Household halal spending: a guide for Muslim families

Halal spending is not a weekend consideration for most Muslim families in the U.S. It shapes what goes in the grocery cart, which personal care products sit on the bathroom shelf, and how charitable giving gets scheduled throughout the year. Yet most mainstream budgeting advice treats it as an afterthought, if it acknowledges it at all. According to 83% of U.S. Muslims, halal preferences are integrated into routine, everyday spending, not just special occasions. This guide explains what household halal spending actually means, what it costs, and how to manage it with intention.

Table of Contents

- Understanding what household halal spending means

- How halal certification and preferences shape your household budget

- Budgeting for halal essentials and religious obligations

- Managing seasonal halal spending spikes during Ramadan and Eid

- Practical tips for effective household halal budgeting

- Why typical budgeting advice misses the mark on halal household spending

- Streamline your household halal spending with Amanah Budget

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Halal spending is daily | Most U.S. Muslim families integrate halal spending into everyday household budgets, not just special occasions. |

| Halal products cost more | Certified halal items usually have a 20–30% price premium impacting budget planning. |

| Plan for religious obligations | Zakat and Sadaqah are fixed budget items that must be scheduled, not treated as discretionary expenses. |

| Seasonal spikes require foresight | Ramadan and Eid increase household halal spending by 30–50%, so pre-funding is essential. |

| Use halal budgeting tools | Dedicated budgeting apps and sinking funds help avoid interest debt and stay aligned with Islamic principles. |

Understanding what household halal spending means

For Muslim families in the U.S., household halal spending means allocating budget toward halal-permissible goods and services across every category of daily life, not just food. It is a religious obligation, not a lifestyle preference, and it touches nearly every purchase a household makes.

Most people outside the community assume halal spending begins and ends at the meat counter. That assumption misses the full picture. Halal guidelines apply to ingredients in packaged foods, alcohol content in personal care products, gelatin in vitamins and supplements, and even the financial products a family uses. This is why halal grocery budgeting is only one piece of a much larger puzzle.

Here is what household halal spending typically covers:

- Food and groceries: Halal-certified meat, poultry, and packaged goods free from prohibited ingredients like pork derivatives or alcohol

- Personal care and cosmetics: Products without animal-derived ingredients from non-halal sources or alcohol-based components

- Medications and supplements: Checking for gelatin capsules or alcohol-based syrups, which may require halal alternatives

- Household products: Some cleaning products contain animal fats; halal-conscious families review ingredient labels

- Financial services: Avoiding interest-bearing accounts, credit products, or investments in prohibited industries

- Religious obligations: Zakat (annual almsgiving), sadaqah (voluntary charity), and savings for Hajj or Umrah

Understanding this scope is the first step toward building a budget that actually reflects your family’s values.

How halal certification and preferences shape your household budget

Not every Muslim family follows the same standard of halal certification, and that variation has a direct impact on household spending. 37% of Muslims only buy products with recognized halal certification, while 46% mostly prefer certified products but will purchase uncertified items if they are not clearly prohibited. That gap in preference creates real differences in how much families spend and where they shop.

Understanding these preferences is key to accurately mapping out your halal household expenses.

How certification levels affect spending:

| Certification approach | Typical shopping behavior | Estimated cost impact |

|---|---|---|

| Strict certified-only | Specialty halal stores, select online retailers | 20 to 30% premium on most items |

| Prefer certified, flexible | Mix of halal stores and mainstream grocery | 10 to 20% premium on select items |

| Ingredient-based review | Mainstream grocery with label checking | Minimal premium, higher time cost |

| Community-trusted sources | Local halal butchers, community-verified brands | Variable, often competitive |

Certified halal products carry a 20 to 30% price premium over conventional alternatives, particularly for protein items like chicken and beef. That premium exists because halal certification involves third-party audits, specialized slaughter practices, and supply chain oversight, all of which add cost.

The certification landscape in the U.S. also adds complexity. Multiple private certifying bodies operate here, each with different standards and logos. Families who recognize one certifier may not trust another, which limits where they can shop and drives up costs when preferred products are unavailable locally.

Key factors that shape your halal spending budget:

- Which certifying bodies your family trusts

- Proximity to halal grocery stores or butchers

- Whether you buy in bulk to reduce per-unit costs

- How strictly you apply halal standards to non-food categories

Pro Tip: Build a short list of three to five halal certification logos your family accepts. Keeping this list consistent across all household shoppers reduces confusion, prevents duplicate purchases, and makes budgeting more predictable month to month.

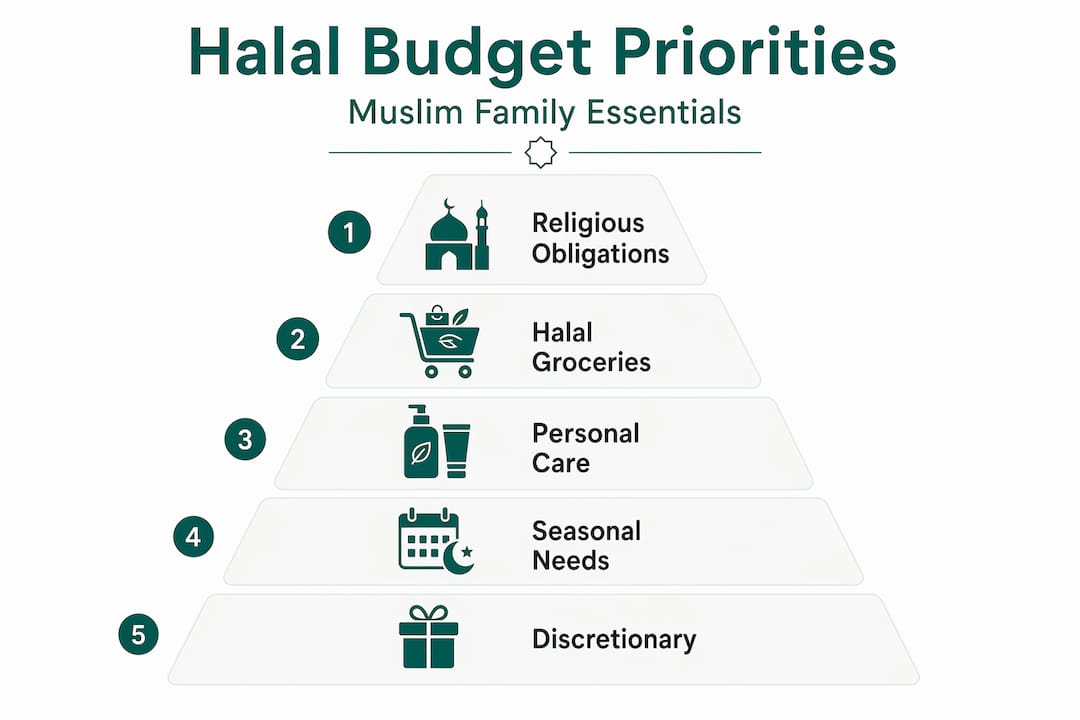

Budgeting for halal essentials and religious obligations

With essentials and obligations defined, let’s examine how seasonal events affect halal spending patterns.

Islamic financial planning draws a clear line between two categories: what you need to live and what your faith requires you to give. Islamic budgeting treats obligations such as zakat and sadaqah as scheduled, non-negotiable parts of the household budget, placed alongside rent and groceries, not lumped in with discretionary spending.

This framing matters. When zakat is treated as optional or variable, it often gets delayed or underfunded. When it is a fixed line item, it gets paid on time and without stress.

How to structure your halal household budget:

- Halal essentials: Groceries, personal care, household products, and utilities that meet halal standards

- Religious obligations: Zakat (calculated annually on eligible wealth), Zakat al-Fitr (paid before Eid al-Fitr), and regular sadaqah

- Savings for religious milestones: Dedicated funds for Hajj, Umrah, Ramadan hosting, and Eid gifts

- Future growth: Halal investment accounts, education savings, and emergency funds held in interest-free accounts

- Lifestyle and discretionary: Dining out at halal restaurants, entertainment, and travel

Understanding how to calculate zakat is essential before you can budget for it accurately. Zakat is typically 2.5% of eligible wealth held above the nisab (minimum threshold) for one lunar year. For many families, this is a meaningful annual sum that deserves its own savings envelope.

Sadaqah, by contrast, is voluntary and can be given at any frequency. Many families budget a fixed monthly amount, treating it like a utility bill, because consistency builds the habit and prevents end-of-year scrambling.

Religious financial obligations to include in your budget:

- Annual zakat on savings, gold, and business inventory

- Zakat al-Fitr per family member before Eid al-Fitr

- Monthly or weekly sadaqah allocation

- Kaffarah (expiation payments) if applicable

- Contributions to local masjid or Islamic school

The best budgeting strategy for Muslim families keeps these obligations visible and funded before discretionary spending begins.

Managing seasonal halal spending spikes during Ramadan and Eid

Ramadan and Eid are the two largest household budget events of the Islamic calendar. During Ramadan, U.S. Muslim households increase grocery spending by 30 to 50 percent for iftar hosting, special foods, Eid gifts, and community contributions. That is not a small variance. For a family spending $800 per month on groceries, Ramadan can push that figure to $1,100 or more, before adding gifts and charitable giving.

Typical Ramadan and Eid spending increases by category:

| Spending category | Average monthly baseline | Ramadan/Eid increase | Estimated spike |

|---|---|---|---|

| Groceries and iftar food | $700 to $900 | 30 to 50% | $210 to $450 |

| Charitable giving and zakat | Variable | Significant increase | $200 to $1,000+ |

| Eid gifts and clothing | $0 | New expense | $150 to $500 |

| Hosting and entertaining | Minimal | Large increase | $100 to $400 |

Seasonal budgeting adds complexity, so let’s discuss practical tips to implement a halal spending plan that works year-round.

How to plan for Ramadan and Eid without financial stress:

- Start a Ramadan sinking fund in Shawwal (the month after Eid). Divide your expected Ramadan budget by 11 and save that amount monthly.

- Separate iftar hosting costs from zakat obligations. They are both Ramadan expenses but serve different purposes and should be tracked separately.

- Pre-purchase non-perishable halal pantry items in the months before Ramadan when prices are lower.

- Set a firm Eid gift budget per child or family unit before shopping begins, not after.

- Automate your Zakat al-Fitr payment by calculating the amount in advance and scheduling it before the last days of Ramadan.

“Pre-funding Ramadan from a dedicated halal savings account is not just a financial best practice. It is a way to protect your ibadah from financial distraction during the most spiritually important month of the year.”

Pro Tip: Use the Ramadan budgeting strategy approach of creating two separate Ramadan envelopes: one for household food and hosting, and one for all charitable giving. This prevents your sadaqah budget from quietly absorbing grocery overruns.

Practical tips for effective household halal budgeting

Having practical budgeting tools, let’s now reflect on how these approaches align with Islamic financial values and modern realities.

Successful halal budgeting uses repeatable mechanisms like sinking funds to manage essentials separately from periodic spikes, preventing families from making non-halal compromises or taking on debt when costs rise unexpectedly.

Core halal budgeting habits to build:

- Standardize your certification list. Decide which halal labels your household trusts and stick to them. This reduces impulse substitutions that blow the budget.

- Use sinking funds for every predictable halal expense. Ramadan, Eid, Hajj savings, annual zakat, and back-to-school halal lunch supplies all qualify.

- Review your halal grocery budgeting quarterly. Halal product availability and pricing shift. A brand you relied on may lose certification, or a better-priced option may enter your local market.

- Avoid interest-bearing debt for halal purchases. If you cannot pre-fund a halal expense, that is a signal to adjust the budget, not to use a conventional credit card.

- Involve your spouse in the budget. Shared visibility on halal spending decisions prevents conflicts when one partner makes a substitution the other would not approve.

- Track non-food halal spending separately. Personal care, supplements, and financial services are easy to overlook but add up meaningfully over the year.

Understanding halal budgeting best practices also means recognizing that your budget will need to evolve. Certification standards shift, family size changes, and income fluctuates. A halal budget is a living document, not a one-time setup.

Pro Tip: Review your Muslim family budgeting tips every six months alongside a full pantry audit. You will often find expired halal products you replaced with non-halal alternatives out of convenience, a pattern worth correcting at the budget level rather than the checkout line.

Why typical budgeting advice misses the mark on halal household spending

Most mainstream budgeting frameworks were not built with Muslim families in mind. They treat food as one line item, charitable giving as optional, and financial products as interchangeable. None of those assumptions hold for a halal household.

The biggest gap is the failure to account for certification complexity. When a conventional budget app categorizes a grocery run, it does not distinguish between halal-certified chicken at $7.99 per pound and conventional chicken at $4.99 per pound. That $3.00 difference, multiplied across a month of meals, is a meaningful budget variance that goes invisible in generic tools.

The second gap is treating religious obligations as discretionary. Zakat is not a donation. It is a pillar of Islam with a precise calculation method and a due date. When it sits in the same budget category as charitable impulse giving, it tends to get underfunded or delayed. Separating it is not just organizationally tidy; it is religiously significant.

The third gap is the seasonal blindspot. Generic budgeting advice acknowledges holiday spending in November and December. It has no framework for Ramadan, Eid al-Fitr, Eid al-Adha, or the multi-year savings horizon of Hajj. These are not minor adjustments. They are structural features of a Muslim family’s financial year.

The solution is not to force halal household spending into a generic framework and hope it fits. The solution is to use Islamic budgeting principles that were designed with these realities from the start. That means treating zakat as a fixed obligation, building Ramadan sinking funds into the annual calendar, and using tools that recognize halal-aware spending categories as a default, not a workaround.

Streamline your household halal spending with Amanah Budget

Managing halal household expenses across food, personal care, religious obligations, and seasonal events is genuinely complex. Generic budgeting apps were not designed for it, and spreadsheets do not scale well when you are tracking zakat, sinking funds, and shared family spending at the same time.

Amanah Budget is built specifically for Muslim families who want their financial tools to reflect their values. The app includes halal-aware spending categories, built-in zakat calculation across different madhabs, and dedicated savings goals for Ramadan, Eid, Hajj, and Umrah. You can share your household budget with your spouse, connect your bank accounts securely, and let AI-assisted categorization handle the transaction sorting. Explore the halal grocery budgeting blog and the best budgeting strategy blog for more guidance built around your deen and your dunya. No ads. No interest-based products. No compromises.

Frequently asked questions

What does household halal spending include?

Household halal spending includes all purchases a family makes that comply with halal guidelines, such as halal-certified food, personal care products, and religious obligations like zakat and sadaqah. It covers both everyday essentials and periodic religious financial duties.

How much more do halal products typically cost?

Halal products often cost 20 to 30% more than non-halal alternatives, especially for protein items like chicken, due to certification audits and specialized production requirements.

How should Muslim families budget for Ramadan expenses?

Muslim families should pre-fund Ramadan costs using dedicated halal savings accounts, covering iftar hosting, zakat obligations, daily sadaqah, and Eid gifts well before the month begins to avoid debt and financial stress.

What are practical tips for halal budgeting?

Standardize trusted halal certification labels, use sinking funds for essentials and seasonal spikes like Ramadan, automate religious giving as a fixed line item, and avoid interest-bearing debt by planning all major halal expenses in advance.

Recommended

- Halal Grocery Budgeting: Why Muslim Families Spend More (and How to Plan for It) — Amanah Budget Blog

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- Amanah Budget Blog — Islamic Finance, Zakat, and Halal Budgeting Guides

- How Much Does Hajj Cost and How to Save for It: A Practical Guide — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account