirm that no single account structure is mandated. The permissibility of any system depends on whether it upholds each spouse’s rights and avoids wrongdoing.

Regardless of which system you choose, these practices strengthen any budget structure:

- Define which categories are “household” versus “personal” in writing

- Set a spending threshold that requires joint approval, for example any single purchase over $200

- Review the budget structure every six months, not just when problems arise

- Keep shared visibility on essential expenses even if personal spending stays private

Pro Tip: Use a simple shared spreadsheet or a halal-first budgeting app to track household categories together. Visibility alone reduces most low-level spending friction.

When planning specific categories, resources like halal grocery budgeting tips and guidance on saving for Hajj can help you build realistic targets for the categories that matter most to your family.

Communicate proactively: scheduled money check-ins and active listening

Building a transparent budget is only effective when paired with open, structured discussion. Most money fights do not start at the budget. They start in the kitchen at 10 p.m. when one spouse discovers an unexpected charge. Reactive conversations are rarely productive.

The solution is to make money conversations scheduled and structured. Evidence-informed communication approaches show that shifting from reactive debate to calm, planned check-ins significantly reduces conflict and builds lasting financial trust.

Here is a practical process for monthly money meetings:

- Set a regular time. Choose a consistent day each month, perhaps the first Sunday after payday, when both spouses are rested and not rushed.

- Review the previous month. Look at actual spending versus the budget without blame. Focus on patterns, not individual purchases.

- Identify upcoming needs. Flag any large expenses, seasonal costs, or goal milestones coming in the next 30 to 60 days.

- Use the speaker-listener method. One spouse speaks while the other listens without interrupting. The listener then summarizes what they heard before responding. This single practice reduces defensive reactions dramatically.

- End with agreed actions. Every meeting should close with one or two specific decisions, not open questions.

“The goal of a money meeting is not to win an argument. It is to leave with a shared plan you both feel good about.”

Additional communication practices that help:

- Stick to facts and numbers during discussions, not characterizations of the other person’s habits

- Acknowledge emotional triggers before they escalate. If one spouse grew up in financial scarcity, spending anxiety is real and valid.

- Separate the “what happened” conversation from the “what should we do” conversation

- Use budgeting conversation templates to structure discussions until the habit feels natural

Pro Tip: If a conversation starts getting heated, agree in advance on a “pause signal.” Either spouse can call a 20-minute break, and the discussion resumes calmly. This is not avoidance. It is emotional intelligence in practice.

Troubleshooting persistent disputes and Islamic fairness

Even with proactive steps, some financial arguments require extra attention and outside wisdom. When disagreements become recurring or emotionally entrenched, a different approach is needed.

Start with a fairness checklist grounded in Islamic obligations:

- Are all nafaqah obligations being met? Is the wife receiving adequate provision for housing, food, and clothing?

- Is the wife’s wealth being accessed without her permission?

- Are both spouses’ voices genuinely heard in major financial decisions?

- Is any spouse hiding income, debt, or spending from the other?

If any of these questions reveal a gap, that gap is the real dispute. Addressing it directly, rather than debating specific amounts, usually moves things forward faster.

“When the disagreement is about fairness, the first question is always whether obligatory responsibilities are being met, not whether preferences are being satisfied.”

Islamic guidance on disputed household spending is clear: confirm obligatory responsibilities are met first, then use mutual consultation to agree on arrangements beyond those obligations. Taking unilateral action, such as redirecting funds without the other spouse’s knowledge, requires careful scholarly guidance and should not be done impulsively.

When disputes remain stuck despite honest effort, outside help is appropriate and wise. Couples financial therapy addresses both the relationship dynamics, including trust, emotional history, and communication patterns, and the practical financial picture, including budgets and debt. Look for a counselor who understands both financial planning and relationship dynamics. Ideally, find someone familiar with Islamic values or willing to respect them.

Signs it is time to seek outside help:

- The same argument repeats every month without resolution

- One spouse feels consistently unheard or dismissed

- Financial decisions are being made unilaterally and repeatedly

- Trust around money has broken down significantly

Budget around halal priorities: zakat, sadaqah, and interest-free savings

Aligning your budgeting process with faith priorities can proactively prevent and resolve financial tension. When a couple shares a clear commitment to halal financial values, many disputes dissolve before they start because the framework for decisions already exists.

Zakat is an obligation, not a preference. Building it into the budget as a fixed line item, calculated accurately using your preferred madhab, removes any negotiation about whether to give. It simply happens. For guidance on calculating zakat correctly, clear resources are available to help you arrive at the right number together.

Sadaqah (voluntary charity) can also be budgeted intentionally. Agreeing as a couple on a monthly sadaqah amount, even a modest one, builds a shared sense of generosity and purpose. It also shifts the conversation from “how do we spend less” to “how do we give more.”

Seasonal planning is one of the most overlooked tools for reducing financial conflict. Ramadan, Eid, and Hajj all bring predictable increases in spending. A halal savings approach that pre-funds these periods through dedicated savings goals eliminates the last-minute stress that so often triggers arguments. Set aside a fixed monthly amount throughout the year specifically for Ramadan and Eid expenses. By the time the season arrives, the funds are ready.

Avoiding riba (interest-bearing debt) is a shared Islamic obligation that also simplifies budgeting. When couples commit together to avoiding interest-based products, they naturally prioritize saving before spending and evaluate purchases more carefully. This shared constraint, embraced as a value rather than a restriction, creates alignment rather than conflict.

Practical steps to anchor your budget in halal priorities:

- Calculate and schedule zakat as a fixed annual or monthly budget line

- Set a monthly sadaqah amount you both agree on and automate it

- Open dedicated savings goals for Ramadan, Eid, Hajj, and Umrah

- Audit existing accounts and products for riba exposure and make a plan to exit them

- Use halal budgeting tools that reflect these priorities natively

What most guides miss: the real root of money fights in Muslim marriages

Most budgeting guides focus on systems and rules. They tell you to make a spreadsheet, categorize your spending, and have a weekly meeting. That advice is not wrong, but it misses something important.

The deepest financial conflicts in Muslim marriages are rarely about money. They are about trust, fear, and values alignment. A spouse who grew up in financial instability may hoard money not out of greed but out of anxiety. A spouse who gives generously may do so not recklessly but because generosity is a core part of their identity. When those patterns collide, no budget template fixes it.

We have seen couples who follow every practical step correctly and still argue constantly. The reason is almost always that one or both spouses have unspoken fears they have never named out loud. Fear of poverty. Fear of losing control. Fear of not being trusted. These fears drive behavior in ways that look like financial disagreement but are actually emotional wounds.

The fix is not more rules. It is more honesty. Couples who build lasting financial harmony tend to share a vision, not just a budget. They talk about what they want their family’s life to look like in ten years. They discuss what money represents to each of them. They revisit those conversations regularly, not just when things go wrong.

Islamic values actually provide a powerful framework for this deeper work. The concept of amanah (trust and stewardship) reminds both spouses that money is not theirs to own but to manage responsibly. Shura is not just a decision-making tool; it is a practice of genuine respect for the other person’s perspective. When couples internalize these values rather than just citing them in arguments, the tone of every money conversation changes.

The Muslim budgeting perspectives that work long-term are the ones built on shared vision and recurring consultation, not perfect spreadsheets. Numbers matter. Systems matter. But the spirit behind them matters more.

Take your budgeting journey further with halal tools

Putting all of this into practice is much easier when your tools are built for your values. Most budgeting apps were not designed with Muslim families in mind. They do not account for zakat, they do not have Hajj savings goals, and they certainly do not distinguish between halal and non-halal spending categories.

The Amanah Budget halal budgeting app was built specifically for Muslim households. It brings together halal-aware spending categories, zakat calculation by madhab, dedicated savings goals for Hajj, Umrah, Ramadan, and Eid, and shared household budgets that both spouses can access. Accounts connect securely through Plaid, and AI-powered categorization helps you see your spending patterns clearly. No ads, no data selling, no interest-based products. If you want a strategy guide for Muslim families to complement the app, that resource walks through practical frameworks in detail.

Frequently asked questions

Does Islam require all finances to be joint in marriage?

No, Islam does not require joint finances. Separate, joint, or hybrid systems are all permissible as long as mutual rights are respected and neither spouse is wronged in the process.

What if spouses disagree on big purchases?

Agree in advance on a spending threshold that requires joint approval, and use shura for anything above it. Defining agreed categories and boundaries for discretionary spending before disagreements arise is the most effective approach.

Can a wife use her own money for family expenses without being asked?

She may do so entirely voluntarily, but her wealth cannot be obligated without her explicit permission under Islamic law. Any contribution she makes is a gift, not a requirement.

What type of financial help should a couple seek if issues persist?

Look for couples financial therapy that addresses both relationship dynamics and practical financial planning. Ideally, choose a counselor who is familiar with or respectful of Islamic values.

How should couples budget for zakat and seasonal spending?

Set aside a fixed monthly amount throughout the year in a dedicated savings goal for zakat and seasonal expenses. A halal savings approach that pre-funds Ramadan and Eid prevents last-minute financial stress and the arguments that come with it.

Recommended

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- Halal Grocery Budgeting: Why Muslim Families Spend More (and How to Plan for It) — Amanah Budget Blog

- Amanah Budget Blog — Islamic Finance, Zakat, and Halal Budgeting Guides

- Amanah Budget — Halal Budgeting App for Muslim Families | Zakat Calculator, Hajj Savings

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account