What is a family financial council: A guide for Muslim families

Most Muslim families in the US already talk about money. But talking about money and governing your finances are two very different things. A family financial council is not a casual dinner conversation about bills. It is a structured governance body with defined roles, scheduled meetings, and real decision-making authority. Understanding what is a family financial council, and why it matters specifically for Muslim families, can be the difference between finances that drift and finances that reflect your values with intention.

Table of Contents

- Understanding the family financial council

- The role of family financial councils in multi-generational families

- Aligning family finances with Islamic principles through a family council

- How to establish and run a family financial council effectively

- Practical financial planning within the family financial council framework

- Why a family financial council is a game-changer for Muslim families’ financial harmony

- Explore Amanah Budget for halal financial planning support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Defines family financial council | A family financial council is a small, elected governance body that aligns family financial decisions with shared values. |

| Supports multi-generational unity | Councils help growing families stay connected, resolve conflicts, and maintain value-aligned decision making. |

| Aligns finances with Islam | Muslim families use councils to operationalize halal income, avoid interest, budget, pay zakat, and ensure Sharia compliance. |

| Governance best practices | Effective councils have clear member terms, meeting cadences, advisers, stipends, and separate decision/informational forums. |

| Practical planning tools | Family councils can implement budgeting, saving, investing, and long-term goal plans consistent with Islamic principles. |

Understanding the family financial council

A family financial council is a formal governance structure, not a suggestion box or a one-time family meeting. A family council is a structured group of family members that creates a forum for decision-making, functioning like a board of directors for your household or extended family. That framing is important. It means the council carries real responsibility, not just good intentions.

Here is what a well-formed family financial council typically looks like in practice:

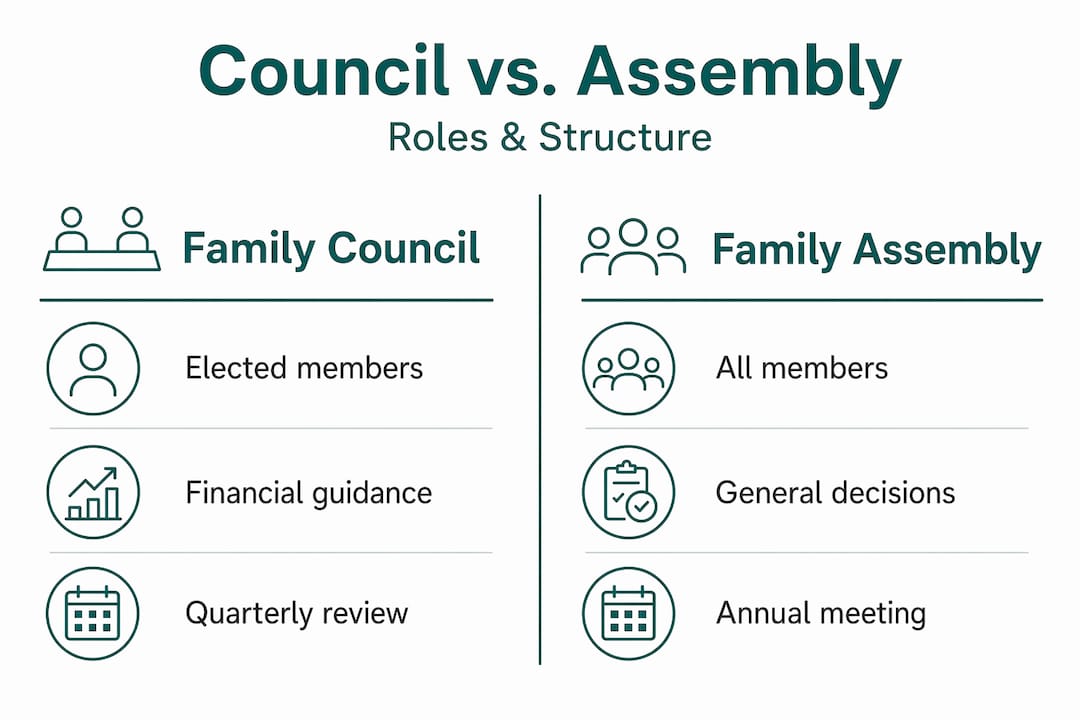

- Size: 5 to 9 elected or appointed family members, ensuring diverse representation without becoming unmanageable

- Meeting cadence: Quarterly council meetings for active decisions, with an annual family assembly for broader updates and input

- Defined roles: A chair, a secretary, and a treasurer at minimum, with clear responsibilities for each

- Term limits: Members typically serve 2 to 3 year terms, which keeps perspectives fresh and prevents one person from dominating decisions

- Governance documents: A written charter or constitution that outlines the council’s purpose, rules, and decision-making process

The distinction between this and a casual family meeting matters enormously. A casual meeting produces conversation. A council produces decisions, accountability, and follow-through. For Muslim families thinking about budgeting strategy for Muslim families, this structure provides the foundation that makes any financial plan actually stick. You can also build on this with resources like personal finance mastery to deepen your household’s financial knowledge.

The role of family financial councils in multi-generational families

The importance of a family financial council grows significantly when your family spans multiple generations. Adult children, parents, grandparents, and even adult siblings may all have stakes in shared financial decisions, whether that involves inherited property, pooled savings, or business interests. Without a formal structure, these conversations tend to happen inconsistently or not at all, which creates friction.

Councils help keep family members connected, provide a platform for voicing opinions, and align decisions with shared values. For Muslim families, those shared values include avoiding riba (interest), giving zakat, and prioritizing halal income. A council makes these values operational rather than aspirational.

Key benefits for multi-generational Muslim families include:

- Structured communication: Regular meetings give every generation a voice, which reduces the feeling that elders dominate or that younger members are ignored

- Early conflict resolution: Disagreements about money surface in a controlled setting before they become family rifts

- Educational retreats: Some families hold annual retreats combining financial review with Islamic education and family bonding, which builds emotional investment in the process

- Stipends for participation: Offering a modest stipend to council members signals that their time and contribution are valued, which improves long-term engagement

- Succession planning: The council creates a natural space to discuss who will manage family finances as older members step back

Exploring financial literacy coaching alongside your council’s work can also help members build the individual knowledge they need to contribute meaningfully to group decisions.

Pro Tip: If your extended family is geographically spread across the US, consider holding one in-person meeting per year and the remaining three quarterly meetings virtually. Consistency matters more than location.

Aligning family finances with Islamic principles through a family council

This is where a family financial council becomes especially powerful for Muslim families. Islamic financial planning means earning, saving, and growing money in a halal way, avoiding riba and paying zakat regularly. A council gives you a formal mechanism to make these principles part of your household’s actual financial operations, not just your intentions.

Here are four concrete ways your council can embed Islamic principles into your family’s financial life:

-

Define halal income standards. The council reviews each family member’s income sources and establishes a shared policy on what qualifies as halal. This is especially relevant for families with investments, business income, or employment in sectors that may carry Sharia concerns.

-

Establish interest-free financial rules. The council formally prohibits interest-bearing products within the family’s financial framework. This includes credit cards used for revolving debt, conventional mortgages without halal alternatives, and savings accounts that generate riba.

-

Schedule zakat calculations and payments. Rather than leaving zakat to individual memory, the council sets a fixed time each year, typically before Ramadan, to calculate and distribute zakat collectively. This ensures no one in the family misses this obligation. You can learn more about calculating zakat to prepare your council for this responsibility.

-

Review investments for Sharia compliance. The council conducts an annual review of all family investments, checking for exposure to prohibited industries such as alcohol, gambling, or conventional banking. This review can be supported by a qualified Islamic finance adviser.

How to establish and run a family financial council effectively

Knowing why a council matters is one thing. Building one that actually functions is another. Here is a practical framework for getting started.

-

Select 5 to 9 members with balanced representation. Include adults from different generations and, where appropriate, different branches of the family. Most families set the minimum age at 18. Avoid selecting members based solely on wealth or seniority.

-

Define meeting structure and cadence. Quarterly council meetings handle active financial decisions. The annual family assembly, which is larger and includes all family members, is for sharing updates and gathering input. These are two distinct forums with two distinct purposes.

-

Hire or appoint an external adviser. Success factors include hiring an adviser, offering stipends for members, and scheduling regular non-business bonding activities to build trust. An adviser, whether a financial planner, an Islamic finance specialist, or a family governance consultant, keeps meetings focused and prevents personal dynamics from derailing financial discussions.

-

Draft a family financial charter. This document defines the council’s mission, decision-making authority, voting procedures, and term limits. It does not need to be lengthy, but it does need to exist in writing.

-

Keep council and assembly roles distinct. Mixing family council and family assembly roles is a common pitfall. The council makes decisions. The assembly receives information and provides broader input. Blurring these roles creates confusion about who actually has authority.

Pro Tip: Start small. If your family has never had formal financial governance, a three-person council with a simple one-page charter is far more effective than an elaborate structure that never gets implemented. You can always expand as the family grows in size and financial complexity. Browse Islamic finance budgeting guides to support your council’s early work.

| Element | Family council | Family assembly |

|---|---|---|

| Size | 5 to 9 elected members | All eligible family members |

| Meeting frequency | Quarterly | Annually |

| Primary role | Decision-making and governance | Information sharing and input |

| Decision authority | High | Low to advisory |

| Typical agenda | Budgets, investments, policies | Updates, education, bonding |

Practical financial planning within the family financial council framework

A council’s governance structure only creates value when it produces real financial plans. A complete family money strategy includes budgeting, saving, investing, debt reduction, and estate planning, and it enhances confidence across the entire household. Your council is the body that builds and maintains that strategy.

Here is what practical financial planning looks like inside a family financial council framework:

- Halal income and expense tracking: The council establishes categories for income and spending that reflect Islamic priorities, including halal food, sadaqah, and religious education, while excluding haram expenditures

- Religious savings goals: Dedicated savings funds for Hajj, Umrah, Ramadan, and Eid are built into the annual budget, not treated as optional extras. See the saving for Hajj guide for a detailed approach your council can adopt

- Education funding: Long-term savings for children’s Islamic and secular education are planned and reviewed annually

- Emergency reserves: The council sets a target for household emergency savings, typically three to six months of expenses, and monitors progress

- Halal grocery and household budgeting: Practical categories like halal grocery budgeting are part of the monthly review

| Financial goal | Recommended council action | Review frequency |

|---|---|---|

| Zakat payment | Calculate and distribute collectively | Annually, before Ramadan |

| Hajj savings | Set monthly contribution target | Quarterly |

| Emergency fund | Monitor balance against 3 to 6 month target | Quarterly |

| Halal investment review | Screen for Sharia compliance | Annually |

| Education savings | Review contribution and growth | Annually |

Why a family financial council is a game-changer for Muslim families’ financial harmony

Most Muslim families in the US have strong values around money. They know riba is prohibited. They know zakat is an obligation. They know wealth should be earned and spent with integrity. What most families lack is a formal structure to translate those values into consistent, coordinated financial decisions across the entire household.

That gap is where financial disharmony grows. One family member opens a conventional savings account without realizing the interest implications. Another delays zakat because no one set a shared date. A third makes an investment without checking Sharia compliance because there was no process for doing so. None of these are failures of faith. They are failures of governance.

The council acts as a values-and-governance bridge, aligning long-term goals without disrupting daily life. That is the insight most families miss. A family financial council does not replace individual financial responsibility. It creates the shared framework that makes individual decisions more consistent and more aligned with what the family actually believes.

There is also an emotional dimension that often goes unacknowledged. When family members feel heard in financial discussions, they are more likely to comply with shared decisions. A council that includes bonding activities, educational sessions on Islamic finance, and genuine dialogue builds the trust that makes financial governance feel like a shared project rather than a top-down mandate. Families that invest in this emotional infrastructure, not just the financial mechanics, tend to sustain their councils far longer.

The truth is that most Muslim families are one generation away from losing financial clarity. Wealth, values, and financial habits need to be transmitted intentionally. A Muslim family budgeting strategy is far more likely to survive across generations when it is embedded in a governance structure than when it exists only in one person’s memory.

Explore Amanah Budget for halal financial planning support

Once your family financial council is in place, you need tools that match your values. Amanah Budget is a halal-first budgeting app built specifically for Muslim families in the US, and it fits naturally into the financial planning work your council will do.

With Amanah Budget, your family can track spending using halal-aware categories, calculate zakat according to your preferred madhab, and set dedicated savings goals for Hajj, Umrah, Ramadan, and education. You can share household budgets with your spouse or other council members, connect bank accounts securely, and receive AI-assisted spending insights that reflect your financial priorities. No ads, no interest-based products, and no selling of your data. Just a financial tool built around your deen and your dunya.

Frequently asked questions

What is the main difference between a family council and a family financial council?

A family council is a broader governance body covering family affairs and business decisions, while a family financial council focuses specifically on financial governance, including budgets, investments, and planning aligned with family values. A family council is a small elected group acting as a decision-making body, often part of larger governance frameworks focused on family-related business or finances.

How can Muslim families ensure their financial council decisions comply with Islamic principles?

Muslim families can embed Islamic rules directly into the council’s governance processes, including avoiding riba, ensuring halal income, budgeting for zakat, and reviewing investments for Sharia compliance annually. Islamic financial planning involves earning, saving, and growing money in a halal way, avoiding interest and paying zakat regularly.

Who should be part of a family financial council and how often should it meet?

Typically, family financial councils consist of 5 to 9 elected family members, often starting at age 18, and meet quarterly to make financial decisions and oversee governance. Family councils generally include 5 to 9 members with terms around 2 to 3 years and hold quarterly meetings.

What are common challenges when establishing a family financial council?

Common challenges include confusing council and assembly roles, lacking written governance documents, and failing to review the council’s alignment with evolving family values over time. Mixing family council and family assembly roles creates inefficiency, and separating their cadence and scope is crucial for clear decision-making.

Recommended

- The Best Budgeting Strategy for Muslim Families: A Practical Guide — Amanah Budget Blog

- Amanah Budget Blog — Islamic Finance, Zakat, and Halal Budgeting Guides

- Amanah Budget — Halal Budgeting App for Muslim Families | Zakat Calculator, Hajj Savings

- Halal Grocery Budgeting: Why Muslim Families Spend More (and How to Plan for It) — Amanah Budget Blog

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account