Household budget share: A guide for Muslim families

Most people think budgeting is just math. Add up your income, divide your expenses into categories, and you’re done. But that assumption breaks down quickly when you look closely at what “household budget share” actually means, and it breaks down even faster when your household has religious obligations that most budgeting frameworks completely ignore. For Muslim families in the US, categories like Zakat, halal food sourcing, Hajj savings, and avoiding israf (extravagance) change the entire picture. This guide walks through both the standard US benchmarks and a faith-aligned approach to help your family budget with intention.

Table of Contents

- What does household budget share mean?

- Typical household budget shares in the US

- How Islamic values shape household budget shares

- Applying budget share principles in your Muslim household

- A fresh perspective: Why generic budgets don’t fit Muslim households

- Take your faith-first budgeting to the next level

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Budget share defined | Household budget share is the percentage of income or spending allocated to each key category. |

| US benchmarks | Typical American households spend over 50% on housing and transportation combined, with benchmarks for other categories. |

| Faith-aligned allocations | Islamic values require prioritizing Zakat, charity, and avoiding extravagance in budget shares. |

| Select the right denominator | Using disposable income or total spending changes your budget share calculations and insights. |

| Practical steps for Muslims | Set fixed shares for obligations, then tailor other spending to your family’s needs and values. |

What does household budget share mean?

The term sounds technical, but the core idea is simple. Household budget share typically means the portion of a household’s income or total spending allocated to a particular category. Housing, food, transportation, healthcare — each one takes a slice of your financial resources, and that slice is your budget share for that category.

Where it gets nuanced is the denominator. Are you measuring each category as a share of total spending, or as a share of disposable income (your take-home pay after taxes)? These two approaches give you different numbers and different insights.

For example, food as a share of disposable personal income tells you how much of what you actually earn goes toward feeding your family. That’s a different story than food as a share of total spending, which only accounts for what you already spent. For Muslim families practicing Muslim budgeting strategies rooted in Islamic values, using disposable income as the denominator tends to be more useful because it forces you to see obligations like Zakat in the context of what you actually have available.

Here’s a quick breakdown of the two main approaches:

| Denominator | What it measures | Best used for |

|---|---|---|

| Total household spending | Share of what you actually spent | Comparing category priorities |

| Disposable (after-tax) income | Share of what you earned and kept | Planning obligations and savings |

| Gross income | Share of total earnings before tax | High-level financial awareness |

Common budget categories include:

- Housing (rent or mortgage, utilities, maintenance)

- Food (groceries and dining out)

- Transportation (car payments, fuel, public transit)

- Healthcare (insurance premiums, out-of-pocket costs)

- Personal insurance and pensions (retirement contributions)

- Charity and religious obligations (Zakat, sadaqah, masjid donations)

The last category is rarely included in mainstream budgeting frameworks. For Muslim families, it belongs near the top of the list. Explore the full range of Islamic budgeting guides to see how these categories are structured in a faith-first context.

“The way you define your denominator shapes the story your budget tells. Choose the one that reflects your actual financial reality and your obligations.”

Typical household budget shares in the US

Before adjusting for Islamic values, it helps to understand what the average US household looks like. The Bureau of Labor Statistics (BLS) publishes Consumer Expenditure Survey data every year, and the 2024 numbers reveal a lot about national spending priorities.

In 2024, housing averaged 33.4% and transportation 17.0% of total US household spending. Together, those two categories alone consumed half of what the average American household spent. That leaves roughly 50% for everything else: food, healthcare, education, entertainment, and savings.

2024 US household spending shares (BLS data)

| Category | Share of total spending |

|---|---|

| Housing | 33.4% |

| Transportation | 17.0% |

| Food | 12.9% |

| Personal insurance and pensions | 12.5% |

| Healthcare | 8.0% |

| Entertainment | 4.7% |

| Apparel and services | 2.5% |

| Other | ~9.0% |

BLS also reports that food accounts for 12.9% and personal insurance and pensions for 12.5% of total spending. Notice what’s missing from this national picture: no category for religious obligations, no line item for charity, and no distinction between halal and non-halal food sourcing.

For Muslim families, these benchmarks are useful as a starting reference, but they are not a template. They reflect the average American household, which has very different priorities and obligations than a practicing Muslim family.

Key observations from US benchmarks:

- Housing is the single largest expense for most households and likely will be for yours too

- Transportation costs are significant and often underestimated

- The “personal insurance and pensions” category is where retirement savings typically live

- There is no dedicated charity or religious obligation category in standard US data

When you look at halal grocery budgeting, for instance, the food share for Muslim families often runs higher than the 12.9% national average because halal-certified products tend to cost more and require more intentional sourcing. That’s a real budget difference worth planning for.

Statistic to keep in mind: The average US household spent over $77,000 in 2024 according to BLS data. At that level, housing alone averaged around $25,700 per year. Understanding where your family sits relative to these benchmarks helps you identify where adjustments are needed.

How Islamic values shape household budget shares

This is where budgeting for Muslim families becomes genuinely different from mainstream financial planning. Islamic values don’t just add a few extra line items. They reorder the entire priority structure of your household budget.

Budgeting shares should incorporate fixed obligations like Zakat and charity, while avoiding extravagance and non-halal priorities. This isn’t a suggestion. In Islamic financial thinking, obligations come before preferences, and giving comes before spending on wants.

Here’s how the major Islamic principles translate into specific budget share adjustments:

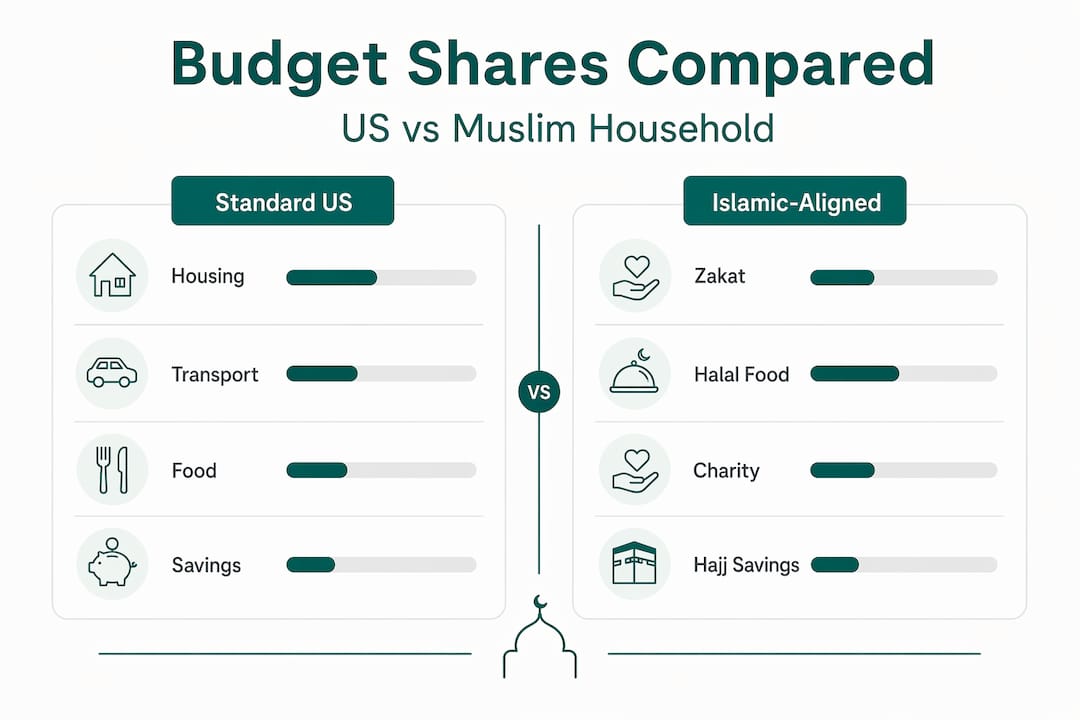

Comparison: Standard US budget vs. Islamic-aligned budget

| Category | Standard US approach | Islamic-aligned approach |

|---|---|---|

| Charity/Zakat | Minimal or absent | Fixed obligation, allocated first |

| Food | Any source | Halal-certified, may cost more |

| Entertainment | Broad category | Filtered for halal permissibility |

| Savings goals | Retirement-focused | Includes Hajj, Umrah, Eid, Ramadan |

| Financial products | May include interest | Avoids riba (interest-based products) |

| Extravagance | Personal choice | Actively limited (avoiding israf) |

The concept of israf (extravagance or waste) is central to faith-first budgeting. Islam teaches moderation in spending. That means your entertainment category, your clothing budget, and even your food spending should reflect need and reasonable comfort, not excess.

Zakat (obligatory almsgiving) is typically 2.5% of your total eligible wealth held above the nisab (minimum threshold) for one lunar year. For many families, this is a meaningful annual obligation. If you don’t plan for it in your budget, it either doesn’t get paid on time or it disrupts other financial goals. Use a Zakat calculation guide to determine your exact obligation based on your assets.

Sadaqah (voluntary charity) is separate from Zakat and reflects your family’s ongoing generosity. Many Muslim families set a sadaqah budget share of 1% to 5% of monthly income, in addition to their annual Zakat.

Hajj and Umrah savings are another category that simply doesn’t exist in standard budgeting frameworks. For a family of four planning Hajj, costs can exceed $20,000 to $30,000 or more. That requires a dedicated savings category, not a vague “travel” bucket.

Pro Tip: Treat Zakat, sadaqah, and Hajj savings as fixed obligations in your budget, not optional line items. Allocate them before you plan discretionary spending. This mirrors the Islamic principle of giving before indulging.

Applying budget share principles in your Muslim household

Understanding the framework is one thing. Putting it into practice is another. Here is a step-by-step process for building a faith-aligned household budget share system.

1. Start with your disposable income

Calculate your monthly take-home pay after taxes. This is your real working number. Everything else is a percentage of this figure.

2. Allocate fixed religious obligations first

Before anything else, set aside your Zakat estimate (calculated annually but tracked monthly), your sadaqah goal, and your Hajj or Umrah savings contribution. These are not negotiable. They come first.

3. Cover essential needs

Housing, utilities, halal groceries, transportation, and healthcare come next. Use the US benchmarks as a rough guide, but adjust upward for halal food costs and downward for any categories where Islamic values call for moderation.

4. Plan for Islamic seasonal goals

Ramadan, Eid, and other Islamic observances bring real costs: food, gifts, travel, and charitable giving. Budget for these explicitly rather than letting them create financial stress.

5. Allocate for savings and education

Retirement savings, children’s education funds, and emergency reserves belong in this layer. Islamic finance encourages building financial resilience, so an emergency fund of three to six months of expenses is a strong goal.

6. Assign the remainder to wants and discretionary spending

Whatever is left after obligations, needs, and savings can go toward wants. This might include halal entertainment, dining out, hobbies, and home improvements. The key is that wants come last.

Islamic financial management emphasizes monitoring expenses and setting aside funds for obligations like Zakat while actively avoiding wastefulness. Regular monthly reviews of your spending against your budget shares are essential. If your food category is running 20% over budget, that’s a signal to investigate, not ignore.

“A budget that reflects your values is not a restriction. It is a map that shows you where your money is going and whether it aligns with what matters most to your family.”

Saving for Hajj deserves special mention. If you plan to perform Hajj in the next five to ten years, calculate the estimated cost, divide by the number of months remaining, and make that a fixed monthly savings contribution. Explore strategies for saving for Hajj to build a realistic plan.

Pro Tip: Review your household budget shares quarterly, not just monthly. Quarterly reviews help you catch seasonal drift (like Ramadan spending) and recalibrate before small overages become large ones.

A fresh perspective: Why generic budgets don’t fit Muslim households

Most mainstream budgeting advice is built around a secular, consumption-driven model of household finance. The implicit assumption is that your money is yours to spend however you want, and the goal is simply to spend less than you earn. That’s not wrong, but it’s incomplete.

For Muslim families, money is an amanah, a trust. You are a steward of your wealth, not its ultimate owner. That changes everything about how you approach budget shares. It means you have obligations that come before your preferences. It means certain categories of spending are simply off the table. And it means your savings goals include spiritual milestones, not just financial ones.

The danger of treating Zakat as optional or “something we’ll figure out at the end of the year” is real. When Zakat is not planned for, it often gets underpaid, delayed, or calculated incorrectly. Treating Zakat and charity as intentional allocations rather than afterthoughts is not just good financial practice. It is an act of worship.

Generic budgeting apps and frameworks also fail to account for the community dimension of Muslim household finance. Many families support extended family members, contribute to their local masjid, and participate in community fundraising. These are not edge cases. They are core features of Muslim financial life that deserve their own budget categories.

The families who thrive financially while honoring their deen are the ones who reject the idea that mainstream budgeting advice is a neutral, one-size-fits-all solution. They build tailored budgeting for Muslims that reflects their actual obligations, values, and goals. That intentionality is what separates a budget that causes stress from one that brings clarity and peace of mind.

Take your faith-first budgeting to the next level

Building a faith-aligned budget from scratch takes effort, especially when your tools weren’t designed with your values in mind.

That’s exactly why Amanah Budget exists. Our halal budgeting app is built specifically for Muslim families in the US, with halal-aware spending categories, built-in Zakat calculation across different madhabs, and dedicated savings goals for Hajj, Umrah, Ramadan, and Eid. You can share your household budget with your spouse, connect your bank accounts securely through Plaid, and let AI-assisted categorization do the heavy lifting on transaction tracking. No ads, no data selling, no interest-based products. Just a tool that reflects your values. Explore our full library of Islamic budgeting resources to go deeper on every topic covered in this guide.

Frequently asked questions

How do you define “budget share” in a household context?

Budget share is the percentage of household income or total spending allocated to each category, such as housing, food, or charity. It helps families understand where their money goes and whether spending aligns with their priorities.

What denominator should Muslim families use for budget share — income or spending?

Both are valid, but disposable income is often more useful for intent-driven Islamic budgeting because it shows how obligations like Zakat and savings relate to what you actually bring home after taxes. The denominator you choose changes the percentages and the story they tell.

How should Zakat and charity be included in budget share calculations?

Allocate Zakat and charity as fixed categories before planning any discretionary spending. This reflects the Islamic principle that obligations come before preferences and ensures these duties are never overlooked.

How are halal grocery expenses different in budget shares?

Halal grocery spending often runs higher than the US average of 12.9% of total spending because halal-certified products cost more and require more intentional sourcing. Muslim families should plan for a higher food budget share than national benchmarks suggest.

Can a budget share help track and control wastefulness (israf)?

Yes. Setting clear budget shares and reviewing them regularly prevents extravagance and keeps spending aligned with Islamic teachings on moderation. A visible budget share makes overspending harder to ignore.

Recommended

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- Halal Grocery Budgeting: Why Muslim Families Spend More (and How to Plan for It) — Amanah Budget Blog

- Amanah Budget Blog — Islamic Finance, Zakat, and Halal Budgeting Guides

- Amanah Budget — Halal Budgeting App for Muslim Families | Zakat Calculator, Hajj Savings

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account